Since developer OpenAI’s ChatGPT chatbot captured people’s attention following its public release in late 2022, the topic of artificial intelligence (AI) has never been far from the headlines, generating both huge excitement and deep concern. In recent weeks, it has been reported how AI is being used to discover new antibiotics,1 create a new Beatles song,2 and generate audio commentary for the Wimbledon tennis championships.3 Elsewhere, with AI presenting a potential threat to large numbers of jobs, even Hollywood actors have raised concerns about being replaced in films and TV shows without proper permissions or payment.4 Meanwhile, acknowledging the risks as well as the upsides of the technology, the founders of OpenAI signaled that AI may eventually require an international regulator equivalent to the International Atomic Energy Agency.5

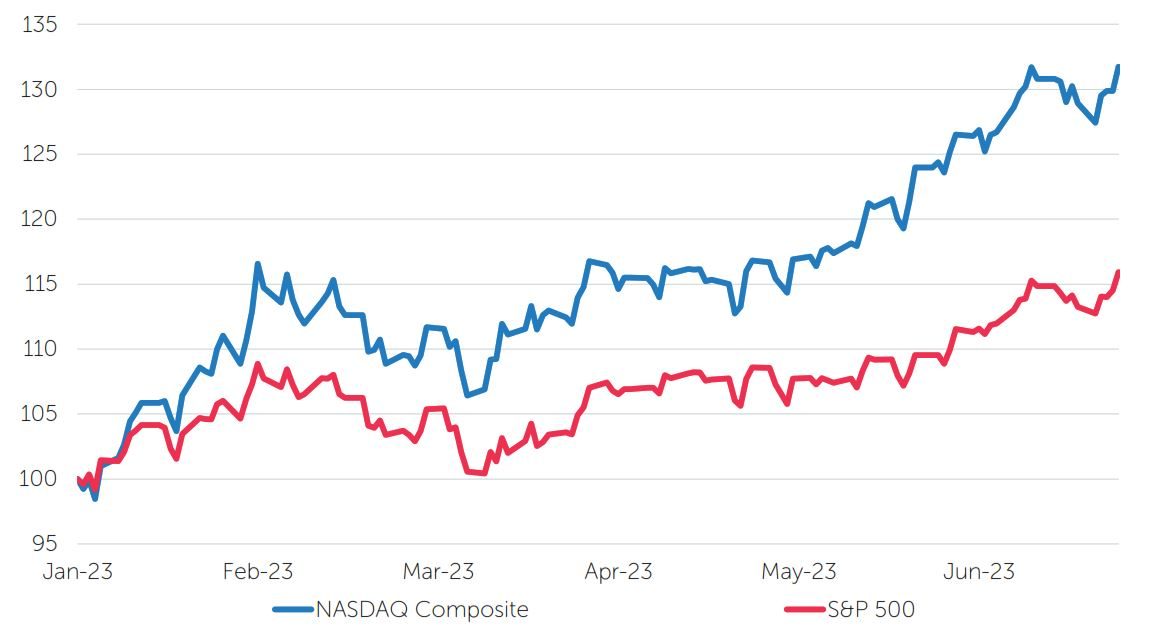

During the second quarter of 2023, financial-market participants continued to drive a rally in the large US technology companies that are expected to benefit from the growth of AI. The Nasdaq Composite Index, which is heavily weighted towards companies in the information technology sector, rose by 12.8% during the quarter, cementing a gain of almost 32% for the first half of the year, nearly twice that of the broader S&P 500 Index over the same period.6

S&P 500 Index and Nasdaq Composite Index

Price (US$), rebased to 100 at 31.12.22

Source: FactSet, July 2023.

On a regional basis, the Japanese equity market was the strongest performer in local-currency terms. After years of stagnation, the country is starting to see higher inflation and a rebounding economy. In addition, recent policy actions by the Japanese government have sought to improve corporate governance and foster more shareholder-friendly behaviors.

