Key Points

- We are in a new market regime characterized by lower economic growth, sustained pressures on inflation, higher interest rates, and less accommodative monetary policy.

- With a 33-year track record, our Dynamic US Equity strategy has faced and successfully navigated different market regimes over time.

- The strategy’s expanded toolkit and disciplined investment process becomes more defensive on equities when the return outlook is challenged and increases exposure when return expectations are constructive.

- Currently, our forecasted equity risk premium is near its long-term average, while the macro outlook is cloudy. With downside risk to earnings growth, the strategy retains a defensive target exposure to equities of 90% and no exposure to bonds.

- Our estimate of the bond term premium continues to oscillate around zero, the carry along the curve is negative and the inflation battle is far from over.

Below Average Equity Risk Premium Driving Lower Equity Allocation

Newton’s Dynamic US Equity strategy (DUSE) seeks to outperform the S&P 500® over time with dynamic exposures that seek to enhance returns in a rising equity market and provide more protection in a declining environment. The strategy takes a flexible approach to how much equity beta it is targeting at any given time, typically ranging from 80-130%. To determine whether to be overweight (>100%) or underweight (<100%) equities, our investment process uses long-term, forward-looking expected return estimates in order to derive risk premia across equities, bonds, and cash. The return estimate for stocks is based on bottom-up fundamental consensus earnings growth estimates which is then complemented with top-down macro forecasts which can account for any developing tail risks. Our expected return on stocks is then compared to bonds and long-term cash to determine our estimate of the equity risk premium.

