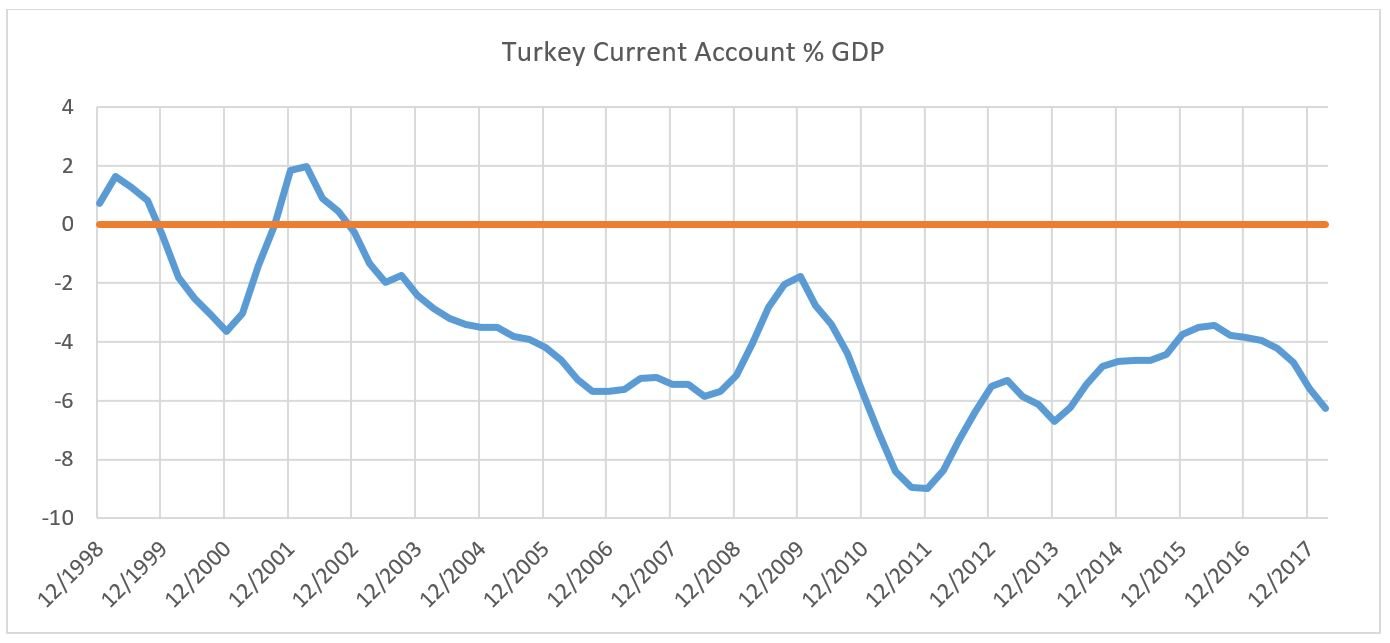

Turkey is the poster child for systems that for over a decade have luxuriated in abundant cheap global liquidity. Since the peak of the last U.S.-dollar bull market in 2001, dysfunctional global finance has provided Turkey with the credit needed to consume more than it has produced, which is reflected in its persistent current-account deficit.

Turkey’s Current Account as a Percentage of GDP (as at March 31, 2018)

Source: Bloomberg, 08/22/18

Tighter global financial conditions between 2012 and early 2016 led to an improvement in Turkey’s current-account deficit. However, as global financial conditions eased from the middle of 2016 onwards and finance become more readily available, the deficit once again began to deteriorate. The cumulative current account reflects the increase in the rest of the world’s financial claims on the Turkish economy.

Increased Liabilities

This increase in foreign liabilities can be seen on the balance sheets of Turkish corporations. Turkish companies’ foreign-denominated borrowings have more than doubled since the global financial crisis, with U.S. dollar-denominated debt standing at over $200 billion and euro-denominated debt at €100 billion.

The combination of tightening global financial conditions, significant funding requirements and a deteriorating political backdrop means there is a very real possibility that the situation has evolved into a fully fledged crisis of confidence. In the past, such scenarios have preceded the violent end to a country’s existing financial and economic structure. So does Turkey have an alternative to going bust? Possibly, but despite President Erdoğan’s assertion that “they have got dollars, we have got our people, our right, our Allah”, right now it really is all about hard currency: if the existing economic and financial structure of Turkey is to survive, it needs access to U.S. dollars. This is unlikely until the U.S. Federal Reserve stops tightening, and even then, avoiding a ‘bust’ is predicated on a return of liquidity before the liquidity crisis becomes a solvency crisis.

Is Turkey the Canary in the Coal Mine?

Should Turkey be considered an isolated event or is it one of those financial canaries in a coal mine? On the one hand, it is clear that local policy and Erdoğan’s bellicose handling of foreign relations have both contributed to the slide in Turkish assets. Those who believe such factors have been the main driver of the sell-off argue that Turkey is going bust for idiosyncratic reasons, and so maintain that a relatively risk-on stance is appropriate.

To us, there is little doubt that the protracted nature of Turkey’s bubble has ensured a deep structural maladjustment, misallocated capital and financial excesses. The risk is that, should the market continue to command higher yields on Turkish assets in order to provide compensation for increased risks, those financial excesses may prove unsustainable. Should Erdoğan adopt a more market-friendly approach to international relations and a more orthodox approach to domestic fiscal policy, perhaps Turkish yields will decline to a level where financing costs are consistent with sustaining the status quo.

Global Liquidity Malaise

However, the other school of thought is to view Turkey as merely the symptom of a wider liquidity malaise globally. The evidence increasingly suggests that the environment of self-reinforcing expanding liquidity, indiscriminate buying of financial assets (speculation) and rising asset prices/bullish trends has come to an end. In this context, declines in Turkish asset prices are met with selling rather than being regarded by many as a dip to be bought. Moreover, while Turkey is the most conspicuous example of this pattern to date, we believe it is one that is becoming increasingly widespread, marking a departure from market dynamics in 2017.

In fact, the increasingly widespread declines in asset prices (such as those currently seen most acutely in Turkish assets) are likely to further impede balance-sheet expansion and risk-taking within the global financial system, thereby weighing on the outlook for nominal growth and asset prices. Recent weakness in the share prices of European banks (particularly those in Spain, but also in France and Italy) reflects their significant exposure to Turkish creditors. In our view the share-price sensitivity of European banks to Turkey’s current travails is the financial market’s manifestation of how contagion plays out through the financial system rather than the real economy.

Authors

Brendan Mulhern

Global strategist, Real Return team

This is a financial promotion. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. Compared to more established economies, the value of investments in emerging markets may be subject to greater volatility, owing to differences in generally accepted accounting principles or from economic, political instability or less developed market practices.

Important information

This is a financial promotion. Issued by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Newton Investment Management Limited is authorized and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. 'Newton' and/or 'Newton Investment Management' brand refers to Newton Investment Management Limited. Newton is registered in England No. 01371973. VAT registration number GB: 577 7181 95. Newton is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Newton's investment business is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only.

Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms, including Newton and (iv) representatives of Newton Americas, a Division of BNY Mellon Securities Corporation, U.S. Distributor of Newton Investment Management Limited.

Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York or any of its affiliates. The Bank of New York assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith. © 2020 The Bank of New York Company, Inc. All rights reserved.