A number of other tailwinds helped support equity markets during the quarter. US consumer price inflation showed further signs of easing in May, rising by 4%, its lowest annual increase in more than two years.7 Investors were also encouraged by a seemingly resilient US economy, with over 600,000 non-farm jobs being added during April and May,8 well ahead of forecasts and reinforcing the ‘soft-landing’ narrative as consumer spending remained strong. In addition, US corporate earnings for the first quarter, while declining for the second successive three-month period, came in significantly ahead of analysts’ expectations, diminishing some concerns about the need for a significant adjustment to 2023 consensus estimates.

Nevertheless, there was also plenty for market participants to worry about. A key issue was the future trajectory of interest rates, as core inflation (excluding food and energy) threatened to remain elevated despite easing headline figures. While the US Federal Reserve (Fed) opted to leave rates unchanged in June, Fed Chair Jay Powell indicated that two further interest-rate rises were likely this year,9 putting further pressure on the economy. The European Central Bank (ECB) maintained similarly hawkish messaging, raising rates by 0.25% again in June and signaling it would do the same in July, as it warned that the battle against inflation was far from over.10 The Bank of England, meanwhile, surprised markets in June with a 0.5% rate increase as the May inflation print came in higher than expected at 8.7%, well above readings in the US and continental Europe.11

In China, the strength of the post-Covid recovery was called into question, with various economic indicators, such as retail sales and investments, weaker than expected as the country’s beleaguered property sector in particular has remained a drag on the economy.

After making gains in the first three months of the year, the recovery in fixed-income markets stalled in the second quarter as interest-rate rises remained on the agenda, and 10-year US Treasury yields (which move inversely to prices) were up 31 basis points to 3.81%. Government bonds, as represented by the JP Morgan Global Government Bond Index, produced a return of -2.2% in US-dollar terms (+0.8% over six months). Corporate bonds, as represented by the ICE BofA Global Corporate Index, returned +0.1% over the quarter (+3.5% over the year to date).12

Most major equity markets made positive returns over the three-month period. North American equities returned +8.5% over the quarter (+16.7% over six months), while Japanese stocks returned +6.4% (+13.2% over the year to date) in US-dollar terms. Meanwhile, European equities delivered a positive return of +3.1% (+14.2% over six months), UK equities were up +2.2% (+8.4%), and emerging-market equities returned +1.0% over the quarter (+5.1% over six months) for US-based investors. Finally, Asia Pacific ex Japan equities fell by -0.9% (+3.2% over the year to date).13

Gold delivered a negative return of -2.6% in US-dollar terms over the quarter (+5.2% over the year to date).14

At the start of June, the US Senate approved a fiscal deal to raise the country’s debt ceiling, ending a long political stand-off that threatened to trigger a historic debt default in the world’s biggest economy. As part of the deal, non-defense fiscal spending will be capped in 2024 and 2025, although spending cuts appear unlikely to have a significant impact on the economy in the near term. However, the deal means the US Treasury will be looking to replenish its balances at the Fed, primarily through increased issuance, which could serve to tighten liquidity and may negatively affect bank reserves.

Although there was no repeat of the turmoil seen in March, the US regional banking sector remained under pressure during the quarter as regulators speedily arranged for First Republic Bank to be rescued by JPMorgan Chase, wiping out its shareholders in the second-biggest bank failure in the country’s history. The collapse of First Republic highlights how banks that relied on low-cost deposits have become exposed in a higher interest-rate environment.

The banking crisis may have been a factor in the Fed’s decision to hold off raising rates in June, but with both inflation and growth projections revised upwards at the June meeting, the Federal Open Market Committee’s latest ‘dot plot’ projection is predicting two further quarter-point hikes this year, increasing the potential for ‘breakages’ in other vulnerable sectors.

In the UK, thousands braved the rain in London and millions more turned on their TVs to celebrate the coronation of King Charles III on May 6. There was little, however, to celebrate for the millions of households seeking to remortgage this year, as financing costs rose sharply ahead of the Bank of England’s decision to raise interest rates in June in an attempt to restore its credibility in the fight against inflation.