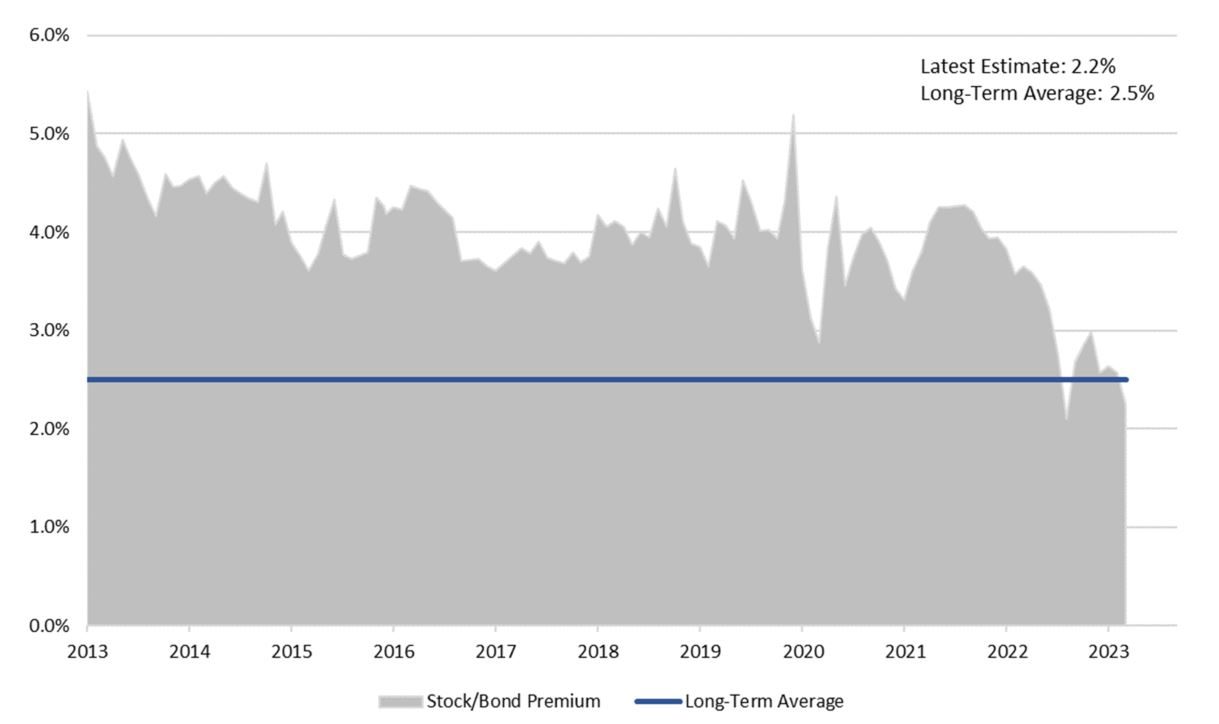

Since September 2022, the DUSE strategy has been underweight US equities with a 90% target exposure. This underweight stance is warranted according to our investment process given higher valuations, elevated risk of recession or at least below-average growth, negative earnings revisions, and pressure on margins. All else equal, the higher the equity risk premium, the higher the overall equity allocation will be at any given time. Our estimate of the equity risk premium (expected return on stocks over corporate bonds) is approximately 2.2%. For much of the post-global financial crisis-period, our estimated equity risk premium hovered at around 4%. However, it came crashing down in 2022, driven by higher bond yields and lower earnings growth.

As shown in the chart below, our current equity risk premium forecast is near the long-term average. The expected return on stocks is 7.4% and corporate bonds is 5.2%, which derives the 2.2% equity risk premium. To see an improvement in our estimate, there would need to be (1) a sell-off in equities, (2) a decline in long-term yields, and (3) an improvement in the earnings-per-share growth of S&P 500® companies.

Our Estimated Equity Risk Premium Has Narrowed Since 2021

Source: Newton, as of 5/31/23.

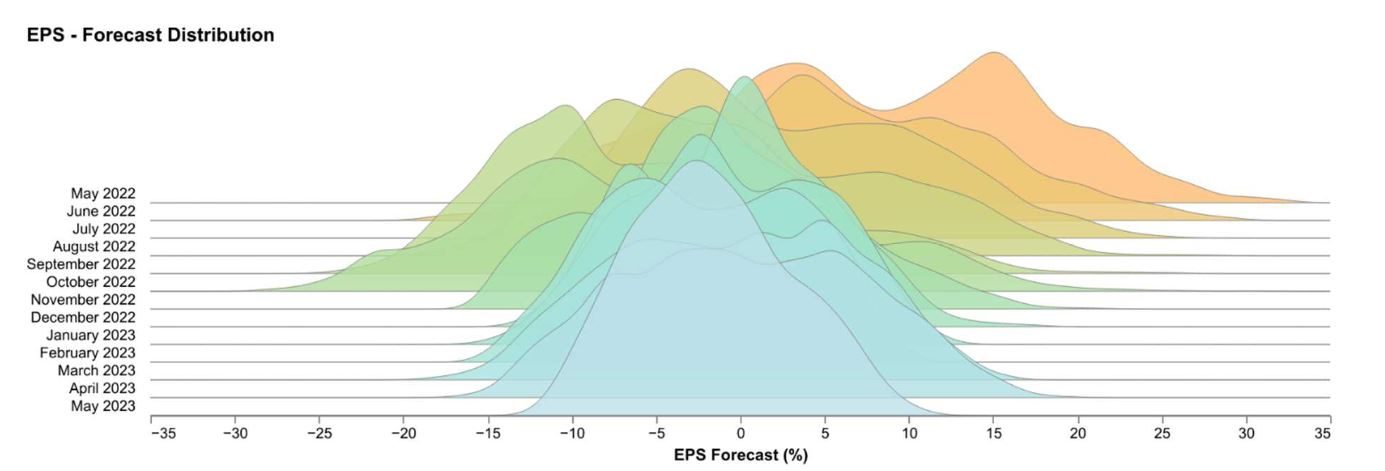

The 12-month consensus earnings-per-share growth, through to May 31, 2024, is currently 5.9%, while our own forecast is -1.7%. The diagram below shows the distribution of Newton’s S&P 500 earnings-per-share (EPS) growth forecast in 12 months’ time.

Newton S&P 500 Index EPS Forecast Distribution

Source: Newton, as of 5/31/23.

