Economic and market background

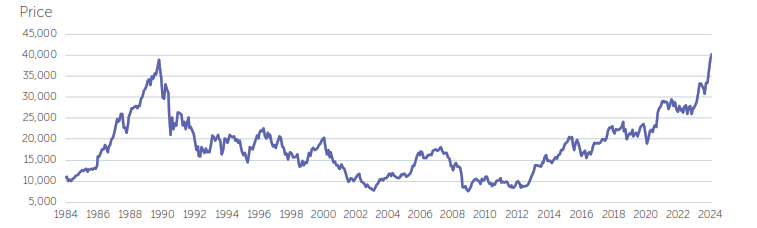

Japan became only the fifth country to land a spacecraft on the moon when its unmanned Smart Lander for Investigating Moon (SLIM) touched down on the lunar surface on 19 January, using rapid image processing and crater mapping to reach its targeted location.1 Two months later, Japan’s central bank also took a giant leap as it ended eight years of negative interest rates and made its first rate hike in 17 years. Against a backdrop of higher inflation, growing investor confidence in the country’s economy saw the Nikkei 225 index of Japanese stocks reach a record high during the quarter, surpassing the previous record from 1989.2

Nikkei 225 index

Source: FactSet, April 2024.

Most other major equity markets also made robust gains over the first three months of the year, although, in contrast to Japan, investors’ focus was on the prospect of falling rather than rising interest rates. While hopes of an economic soft landing and expectations of central-bank policy easing had been bolstered in late 2023, data releases over the opening weeks of 2024 conveyed mixed messages to market participants, leading in aggregate to a scaling back in expectations of rate cuts. In particular, US core services inflation showed signs of remaining sticky, with the consumer price index rising 0.4% in February after a 0.3% increase in January.3 The country’s labour market also appeared surprisingly resilient, with 229,000 jobs added to non-farm payrolls in January and a further 275,000 in February. However, a rise in the unemployment rate to a two-year high of 3.9% and a moderation in wage increases helped to assuage concerns that the economy was running too hot.4

Leaving interest rates unchanged at its March meeting, the US Federal Reserve (Fed) acknowledged that price pressures remained “elevated” while maintaining its projection for three rate cuts this year. However, although indicating that he believed inflation was still “moving down gradually on a sometimes bumpy road to 2%”, Fed Chair Jerome Powell signalled that the central bank would maintain high interest rates for as long as necessary. He reiterated the need for a cautious approach in light of the economy’s continued strength, and said that more data would be needed to confirm that inflation was continuing to ease before the Fed changed its policy.5

Conversely, while the European Central Bank and Bank of England also elected to keep rates on hold, the Swiss National Bank (SNB) unexpectedly cut its main interest rate by 0.25% to 1.5% at its March meeting,6 marking its first rate cut in nine years and effectively firing the starting gun for an easing cycle among large, developed economies.

With Swiss inflation having remained below the SNB’s 2% target for several months and falling to 1.2% in February, the central bank said that it was taking into account the reduced inflationary pressures, as well as seeking to support economic activity after the Swiss franc had appreciated significantly against the US dollar and euro over the last year.

The continued enthusiasm for artificial intelligence (AI) helped to fuel equity markets’ performance during the quarter, with leading technology stocks generating outsized revenue growth. But as the quarter progressed, the rally broadened, with stocks in Europe and Japan, and sectors beyond technology, also recording strong gains. China, however, did not join the party, as its continued property crisis and weak consumption, in the absence of major policy stimulus, deterred global investors.

In fixed income, government bonds came under pressure during January and February as concerns over inflation persisted and the Fed indicated that interest-rate cuts were not imminent. However, bond markets staged a recovery in March as central-bank rhetoric became more dovish. Emerging-market bonds in particular saw strong returns, as the prospect of US interest-rate cuts led to an easing of external financial conditions.