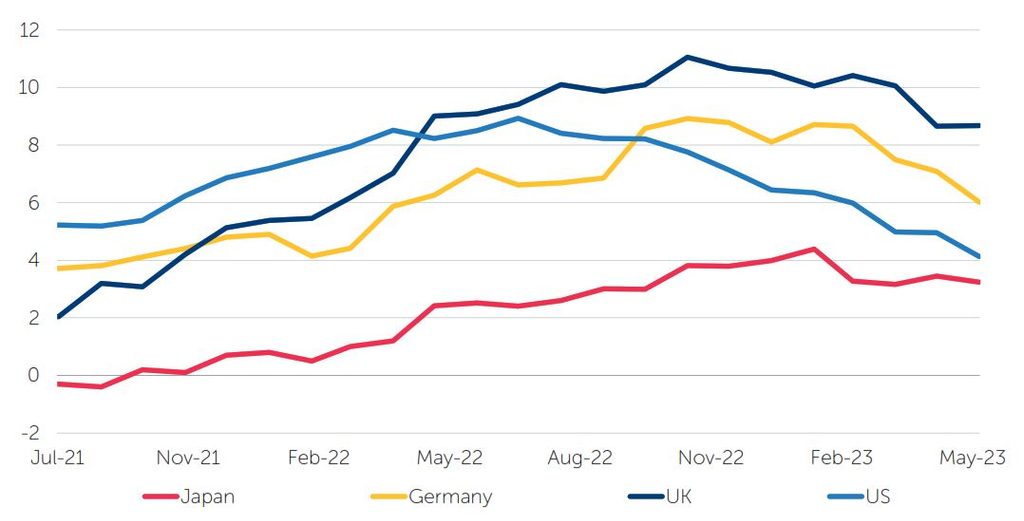

Speaking in May, Bank of England Governor Andrew Bailey admitted that the UK had been experiencing “second-round” inflationary effects, as higher energy and food prices have led to persistent wage growth and price increases by companies, risking a wage-price spiral.15 The UK appears more vulnerable to such a development than the US or European Union (EU), as it is more reliant on food and energy imports and its labor market has been constrained by post-Brexit rules.

Consumer Price Inflation

% change year on year

Source: FactSet, July 2023.

While the UK’s economic outlook has recently improved,16 thanks in large part to falling energy prices, consumer confidence is likely to be hampered by rising mortgage costs and other inflationary pressures for the remainder of the year.

In Europe, Germany closed the last of its nuclear power stations in April.17 Despite the continuing energy crisis as a result of the Russia-Ukraine conflict, the government believes nuclear power is unsustainable and will distract from a focus on renewable-energy production, while opponents view the closures as ill-advised at a time when sources of low-carbon energy are urgently needed.

Germany’s economy appeared to need an energy boost, as its federal statistical agency reported that gross domestic product (GDP) had declined by 0.3% during the first quarter, lagging many of its European counterparts. The country has experienced weakness in its important manufacturing sector, while consumption fell 1.2% from the previous quarter as consumers have been hit by increasing borrowing costs and rising inflation.18

While the eurozone economy has remained weak, with GDP shrinking slightly for the last two quarters, the labor market has remained resilient, with ECB President Christine Lagarde describing its strength as “incredible.” She also asked governments to promptly roll back the fiscal support launched during the energy crisis, to avoid pushing up inflation that would ultimately require an even stronger monetary-policy response.

