As the global pandemic fallout continues, we assess the relative merits of developed and emerging-market debt.

- Amid the continuing Covid-19 crisis, most major developed-market government debt levels are now comfortably above 100% of GDP.

- High public debt diminishes a sovereign’s ability to respond to future shocks, and is a principal predictor of fiscal crises.

- We believe it prudent for investors to retain some exposure to inflation-linked securities, and to diversify currency exposure towards countries with strong fundamentals and conventional policy capacity.

- Most – but not all – major emerging-markets’ government debt to GDP has remained more modest than developed-market counterparts. However, many lower-rated emerging-market sovereigns face mounting debt sustainability risks.

Public and private-sector debt was already at historically high and rising levels before the onset of the Covid-19 crisis, but this exogenous shock has triggered a further ballooning of fiscal deficits in response to the related collapse of economic activity.

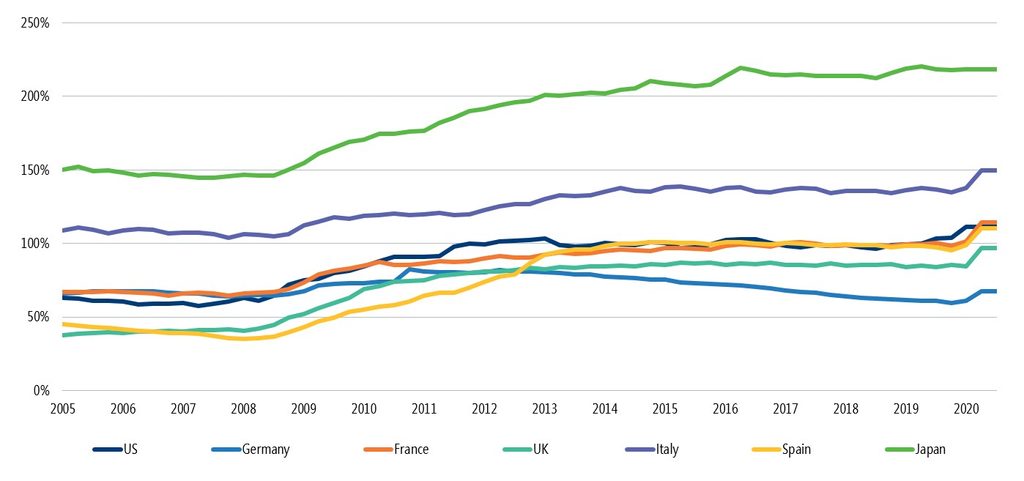

Developed-market government debt to GDP (as %)

As the above chart shows, developed-market government debt-to-GDP ratios were already running close to 100% in many cases (and more than double that level in Japan), as economies – with the exception of Germany – have had little success in deleveraging since the global financial crisis; this is despite the imposition of austerity programmes of varying degrees of stringency and duration. Amid the continuing Covid-19 crisis, major developed-market government debt levels are now comfortably above 100% of GDP.

Maintaining ultra-low rates

The ability of major central banks to maintain ultra-low interest rates and absorb supply is crucial to the sustainability of bloated sovereign debt obligations, but uncertainty over how long the current crisis will last, and widespread rejection of ‘austerity’ by electorates and (consequently) mainstream politicians, risks further increases in borrowing and the blurring of monetary and fiscal policy.

High public debt diminishes a sovereign’s ability to respond to future shocks and is a principal predictor of fiscal crises. At the current juncture, however, policy preferences are skewed more towards attempted deleveraging via public investment-led inflation and nominal GDP growth, than towards aggressive expenditure cuts.

