Against a diverse emerging-market backdrop, we use themes to identify globally important, observable forces of long-term change that we believe can influence our investible universe. In a short series of posts we explore key themes that play a role in helping us to select our emerging-market investments, starting with ‘state intervention’.

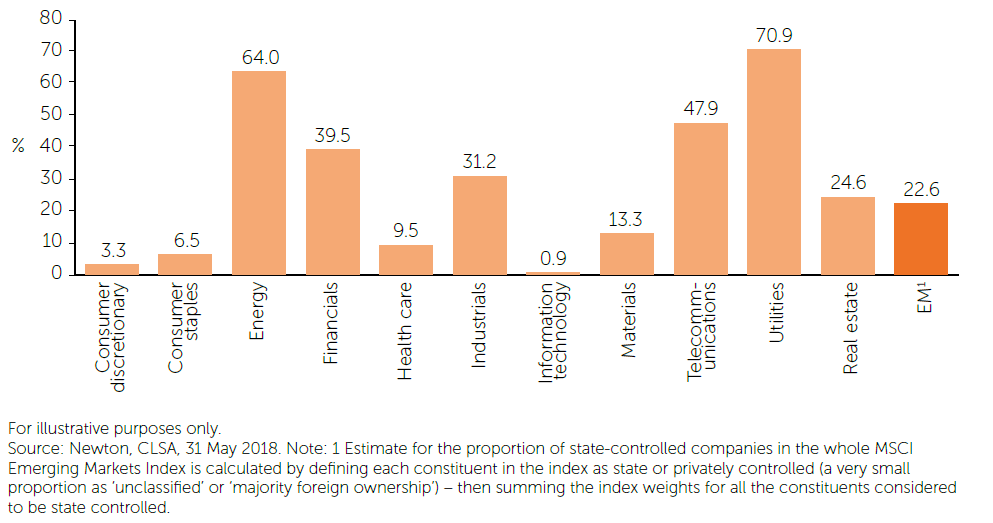

In more developed markets, concern over state intervention centres around central bank policymaking. While that is of course highly relevant across emerging markets too, there is in fact an even larger state-led consideration when investing in these markets: the fact that c.23% of the MSCI Emerging Markets index is comprised of state-owned enterprises (SOEs).

Exhibit 1: MSCI Emerging Market sectors – estimated state control

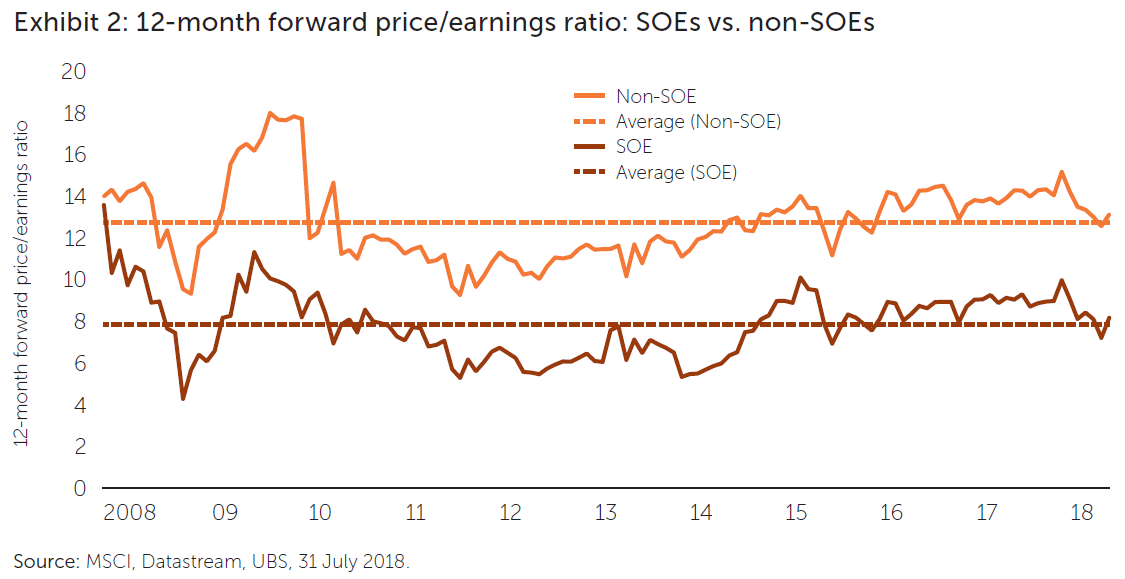

The majority of these companies are not run with profit-maximising intention. They tend to be strategic state assets such as banks, or utility and resources companies, with heavy capital-expenditure burdens. This tends to make them poor stock investments over the long term, though a major commodity bull market can change the optics temporarily. Return on equity (ROE) is usually less important than other strategic desires of the state in capital-allocation decisions.