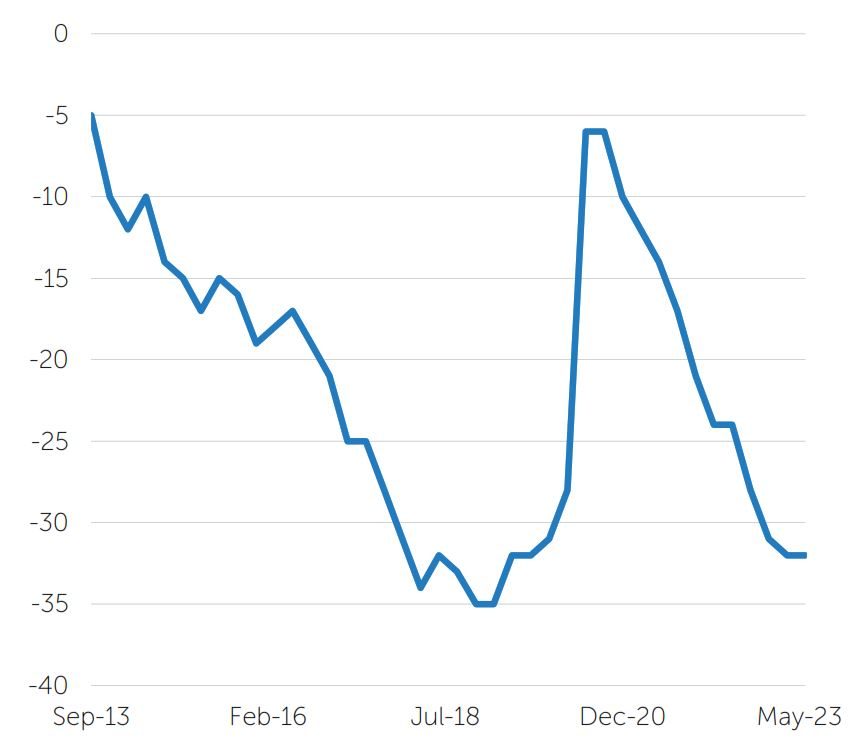

The rekindling of Japan’s economy is evident in the resurgence of wage inflation. The Bank of Japan’s (BoJ) quarterly Tankan survey of economic conditions is highlighting how companies are finding it increasingly difficult to find labor, forcing them to offer higher wages and improved benefits. The annual ‘shunto’ wage negotiations between unions and major companies this spring saw the highest wage increases in over 30 years, with the growth in base salaries (excluding automatic wage increases based on seniority) reaching 2.3%, compared with 0.5% a year earlier.19

Japan Tankan Employment Conditions – All Enterprises, All Industries

Source: FactSet, July 2023.

Business sentiment for both services and manufacturers rose in June compared to three months previously, with sentiment among large Japanese manufacturers improving for the first time since 2021, as the costs of raw materials started to fall. Meanwhile, large companies plan to boost capital expenditure by 13.4% in the current fiscal year.20 Core inflation has remained above the BoJ’s target, and its ‘core-core’ index that excludes fresh food and fuel rose by 4.3% in May, the biggest annual increase since June 1981.21

Against this backdrop, the BoJ looks set to become more hawkish over time. It seems likely that the policy of yield-curve control – which has resulted in enormous distortion of the Japanese government-bond market – could be abandoned later this year.

The People’s Bank of China cut its main policy rate in June as data continued to show that the post-Covid rebound was faltering. Retail sales increased by 12.7% from the prior year in May 2023, although they were down from 18.4% in April and missed expectations.22 The property sector, which was an important source of growth across the economy before the pandemic, has remained weak, with real-estate investment falling by 7.2% between January and May, compared with the same period in 2022.23 The sector’s malaise has dragged down related industries such as construction, and consumers remain reluctant to invest after a number of developers went into default during the pandemic. Exports also fell significantly in April.

Further stimulus in addition to rate cuts is likely to be required if China is to reach the 5.0% growth target it has set for this year. This could include infrastructure spending, tax breaks for consumers, or providing property developers with assistance to help them complete unfinished real-estate projects.

INVESTMENT IMPLICATIONS

As we enter the second half of the year, the much-anticipated global recession still appears to be far from the horizon. With the exception of the UK, where inflationary pressures appear more embedded, annual headline inflation figures have begun to fall significantly across Europe and the US in recent months, and there has been little sign of weakening in labor markets. Global equity markets have avoided a sell-off in spite of several interest-rate hikes from major central banks, and US technology stocks in particular have seen a resurgence as investors rush to buy the AI trend.