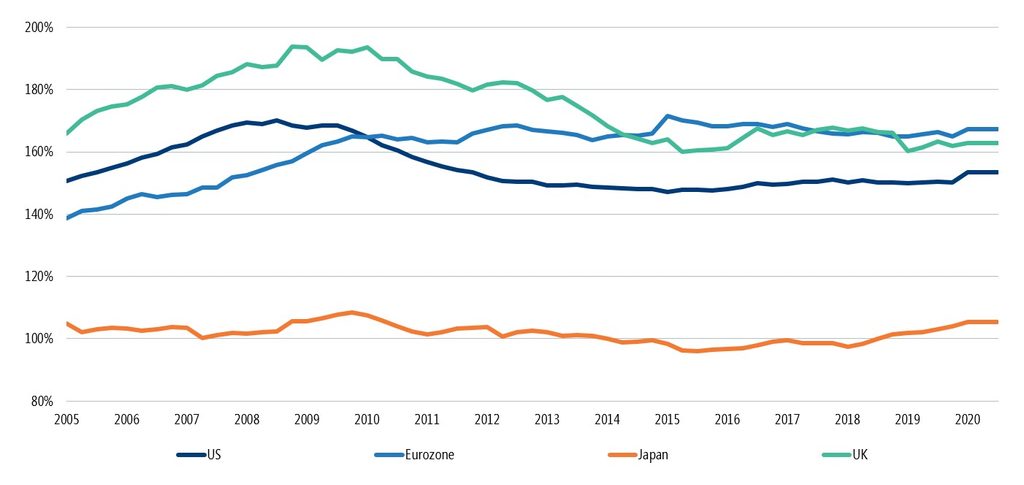

Developed-market non-financial private-sector debt to GDP (%)

In contrast to government balance sheets, the developed-market private sector witnessed a period of deleveraging following the global financial crisis. The current economic distress is likely to necessitate a further period of debt reduction and restructuring for companies acutely affected by the Covid-19-induced demand shock. Unprecedented buying of corporate bonds by central banks, and the ability of more sustainable businesses to access the market, may limit the scale of overall corporate deleveraging, but the extent to which companies are able to lengthen the maturity profile of their debt will depend on the strength and durability of the economic recovery.

Tempering future stimulus

Furthermore, should the recovery gather pace, and corporate (and household) balance sheets begin to expand once more, a timely tempering of government stimulus will be key to the dampening of potential inflationary risks, particularly in the case of a more muted central-bank reaction function – as already articulated in the case of the US Federal Reserve (Fed).

We are very mindful of these risks of longer-term upward price pressures, and consequently believe it prudent for investors to retain some exposure to inflation-linked securities. Equally, we are conscious of the downside risks for currencies undermined by sharply widening twin deficits (fiscal and external) and interest-rate inertia. The US dollar and sterling are particularly vulnerable in this regard, and we believe it sensible for bond investors to favour other (particularly Asian) currencies with more attractive fundamentals in the present environment.

Emerging-market debt manageable…for most

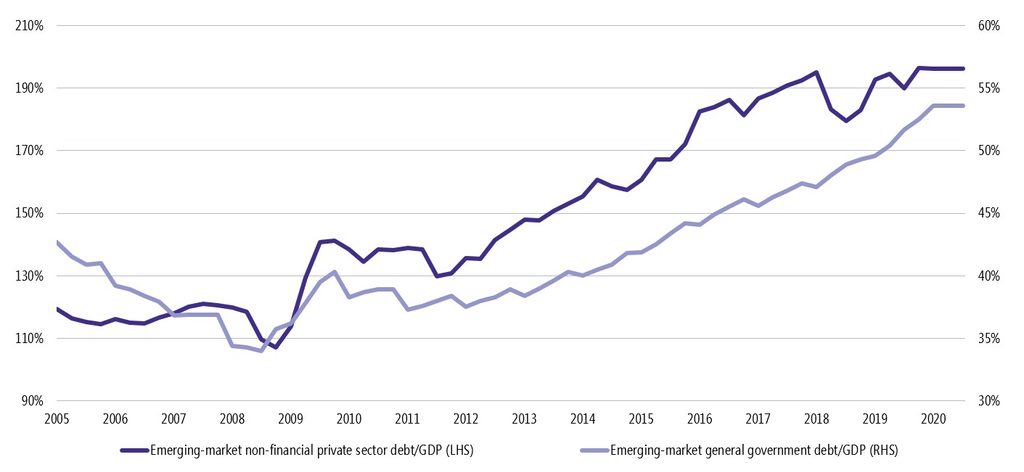

In the case of emerging markets, both government and private sector debt-to-GDP ratios were already rising steadily prior to the Covid-19 crisis owing to a number of factors: lower global interest rates, developed-market investors’ search for yield, weaker growth, and lower commodity prices.