Total returns (%) to 31 March 2024

| Asset class | Index | 3 months |

| UK equities | FTSE All-Share | +3.6 |

| North American equities | FTSE World North America (£) | +11.1 |

| European ex UK equities | FTSE World Europe ex UK (£) | +6.8 |

| Japanese equities | FTSE Japan (£) | +11.6 |

| Asia-Pacific ex Japan equities | FTSE World Asia Pacific ex Japan (£) | +3.5 |

| Emerging-market equities | FTSE All-World Emerging (£) | +3.1 |

| UK gilts | FTSE Actuaries UK Conventional Gilts All Stocks | -1.6 |

| Corporate bonds | ICE BofA Sterling Non-Gilt | 0.0 |

| Overseas government bonds | JP Morgan Global Government Bond (ex UK) (£) | -1.8 |

| Gold (US$) | Gold ($/ozt SIX) | +8.1 |

| Gold (£) | Gold (£/ozt SIX) | +9.0 |

Source: FactSet, 1 April 2024. All equity market returns are sterling total returns.

Regional overview

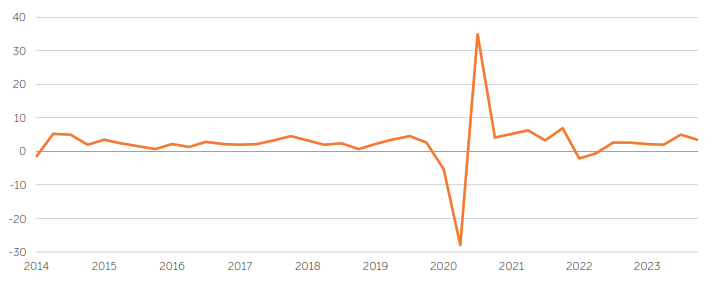

US gross domestic product (GDP ) was estimated to have grown at an annualised rate of 3.4% during the fourth quarter of 2023, well ahead of consensus expectations. The updated report released by the Bureau of Economic Analysis on 28 March painted a positive picture, with strong consumer spending and business investment in areas such as factories and health-care facilities, while corporate profits and worker productivity also increased.7

US GDP

%change, year on year

Source: FactSet, April 2024.

At its March meeting, the Fed revised up its economic projections, with the Federal Open Market Committee’s (FOMC) ‘dot plot’ projections showing that the median expectation for economic growth this year had risen to 2.1% (compared to the 1.4% forecast in December), while unemployment was projected to reach 4.0% by the end of the year, only a small increase from its current 3.9% level. Although the Fed’s preferred measure of inflation, the core personal consumption expenditures price index, is forecast to end the year at 2.6%, falling at a slower pace than previously anticipated, and the distribution of FOMC members’ ‘dots’ implied a slightly more hawkish view on future rate cuts than in December, Chair Powell did not challenge the overriding market narrative which implies a high probability of a first rate cut in June.

Like its US counterpart, the European Central Bank (ECB) stated at its March meeting that more evidence would be needed before it could begin to cut interest rates, with President Christine Lagarde saying that “we will know a lot more in June”, when wage data for the first quarter will have been published.8 The ECB expects inflation to decline to 2.3% this year, and fall back to its 2% target in 2025.

With subdued foreign demand and construction activity hindered by higher interest rates, the economy of the eurozone is forecast to expand by just 0.6% this year. However, after 10 months of contraction, a survey showed that business activity was close to returning to growth in March, with the HCOB preliminary composite purchasing managers’ index rising to 49.9 (just below the 50 level that separates growth from contraction).9 Nevertheless, any recovery looks set to be uneven. While the services sector in Germany, the eurozone’s largest economy, came close to stabilising in March, the country’s manufacturing sector was still firmly in contraction, while France, which hosts the Olympic Games this summer, saw demand for goods and services weaken and employment fall.

After a shallow recession in the second half of last year, the UK economy appeared to revive in early 2024, with modest GDP growth of 0.2% reported in January by the Office for National Statistics, boosted by housebuilding activity and retail sales, which saw their biggest jump since Covid restrictions were lifted in 2021.10

With consumer price inflation having fallen to an annualised rate of 3.4% in February, the Bank of England’s (BoE) 21 March meeting was the first time since September 2021 that none of its nine Monetary Policy Committee members had voted for an interest-rate hike.11 BoE Governor Andrew Bailey stated that “things are moving in the right direction” for rate cuts, but that further proof was required before confirming that price pressures were fully under control. The central bank believes that inflation will drop below its 2% target during the second quarter owing to the government’s decision to freeze fuel duty again. However, at around 6%, average wage growth remains elevated and higher than in the US and the eurozone, which could rekindle inflationary pressures later in the year.