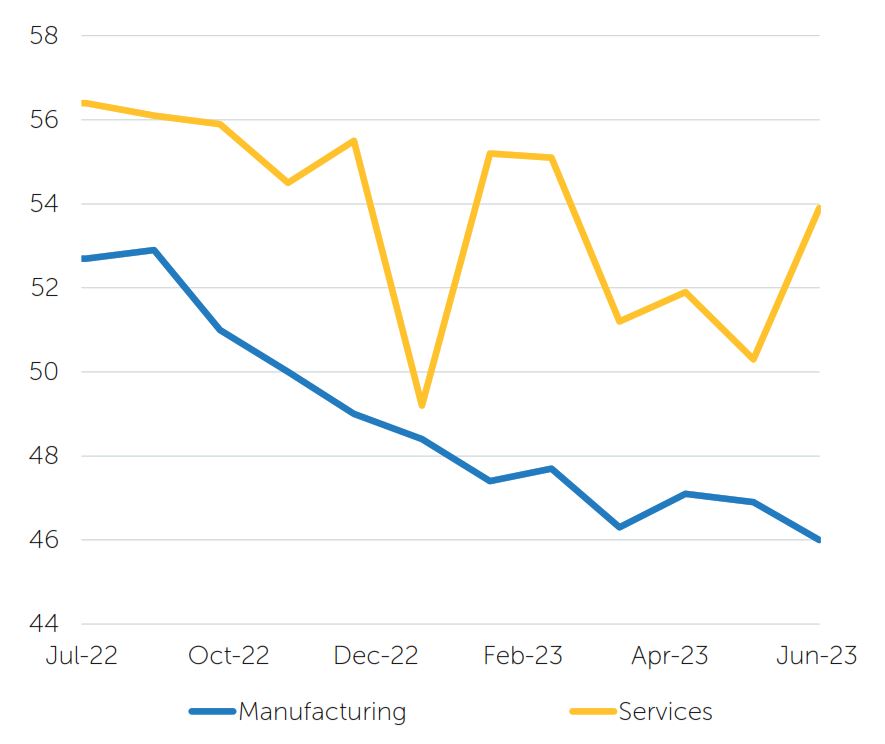

However, closer examination of some key data points reveals a less rosy picture. While headline inflation rates have dropped as last year’s energy price shock fades away, ‘core’ inflation (which excludes energy and energy prices) has remained persistent over the last year and is proving harder to curb, with the rate still above 5% in both the US and the eurozone (and around 7% in the UK). Meanwhile, manufacturing purchasing managers’ indices across the world have moved into contraction territory, while inventories have built up in both the US and Europe, hinting at weaker demand.

Service sectors have remained more resilient and have seen continued growth, though this is, in part, likely to be a delayed impact of the pandemic, as people have used savings built up during lockdowns to spend money on experiences after reopening. The unique circumstances of the post-Covid environment have also led to distortions in the labor market, with many workers simply leaving the market through sickness or choice while labor demand remains high. These and other factors have served to delay the effects of monetary tightening.

US Institute for Supply Management Purchasing Managers’ Index

Source: FactSet, July 2023.

In this context, central banks may need to administer further pain if they are to keep their word and persist in their fight against stubborn inflation. Interest-rate rises are ultimately a blunt instrument, taking months to filter across the global economy and take full effect. The data points that central banks are monitoring – such as employment and wages – are lagging indicators, and the risk of monetary-policy error is significant. Ultimately, rising unemployment may be the price Western economies have to pay to truly quash inflation, and a slowdown towards the end of this year, or even early in 2024, looks hard to avoid.

In the meantime, the removal of the ‘cheap money’ that dominated the backdrop in the years following the 2008 global financial crisis could lead to further breakages as vulnerable sectors adjust to a higher-interest-rate world. In addition to the troubles already seen in the US regional banking sector, stresses could develop in other areas that became reliant on easy access to credit, such as commercial real estate, leveraged loans, and the housing markets in regions like Scandinavia and the UK.

Against this backdrop, we believe we are in an economic phase where ‘safe-haven’ government bonds look increasingly appealing, although we would favor those markets where interest-rate increases look to be fully priced in. We would advocate broadening exposure as evidence builds that the continuing tightening of policy is causing economies to slow.

We believe careful security selection will be important when allocating to investment-grade corporate bonds, and a very cautious approach to high-yield credit is required in view of the heightened recession risk. Conversely, certain emerging markets have had a very different economic and interest-rate profile from their developed counterparts, and there may be pockets of opportunity in local-currency emerging-market bonds that can offer positive real yields and positive yield curves.