Headline emerging-market government debt-to-GDP levels have remained manageable (54% of GDP as at the end of the first quarter of 2020), particularly for most major emerging-market economies where debt is predominantly local currency-denominated; this supports our relatively constructive view on the asset class through periods of accommodative global US-dollar liquidity.

The current crisis has seen many of the major emerging markets respond with fiscal stimulus packages and unprecedented central-bank asset purchases. However, the scale of these policies has remained reassuringly modest versus the developed-market experience (i.e. low to mid-single-digit percentages of GDP in emerging markets versus double-digit percentages of GDP in developed markets). This, coupled with accommodative Fed policy, has helped to limit emerging-market currency depreciation, despite the longer-term risk that monetary discipline wavers on a more permanent basis. That said, currency and fiscal risks are already apparent for two major emerging markets – Brazil and South Africa – which are characterised by high debt levels, weaker external balances, and low real interest rates.

Lower-rated country outlook more challenged

For many lower-rated (single B) emerging-market sovereigns, external balances are typically weaker, and a larger proportion of the debt stock is foreign currency-denominated. The multi-year rise in borrowing for these countries is more concerning. Official sector support in the form of emergency International Monetary Fund (IMF)/World Bank funding and G20 debt service suspension (recently extended to June 2021) has cushioned the immediate pandemic impact, but debt sustainability for these governments depends on an enduring global economic recovery. We have tended to favour sovereigns characterised by low debt-to-GDP ratios, strong foreign-exchange reserve adequacy, and constructive IMF engagement.

Emerging-market corporate debt levels were already at very concerning levels pre-Covid (see below), rendering us cautious on the asset class for some time, and very much cognisant of the higher dollar-denominated nature of the debt stock, and the potential contingent liability risks for some emerging-market sovereigns.

Fed policy reduces emerging-market debt risk

The sudden halt to capital flows in March/April threatened a reckoning, but the Fed’s liquidity provision, and renewed capital inflows since, are helping companies to access the market and mitigate rollover risks again. We continue to prefer emerging-market sovereigns where such risks are either negligible or mitigated by the solid (investment grade-rated) credit strengths of the government (e.g. Mexico, Malaysia or China).

An unexpectedly strong developed-market recovery would potentially present renewed capital-account risks for emerging markets (as witnessed during the 2017-18 period of emerging-market corporate deleveraging), but the Federal Reserve’s commitment to accommodative policy helps to render these risks a less immediate concern.

Emerging-market government versus non-financial private-sector debt to GDP (as %)

Authors

Trevor Holder

Portfolio manager, Fixed Income team

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that holdings and positioning are subject to change without notice. Compared to more established economies, the value of investments in emerging markets may be subject to greater volatility, owing to differences in generally accepted accounting principles or from economic, political instability or less developed market practices.

Important information

This material is for Australian wholesale clients only and is not intended for distribution to, nor should it be relied upon by, retail clients. This information has not been prepared to take into account the investment objectives, financial objectives or particular needs of any particular person. Before making an investment decision you should carefully consider, with or without the assistance of a financial adviser, whether such an investment strategy is appropriate in light of your particular investment needs, objectives and financial circumstances.

Newton Investment Management Limited is exempt from the requirement to hold an Australian financial services licence in respect of the financial services it provides to wholesale clients in Australia and is authorised and regulated by the Financial Conduct Authority of the UK under UK laws, which differ from Australian laws.

Newton Investment Management Limited (Newton) is authorised and regulated in the UK by the Financial Conduct Authority (FCA), 12 Endeavour Square, London, E20 1JN. Newton is providing financial services to wholesale clients in Australia in reliance on ASIC Corporations (Repeal and Transitional) Instrument 2016/396, a copy of which is on the website of the Australian Securities and Investments Commission, www.asic.gov.au. The instrument exempts entities that are authorised and regulated in the UK by the FCA, such as Newton, from the need to hold an Australian financial services license under the Corporations Act 2001 for certain financial services provided to Australian wholesale clients on certain conditions. Financial services provided by Newton are regulated by the FCA under the laws and regulatory requirements of the United Kingdom, which are different to the laws applying in Australia.

Comments