We analyse the potential consequences of tighter money supply and changing central-bank rate policy for the global economy.

Key points

- We believe the financial stress over the last few days initiated by the collapse of Silicon Valley Bank (SVB) is enough to rein in, but not stop, expectations of rate increases in the near term.

- We think it reasonable to assume that volatility around SVB and Credit Suisse could reduce investor appetite to take on European bank exposure.

- Looking to the longer term, we can link such events as SVB’s collapse to the ‘regime change’ in markets, and to trends identified by our financialisation and big government themes.

- We anticipate that we will see more ‘breakages’ this year, potentially in the leveraged loans market for example.

- Our biggest current concern is that tighter money supply causes a recession, thus derating both the economy and asset prices at the same time.

Investors can waste a lot of time and energy trying to predict what the central banks might or might not do over the coming days and weeks, but the bottom line is that we do not have a seat on their respective councils so will not find out until they make their announcements.

Financial stress

For us, the financial stress over the last few days, initiated by the collapse of Silicon Valley Bank (SVB), is enough to rein in expectations of rate increases for the moment, but if that volatility goes away, why wouldn’t central banks consider further rate hikes?

Meanwhile, we are focused on the secondary effects of the market volatility. Over the last few days, for example, we have received a number of questions from clients about our overall exposure to the European banking sector.

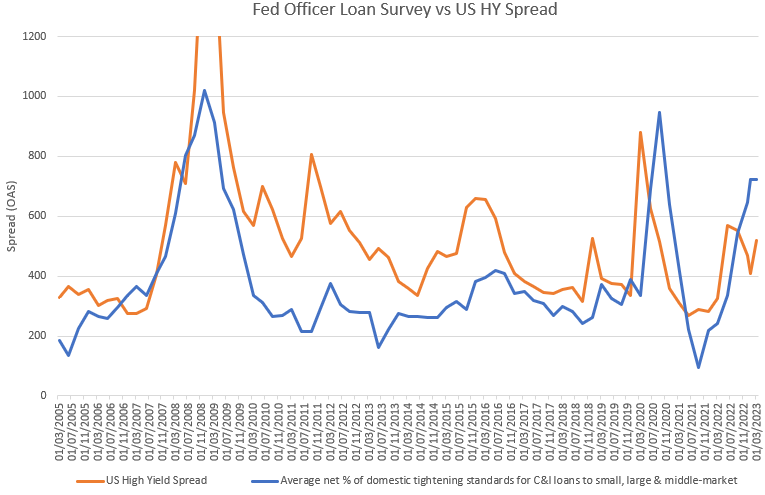

We think it is reasonable to assume that this volatility could have a global impact on the financial sector, and could, at the margin, reduce the appetite to take on risk. We have already seen the commercial banks tighten their lending criteria in the US (see chart below), and we are likely to see the same in Europe. The relationship between tighter lending standards and a weaker real economy is a strong one and gives us confidence that a hard landing for the economy may be coming sooner than financial markets imply. As the chart suggests, that tighter lending environment has an impact on more leveraged corporate bonds, especially if their issuers’ profits decline.

Source: Bloomberg, 15 March 2023

C&I refers to the commercial and industrial sectors.

‘Financialisation’ and ‘big government’

Looking to the longer term, we can link events such as SVB’S collapse back to our thematic research. When we talk about ‘regime change’ in markets, we are referring to trends identified by two of our macro themes: financialisation and big government. The move from ‘free money’ to ‘expensive money’ is a de-financialisation trend which could lead to a significant derating of financial assets.

When we consider areas such as technology start-ups, cryptocurrency, private capital markets and real estate, we believe the system can ‘break’ if things develop too quickly. We anticipate that we will see more ‘breakages’ this year, potentially in the leveraged loans market, for example. As asset managers, we used to talk about inflation being everywhere after the global financial crisis, but not on the narrow horizon of the central banks. We experienced asset-price inflation and goods-price deflation. Today, we are starting to see exactly the opposite.

Moving towards recession?

While the financial system is derating, the real economy has continued to do quite well, and thus central banks are obliged to do something about the inflationary consequences. In turn, this can cause things to malfunction in the financial system. Governments, on the other hand, are meddling in the real economy more than they have done in recent memory (our big government theme) and run the risk of exacerbating the inflationary backdrop by maintaining fiscal spending at elevated levels. This increases the de-financialisation trend as central banks are forced to raise rates.

What could change from here? We believe there are some signs that asset markets and the global economy could come back in sync. We see signs of fiscal spending that seeks to fix employment issues (the UK budget on 15 March for example) and thereby reduces the need for higher rates. Unfortunately, however, the biggest current concern for us is that tighter money supply causes a recession, thus derating both the economy and asset prices at the same time. We believe that we may be starting to witness this process.

Authors

Paul Brain

Deputy chief investment officer of Multi-Asset

Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic structure the security has been assigned to. This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that holdings and positioning are subject to change without notice.

Important information

This material is for Australian wholesale clients only and is not intended for distribution to, nor should it be relied upon by, retail clients. This information has not been prepared to take into account the investment objectives, financial objectives or particular needs of any particular person. Before making an investment decision you should carefully consider, with or without the assistance of a financial adviser, whether such an investment strategy is appropriate in light of your particular investment needs, objectives and financial circumstances.

Newton Investment Management Limited is exempt from the requirement to hold an Australian financial services licence in respect of the financial services it provides to wholesale clients in Australia and is authorised and regulated by the Financial Conduct Authority of the UK under UK laws, which differ from Australian laws.

Newton Investment Management Limited (Newton) is authorised and regulated in the UK by the Financial Conduct Authority (FCA), 12 Endeavour Square, London, E20 1JN. Newton is providing financial services to wholesale clients in Australia in reliance on ASIC Corporations (Repeal and Transitional) Instrument 2016/396, a copy of which is on the website of the Australian Securities and Investments Commission, www.asic.gov.au. The instrument exempts entities that are authorised and regulated in the UK by the FCA, such as Newton, from the need to hold an Australian financial services license under the Corporations Act 2001 for certain financial services provided to Australian wholesale clients on certain conditions. Financial services provided by Newton are regulated by the FCA under the laws and regulatory requirements of the United Kingdom, which are different to the laws applying in Australia.

Comments