Term Premium Remains Unattractive

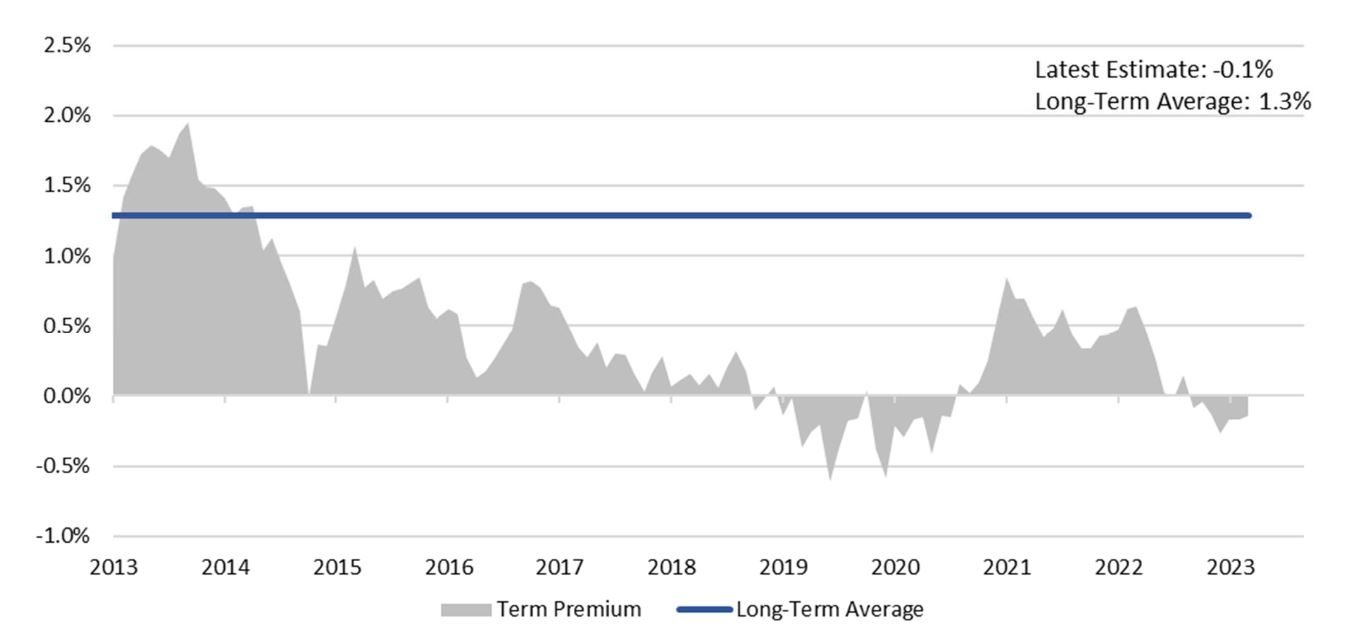

A modest allocation to US Treasury bonds and/or cash is allowed within the strategy to diversify and counterbalance the dynamic equity exposures over time. The primary role for bonds is risk mitigation—as long-term US Treasuries have been the chief diversifier for stocks during market corrections and over the long run. On a secondary basis, bonds can provide excess return in an equity bear market (2022 aside). To determine if a bond allocation is warranted in the strategy, we look to stock/bond correlations as well as our estimate of the term premium. Viewed from those lenses, bonds have not been attractive in the strategy for some time. Recently, the correlation between stocks and bonds has been slightly positive and closer to zero, making bonds a less reliable diversifier after many years of mostly negative correlations. In addition, given the extreme rise in short-term interest rates, our term-premium forecast for US long-term bonds is just negative at -0.01%. Based on this estimate, bonds have not been attractive, but that outlook significantly worsened in 2022 when 3-month Treasury bill rates rose from 0.07% to 2.9%. We began 2022 with a very modest (6%) allocation to bonds to complement our overweight equity exposure (115%) but eliminated that position in September 2022 when our estimated return on cash exceeded long-term bonds amid the Federal Reserve’s brisk pace of interest-rate rises, making it unattractive to bear duration risk.

Our Estimate of the Term Premium Is Negative and Far Below its Long-Term Average

Source: Newton, as of 5/31/23.