The Bank of Japan’s (BoJ) decision in March to abandon negative interest rates and revert to a “normal” monetary policy came after inflation had exceeded the BoJ’s 2% target for more than a year.12 In addition, the country’s biggest companies had just agreed to raise salaries by almost 5.3% in the annual ‘shunto’ wage negotiations, the largest increase in 33 years.13 The BoJ has also ended its yield-curve control policy (a cap on bond yields), and abandoned purchases of risky assets.

However, with the BoJ continuing to buy government bonds with scope to ramp up purchases in the event of rapidly rising yields, the central bank highlighted that it expects “accommodative financial conditions to be maintained for the time being”, and the country’s fragile economic recovery and huge public debt are likely to restrict the pace of future rate hikes.

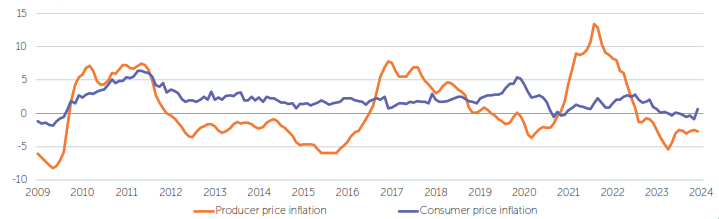

China consumer price and producer price inflation

% change, year on year

Source: FactSet, April 2024.

China has set itself an ambitious 2024 economic growth target of 5%, which looks difficult to achieve as its post-pandemic recovery has faltered. In addition to the challenges facing property developers and indebted local governments, the country is also contending with deflationary risks. In January, consumer prices fell at their steepest pace in over 14 years,14 while producer prices fell for the 15th consecutive month.15

Although China has announced moderate stimulus measures, including plans to issue 1 trillion yuan (US$139 billion) in special ultra-long term treasury bonds that could be used to fund strategically important sectors,16 it has so far avoided bolder structural reforms. The country has boosted lending to high-tech manufacturers in industries such as renewable energy, which could lead to overcapacity as well as exacerbating trade tensions with its Western counterparts, which are also wary of increased Chinese defence spending as tensions have risen over Taiwan.

Investment implications

As we enter the second quarter of 2024, financial-market participants have become increasingly comfortable with the idea that an economic slowdown, caused by high interest rates, is to be avoided, and that central banks will bring rates down in the second half of the year owing to lower inflation. The current period of disinflationary growth appears set to continue and broaden, enabling economic laggards such as Europe and China to join this ‘Goldilocks’ party.

The predictive powers of the inverted government bond yield curve to signal a recession appear to have misled investors on this occasion, as economic slowdown forecasts are being dropped faster than last year’s fashion fad. As we look back in a few years’ time, will we be able to gloss over this predictive error with the suggestion that central banks averted the slowdown by reducing rates in the second half of 2024, or will we reflect that the data has become flawed owing to the distorting events of the Covid pandemic?

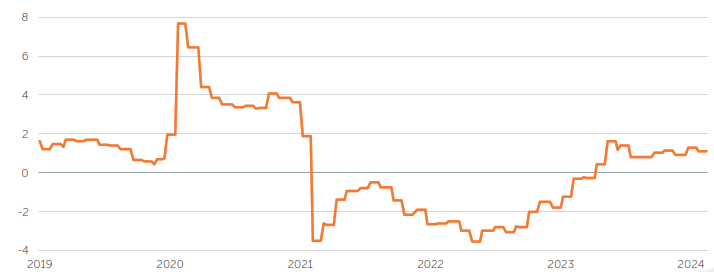

Meanwhile, economies and markets move on regardless, fed by good liquidity and a globally synchronised growth story that is driven by a new cycle of investment in changing supply lines, independent energy sources, and AI. With real wages now in positive territory in many countries, the cost-of-living crisis felt in large parts of the world during the period of high inflation should become less severe, even if for many it does not go away.

Average hourly earnings of US private employees, adjusted for inflation

% change, year on year

Source: FactSet, April 2024.

As we look across the world, we see a differentiated outlook developing for the respective economic regions.