After experiencing precipitous declines in 2022, high-growth technology-related stocks have reasserted their leadership in global equity markets during the first six months of the year, driven by enthusiasm about the potential for AI. Indeed, the ten largest stocks in the S&P 500 have been driving the recent rally and now account for around 75% of the total market capitalization. While in many cases earnings are expected to grow materially, it is worth bearing in mind that many of these businesses sit on high multiples, and some are facing increased regulatory scrutiny and stiff competition.

With the prospect of a slowdown and with earnings likely to come under pressure, dividends can be more resilient, and it is noteworthy that, during previous inflationary periods, income stocks have proved an attractive proposition for investors looking for inflation protection and defensiveness at a reasonable price. On a global basis, the valuation of stocks offering income at above-average rates remains attractive relative to low-income stocks.

With defensive characteristics in mind, we also favor consumer companies with pricing power, and parts of the health-care sector. The latter has been an unloved area owing to worries over patent expiries. However, post Covid, the health-care industry is trying to catch up on procedures that were delayed, while innovation in drugs has become an exciting area that could save governments billions in health-care provision, particularly in areas like Alzheimer’s and obesity. Higher interest rates can benefit certain financials businesses such as insurers, which are able to invest their premium income at higher rates and improve the yield on their investment portfolios.

Elsewhere, the continuing push for electrification is likely to drive demand for commodities, such as copper. Other aspects of the energy transition, like wind farms and solar panels, can have attractive qualities that include somewhat predictable cash flows thanks to implicit and explicit government support.

The rise of AI could be the worst or the best thing that has happened for humanity.

Stephen Hawking, theoretical physicist, 1942-2018

1 Scientists use AI to discover new antibiotic to treat deadly superbug, The Guardian, May 25, 2023

2 Sir Paul McCartney says artificial intelligence has enabled a ‘final’ Beatles song, BBC News, June 13, 2023

3 Wimbledon to use AI for video highlight commentary, CNN, June 21, 2023

4 A.I. worries Hollywood actors as they enter high-stakes union talks, CNBC, June 7, 2023

5 Governance of superintelligence, OpenAI, May 22, 2023 (https://openai.com/blog/governance-of-superintelligence)

6 Source: FactSet, July 1, 2023

7 Pace of US inflation eases to slowest in over two years, Financial Times, June 13, 2023

8 Source: FactSet, July 1, 2023

9 Federal Reserve skips rate rise but signals two more increases on the way, Financial Times, June 14, 2023

10 ECB increases interest rates to highest level since 2001, Financial Times, June 15, 2023

11 Bank of England raises interest rates by 0.5 percentage points, Financial Times, June 22, 2023

12 Bond market returns sourced from FactSet, July 1, 2023

13 Equity market returns sourced from FactSet, July 1, 2023 (All US-dollar total returns, MSCI index series)

14 Gold bullion returns sourced from FactSet, July 1, 2023

15 Bank of England governor says the UK is facing a wage-price spiral, CNBC, May 18, 2023

16 UK economy returns to growth driven by consumer spending, Financial Times, June 14, 2023

17 ‘A new era’: Germany quits nuclear power, closing its final three plants, CNN, April 15, 2023

18 Fall in German GDP increases threat of sustained recession in EU’s largest economy, Financial Times, May 25, 2023

19 Source: CEIC, MHLW Haver, Morgan Stanley Research, April 5, 2023

20 Improving Japan business mood signals steady economic recovery, Reuters, July 3, 2023

21 Japan’s inflation stays above BOJ target, key gauge hits 42-year high, Reuters, June 23, 2023

22 Chinese economic data fuels gloom over recovery, Financial Times, June 15, 2023

23 China’s economic recovery is spluttering. The prognosis is not good, The Economist, June 22, 2023

All data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important Information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC. Newton Investment Management North America LLC (“NIMNA” or the “Firm”) is a registered investment adviser with the US Securities and Exchange Commission (“SEC”) and subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand “Newton” or “Newton Investment Management”. Newton currently includes NIMNA, Newton Investment Management Ltd. (“NIM”) and Newton Investment Management Japan Limited (“NIMJ”).

This document is provided for general information only and should not be construed as investment advice or a recommendation. You should consult with your advisor to determine whether any particular investment strategy is appropriate. Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements.

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that portfolio holdings and positioning are subject to change without notice.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario, including the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.