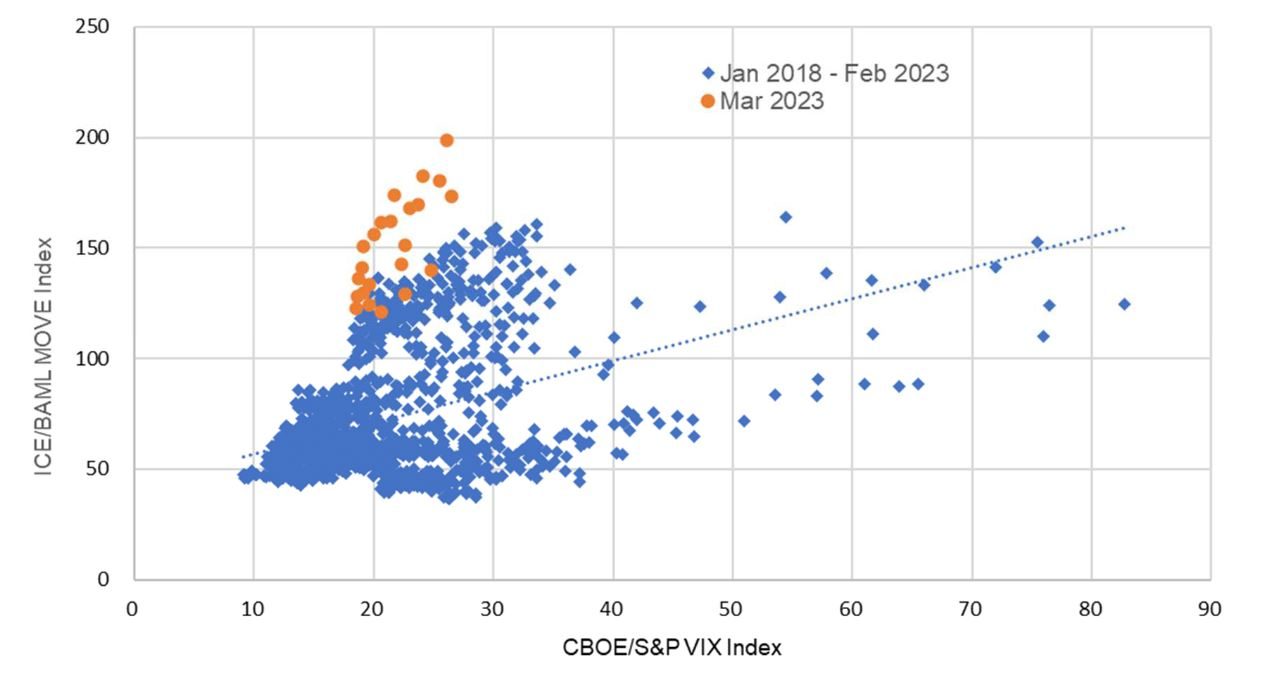

In our view there are other reasons to be cautious toward bonds. The ICE Bank of America MOVE Index, which measures bond-market volatility, recently reached its highest level since 2009, while the US equity market (as measured by the CBOE VIX index) remained comparatively calm, even in the face of the regional banking crisis created by the failure of Silicon Valley Bank and Signature Bank. This reflects a high level of uncertainty around the future path of interest rates as the Federal Open Market Committee (FOMC) waits for credit conditions to tighten and lower overall economic activity and ultimately inflation.

ICE BofA MOVE Index vs. CBOE VIX Index – Daily Levels

Source: Newton, as of 3/31/23.

Macro Outlook Points to Stagflationary Environment

Dynamic Equity’s investment process is first and foremost rooted in efficient portfolio construction and an assessment of current risk premia. We complement our bottom-up fundamental process with a top-down macroeconomic forecast. This macro forecast leverages proprietary signals that ultimately give us insight into the current and future state of earnings. This top-down insight is invaluable as stock analysts tend to remain optimistic and can be slow to revise earnings expectations. We believe our macroeconomic forecasting approach can better identify turning points in the regime and what may be priced in versus the consensus. Importantly, we do not just generate a point forecast for earnings growth over the next 12 months, for instance, but we look at the range and magnitude of the tails estimated by a number of economic models. This range provides us insight into whether risks are skewed to the upside or downside. As we seek to deliver consistent returns and prudent risk management, we incorporate tail risks and whether the distribution of potential outcomes is wide—which would indicate greater uncertainty and a lack of consensus.