State ownership can provide stability, but this may involve significant shareholder value dilution, as minority investors tend to be a low priority in stressed situations or in capital-allocation decisions. Interestingly, we saw such dilution with many Western banks following the global financial crisis, and emerging-market companies are perhaps even less likely to focus on shareholder value in such situations.

Of the larger emerging markets, the proportion of state ownership is highest in Russia at c.55% and China at c.40%, though the Middle Eastern countries United Arab Emirates (UAE) and Qatar have the highest rates overall at 96% and 81% respectively.

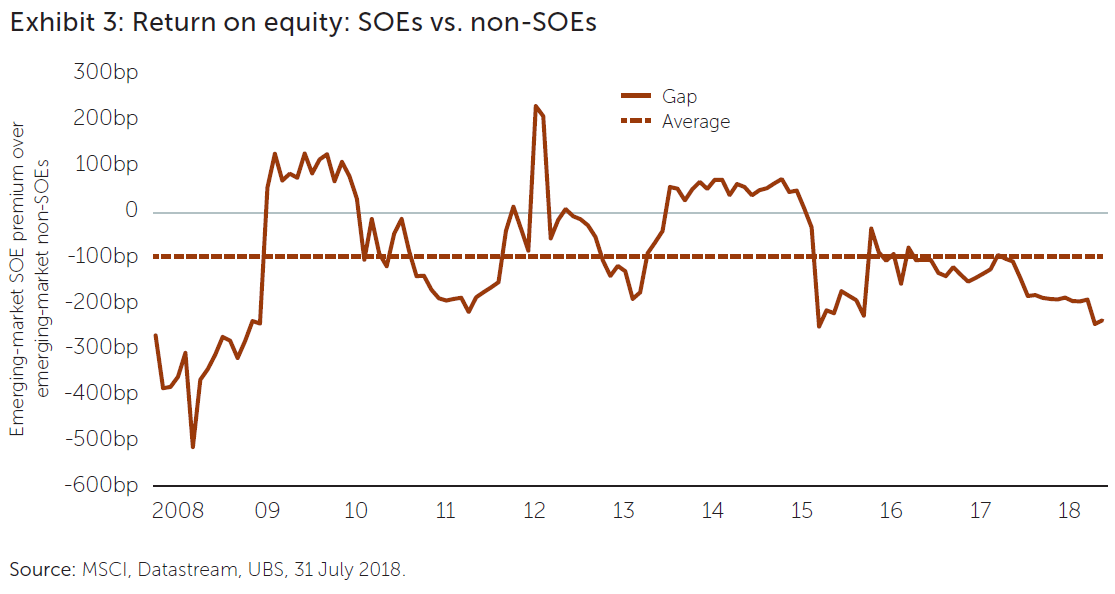

History teaches us that the interests of a Russian oligarch or the Chinese politburo are rarely aligned with those of minority investors, and we therefore believe our active approach which allows us to currently take zero exposure to SOEs is a big advantage. SOEs have significantly underperformed non-SOE companies over both the long term and more recent periods (11.5% vs. 22% over the 12 months to end May 2018), despite trading at a wide valuation discount. This, we believe, is owing to them, in aggregate, being perennial value destroyers on a through-the-cycle basis. Exhibit 3 shows that there is a long term ROE gap (11.05% vs. 13% and widening) between the two types of companies owing to the lower quality of SOEs, which tend to have more indebted balance sheets, lower growth rates and higher capital-expenditure burdens, leading to lower cash flows and returns.

Conversely, the technology, consumer and health-care sectors are relatively free from state control and are where we find the most interesting investment opportunities.

Authors

Newton emerging markets & Asia equities team

The team who manage our emerging & Asian equity strategies

This is a financial promotion. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those countries or sectors. Please note that holdings and positioning are subject to change without notice. Compared to more established economies, the value of investments in emerging markets may be subject to greater volatility, owing to differences in generally accepted accounting principles or from economic, political instability or less developed market practices.

Comments