- In response to the global pandemic, we have already witnessed two stages of state intervention: a liquidity injection, followed by continuing emergency support for struggling economies.

- Stage three involves government and central-bank support for restructuring economies that are transitioning from old ways of doing business to new ones, and will be the most difficult stage of the recovery.

- We anticipate that the global recovery is more likely to be shaped like a U-bend rather than in the form of a ‘V’ or ‘W’.

- We expect to see a deflationary environment over the next 12 months, but beyond that, we believe inflation is more likely to return.

The bounce in markets during the second quarter of 2020 enabled bond strategies to recover most of the losses that they suffered during the initial dislocation caused by the pandemic in March. The second half of the year will be more difficult, however, as we anticipate that low cash and government-bond yields will continue, alongside a rise in corporate defaults and downgrades.

One of our primary investment themes, which plays a key role in fixed-income investing, is state intervention, and we have already witnessed two of the three phases of state intervention in response to the pandemic over the last six months: first, March’s liquidity injection, and secondly, continuing emergency support for the pandemic-induced fall in gross domestic product (GDP). This began in April, but may continue well into the autumn.

Difficult phase three

The third phase of state intervention will be more difficult to navigate. It concerns the support from government and central-bank authorities for a restructuring of economies as they transition from an old way of doing business to a new one; the difficulty stems from the fact that some of the emergency measures that are in place roll off before companies and employees can benefit from any new economic direction. In this third phase, we would expect to see more ‘recovery fund’-type fiscal stimulus and less direct employment support. However, this transition is hampered by the need to extend phase two owing to the lingering virus threat, and the politics of getting the stimulus packages approved.

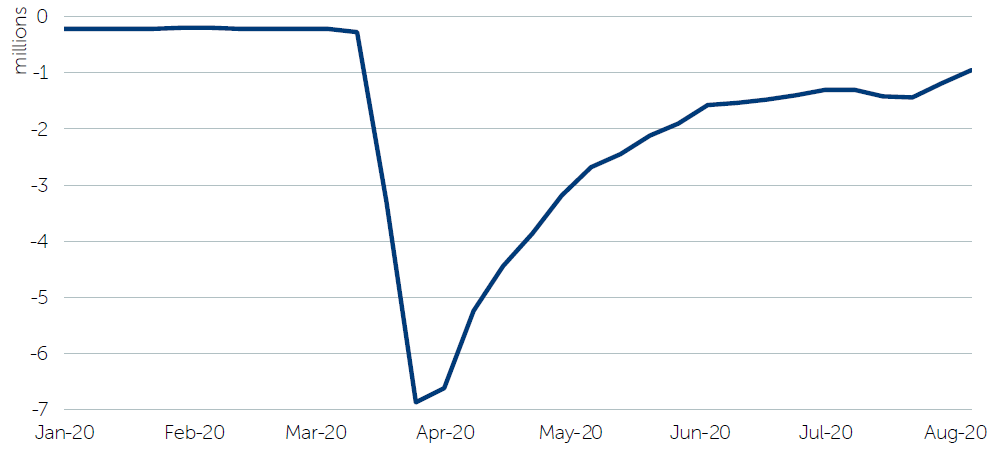

The chart below shows initial US unemployment claims and is a good example of our view that economic data (having bounced from the lows of the March/April lockdown periods) will take a while to get back to pre-crisis levels. While the market has debated a ‘V’ or ‘W’-shaped recovery, we have been talking about a U-bend shape.

US initial jobless claims, 1 January-6 August 2020

Source: Bloomberg, 7 August 2020

No immediate return

There are a few reasons why we think economies will not return in two years’ time to the same pattern in which they were before the pandemic. This is about more than the virus alone, and has its roots in the leverage-distorted system which was in place prior to the pandemic, which helped to create untenable wealth inequality which, in turn, fuelled populism and a reversal of the globalisation trend.

As always with a crisis, there are reasons why previous trends are accelerated and new trends emerge. The global financial crisis was a good example: economies weakened and then recovered, political parties changed, and some other pre-existing trends accelerated while new ones came into force. The rise of social media, smartphones and technology continued after the crisis, probably helped in part by the low cost of finance and the abundant availability of venture capital. The banking system, however, had to restructure by shrinking balance sheets and reducing staff.

Significant economic turmoil always leads to a change in political parties as new leaders suggest they can do better than their predecessors, and a disillusioned electorate looks for change. The long-term trend of globalisation was also a casualty of the global financial crisis; the current calls to bring jobs home and rising trade tensions are a symptom of this.

People crisis

The new crisis is a people crisis rather than a financial one, and therefore the systems that are in need of a restructure are those that are connected to a change in the way people live, rather than a restructuring of the financial system. Therefore, the prior trends that are not hit by this change should continue, and may receive a boost from the availability of cheaper money and, more importantly, the increasing use of fiscal stimulus rather than just loose monetary policy.

For example, the rise of populism and its negative effect on trade is likely to continue, but crucially, as governments get more involved in the economy, investment in environmental projects is likely to rise and the focus on the social agenda will also pick up; the wellbeing of staff will be a key concern and health-care systems will see more investment too.

ESG considerations

When it comes to environment, social and governance (ESG) concerns, the increasing focus on the ‘E’ that we witnessed prior to the crisis should continue as the recovery grows. The ‘S’ agenda is more difficult to define, but those employers that look after their staff through greater use of flexible working and wellbeing support may attract the highest-calibre workers. Finally, the ‘G’ consideration should also attract heightened interest, as weak economies tend to flush out bad practice.

The sectors that need to change or adapt are those that were gearing up before the crisis based on previous trends that are no longer there. For example, the airline industry was constantly focused on expanding passenger traffic, but much of this growth may not now materialise. Many of the deflationary trends that were there in the decades before the crisis had already started to roll off – for example, globalisation and demographics. Over the next 12 months as economies restructure, unemployment is likely to remain high, demand weak, and inflation at low levels.

Inflation lurking further out?

Once that transition has passed, there is a real possibility that inflation could end up higher than it was previously. Prior to the crisis we were starting to worry about many of the deflation champions reaching a share of the market where (instead of looking to gain market share at a cheaper price) they would be inclined to raise prices as their market share plateaued. For example, low-cost airlines were steadily increasing prices as their competition was squeezed out of the market. The airlines that survive the current dip in travel demand will be operating with lower capacity and, perhaps as a result, higher costs.

Meanwhile, the ‘baby boomer’ generation is retiring, and thus shifting from saving to consumption mode. Deglobalisation will receive fresh impetus as supply chains are shortened (but become more inefficient), trade barriers are erected, and politicians try to boost domestic employment. Finally, from their current low levels, we anticipate that energy prices could rise as we shift towards more renewable energy sources – all factors that could lead to higher inflation over the longer term.

Authors

Paul Brain

Deputy chief investment officer of Multi-Asset

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that holdings and positioning are subject to change without notice.

Comments