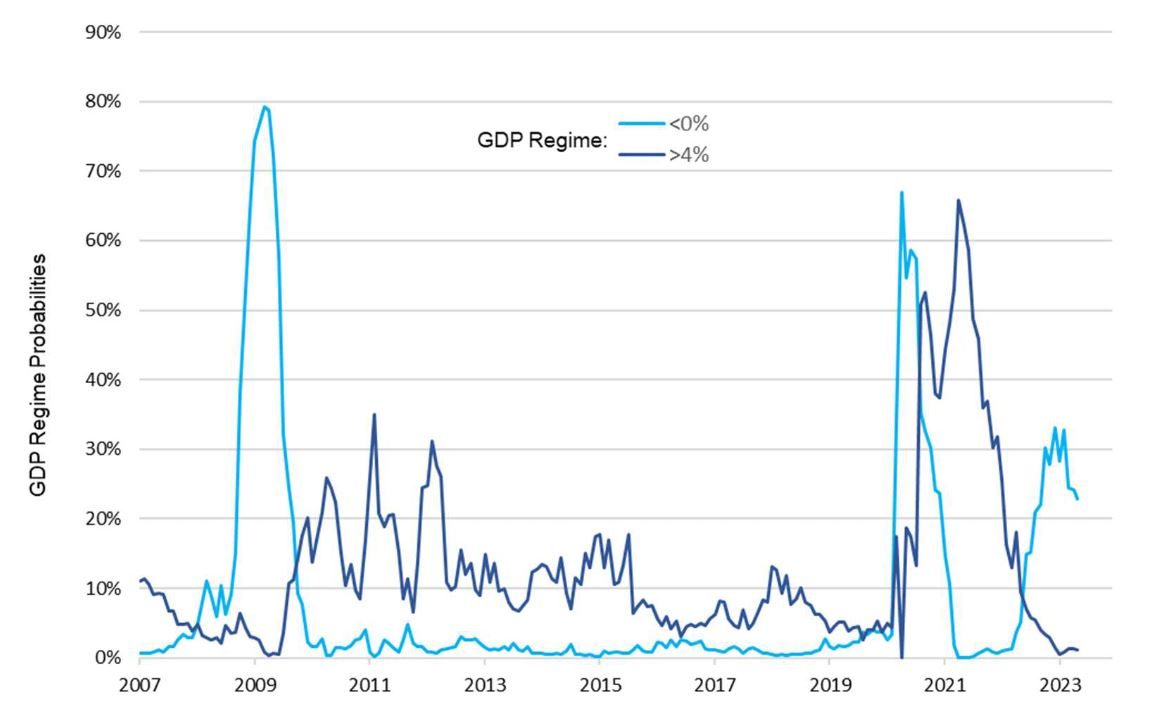

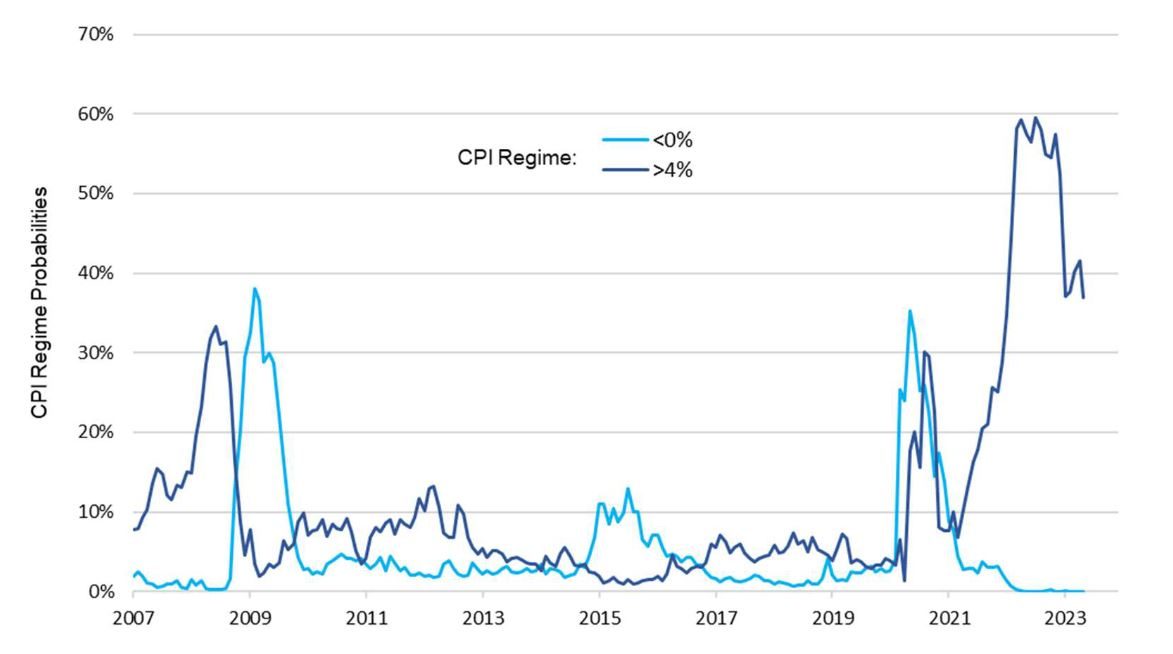

As of the end of May, our base case over the next 12 months is below average real US GDP growth (+1.0%) and lower but still high inflation of 3.4%. This is consistent with a stagflationary environment. Interestingly, our US real GDP forecast distribution still shows a meaningful risk (23%) of below 0% growth but there has been some improvement over the last three months.

Newton US Real GDP Forecast Probabilities

Source: Newton, as of 5/31/23.

Newton US Inflation (CPI) Forecast Probabilities

Source: Newton, as of 5/31/23.

Looking Forward

The current positioning in Dynamic Equity is supported by an average equity risk premium, down from its post global financial crisis highs, challenged stock valuations and a stagflationary economic environment which we believe will lead to weaker earnings growth. Certainly, over DUSE’s 33-year history, there have been pockets when the market temporarily diverges from fundamentals.

While we expect and are positioned for a challenging market environment, Dynamic Equity has an expanded toolkit to navigate different market environments. This includes:

- Underweight positions: While we are currently underweight equities in our US strategy and neutral in our global ex-US version, if risk premia deteriorate further, we can reduce equity exposure further as well as take a short position in bonds.

- Convexity through options: We continue to implement convexity through equity options to provide a humility hedge in the event our positioning is incorrect, which would benefit the strategy if the equity market rise.

- Overweight cash: The strategy can (and currently does) take a net long position in cash given heightened short-term yields, which is rare in our long history.

- Overweight risky assets: If the equity risk premium improves, we would likely increase our long exposure to stocks. Similarly, if the bond term premium improves and/or if bonds become more diversifying, we may enter a long exposure to bonds.

To overweight risky assets such as bonds or equities, there are several variables we monitor closely on a daily basis:

- Re-pricing of equities: The simplest way for equities to become more attractive, and for our estimate of the equity risk premium to rise again above long-term averages, is through lower equity prices. Alternatively, lower long-term bond yields or positive surprises in EPS growth could improve our equity outlook but appear unlikely in the near term.

- A reduction in short-term cash rates: If the FOMC were to cut rates, our overall estimate of long-term cash would fall. The FOMC’s summary of economic projections clearly shows no rate cuts until mid-2024; however, the market anticipates a cut before the end of 2023, predicated on a hard landing and/or heightened risk to the stability of the financial system.

- Negative equity/bond correlation: According to our long-term forecast and high frequency intra-day tick data, the equity/bond correlation is approximately zero. Prior to the pandemic and unprecedented stimulus, the correlation was negative. If bonds were to become less correlated and thus a more attractive source of diversification, the attractiveness of bonds would increase.

- Recalibration of longer-dated yields: Eventually the term premium will revert to positive; however, it will take time for market participants to adjust to a new regime that is likely to include higher longer-term inflation. Alternatively based on breakeven rates, the market assumes the inflation battle will be won within the next two years, if not sooner. The first option could lead to higher yields on longer dated Treasuries while the second option could lead to lower cash rates; either option will translate to a higher bond term premium, we are just not there yet.

Important Information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC (“NIMNA” or the “Firm”). NIMNA is a registered investment adviser with the US Securities and Exchange Commission (“SEC”) and subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand “Newton” or “Newton Investment Management”. Newton currently includes NIMNA and Newton Investment Management Ltd (“NIM”) and Newton Investment Management Japan Limited (“NIMJ”).

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Past performance is not necessarily indicative of future results. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.