Amid price instability, heightened geopolitical risks and volatility, investment opportunities remain.

Last year was a transition year – and a painful one at that. The end of the Cold War, the break-up of Russia, and the advancement of China had driven inflation and interest rates lower for decades, creating a benign environment for risk assets. However, the 2020 Covid-19 pandemic led to unprecedented spending and assistance – with global central banks spending the equivalent of nearly US$800m every hour for 18 months. This was bound to have an inflationary impact, with the subsequent environment seeing the fastest, most aggressive interest rate-hiking cycle in decades.

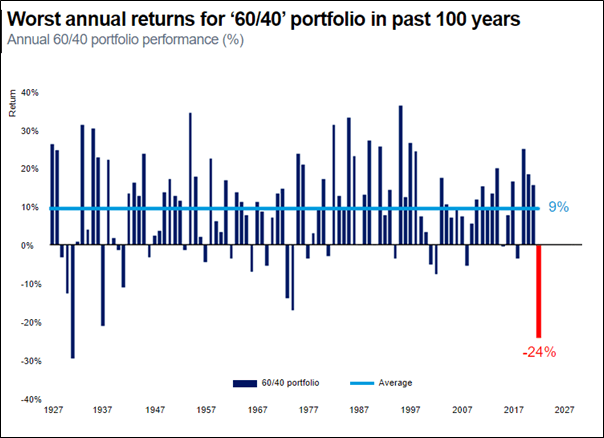

In the context of this transition, 2022 was a difficult year across all asset classes, disrupting the negative correlations that have supported the traditional 60/40 equity/bond asset-allocation model in recent years. Against this backdrop, we believe bonds may no longer be the best way to stabilise portfolios. While it appears unlikely that we will return to the c.15% interest-rate levels experienced by past generations, a return to zero interest rates also looks improbable any time soon. This is why we believe it is important to start considering a broader set of alternative investments.

Source: BofA Global Investment Strategy, GFD Finaeon. 2022 estimate is annualised as of December. Reprinted by permission. Copyright © 2023 Bank of America Corporation (“BAC”).

I would highlight the attractiveness of a few such alternatives, such as carbon. In 2005, carbon emissions trading schemes were initiated, allowing companies to sell on unused credits which bigger polluters can buy. Europe has become the largest carbon trading market in the world. Today, with the increased global focus on emissions and lowering targets, each year the supply of unused credits is becoming constricted.

Another area of alternatives relates to continuing electrification, which is driving greater demand for commodities. Such is the growing demand for commodities that we may eventually see governments start to hoard supply in anticipation of future shortages – such as in copper. Other aspects of the energy transition, like wind farms and solar panels, have other attractive qualities, such as somewhat predictable cash flows thanks to implicit and explicit government support.

Another potential area where alternatives can offer diversifying effects is volatility itself. Volatility can be seen as an asset class, and some of the instruments in this area can offer the prospect of equity-like returns with roughly half the volatility.

Reflecting this view, allocations within our Real Return strategy have increasingly favoured alternatives in recent years. As of the end of April 2023, just under 20% of the strategy was invested in alternatives such as infrastructure, music royalties, energy storage, commodities and risk premia.

We also favour consumer companies with pricing power as well as domestic producers (companies that do not have to worry about foreign-exchange issues), commodities and health care. The latter has been an unloved area thanks to worries over patent expiries. However, post Covid, the health-care industry is trying to catch up on procedures that were delayed, while innovation in drugs has become an exciting area that could save governments billions in health-care provision, particularly in areas like Alzheimer’s and obesity.

Elsewhere, we see opportunities in China’s reopening, and while we find select individual Chinese/Hong Kong securities attractive, we believe index futures can be a liquid and efficient way for a diversified, multi-asset strategy to gain exposure to the reopening story. Liquidity is key for us in this market as we want to be able to exit quickly should it be necessary.

While we value alternatives’ attractive diversification and return potential, we believe there is still a place for risk assets. Although we are cautious, we view the use of alternatives as providing an opportunity to be more dynamic. If we are to learn from times such as the high-inflation, rising-rate environment of the 1970s, we must remember that such periods also saw aggressive equity rallies, in spite of the challenging economic backdrop. It is therefore important to be adaptable.

We do expect volatility to rise, and we believe that the way in which an investment strategy manages that eventuality is likely to become increasingly important. Volatility does create opportunities and dispersion of performance between different securities, sectors and asset classes, which we believe favours active stock selection.

Authors

Andy Warwick

Co-head of Real Return team

This is a financial promotion. These opinions should not be construed as investment or any other advice and are subject to change. This material is for information purposes only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that portfolio holdings and positioning are subject to change without notice.

Comments