China’s economic readjustment following its property-market collapse will be felt for some time, and the authorities will need to lean against the deflationary effects of the decline in Chinese consumers’ main store of wealth. They have continued to ease the monetary strain by progressively lowering interest rates and providing additional liquidity. While China’s trade with the US has started to slow, its trade with many other parts of the world, especially the rest of Asia, has risen. This reglobalisation story is underappreciated by many in the West. Eventually, piecemeal intervention efforts should provide a lift to China’s economy, but it is unlikely to experience the same investment-led boom of previous cycles.

The structural trend of evolving trade has helped emerging-market economies in general, while many have been boosted by an earlier decline in inflation levels, which has allowed them to lead developed markets into the easing cycle.

Elsewhere, Europe was hit particularly hard by the energy inflation shock that followed Russia’s invasion of Ukraine in 2022. Since then, the switch from reliance on Russian energy supplies to other sources has been in full swing, and a shortage has evolved into a growing oversupply situation. European inflation is still falling, alleviating some of the pressure on capital-intensive industries. The lower inflation readings should also allow the European Central Bank to join its Swiss counterpart and start to cut rates this summer.

In the US, while the ‘magnificent seven’ mega-cap technology stocks have been instrumental in propelling equity markets to new highs, their prospects look increasingly disparate. Those companies that are integral to the AI investment cycle appear stronger, while others may be more exposed to growing competition. Meanwhile, a broader recovery now appears to be in play, with the outlook also improving for smaller companies in different industries, albeit that one potential concern for the US is higher headline inflation, as the US economy is particularly vulnerable to spikes in oil prices, which have recently been on the rise once again.

For the time being, the rosy economic scenario looks set to continue into the summer, but as investors we should consider what could bring it to an end. In this context, we see two key tail risks. The first is that inflation expectations accelerate through the summer, and the interest-rate cuts that are currently priced into markets do not happen or are even replaced with the prospect of rate increases. The second scenario, which currently appears less likely, is that economies do succumb to pressure from higher interest rates, with investment slipping and unemployment starting to rise meaningfully. This slowdown scenario will become more probable should interest rates remain higher for longer or if they are expected to rise again.

Against this backdrop, it looks likely that Goldilocks investors will not be concerned about the temperature of their porridge for some time yet, but when they do, it is likely to be because it is too hot before it becomes too cold.

In this environment, government bond markets look set to be range bound, but with a tendency for a rise in yields (which move inversely to prices). As economic growth becomes more global and inflation expectations start to lift once more, we would expect yield curves to ‘disinvert’ (when the yields of longer-term bonds rise more than those of shorter-term bonds). Credit markets, meanwhile, have enjoyed the disinflationary growth period and should continue to do so for now, but may falter if fears of rising interest rates return later in the year. The same is likely to be the case for emerging-market bonds, many of which should also continue to benefit from declining domestic interest rates.

For risk assets such as equities, the broadening of economic growth should allow the rally to continue to spread from the previous market leaders to encompass a greater geographical and sectoral mix. Eventually, should inflation concerns rise, together with the prospect of higher rates, this upward trajectory may succumb to profit taking, but for now we think the outlook remains positive.

Commodities and currencies are a mixed bag. Broad global economic growth is usually bearish for the US dollar as capital flows into other markets, but the potential for the US to maintain its interest-rate advantage over other currencies for longer is keeping the greenback supported. Meanwhile, commodities are unlikely to see the same investment-led growth which drove prices higher in previous years, but a modest pickup in global demand could lift some industrial commodities from their recent lows, while geopolitical concerns could keep the demand for precious metals higher for longer.

Conclusion

The first quarter of 2024 was characterised by a globally synchronised growth narrative, with a US economy that has remained robust and the prospect of a recovery broadening out to other regions. While inflation remains above target in major developed economies, market participants’ concerns have continued to ease, with much anticipated interest-rate cuts forecast for the second half of the year.

Against this backdrop, investors can seek to capitalise on structural demand trends in growth areas such as AI and the energy transition, and as supply chains continue to be realigned.

Nevertheless, investors still face significant risks. Inflation has the potential to remain sticky or even rebound later in the year, leading to rates remaining higher for longer and heightening the prospect of an economic slowdown. Geopolitical factors, such as the conflicts in Ukraine and the Middle East, as well as continuing tensions between China and the US, could spark renewed market volatility.

In this environment, we believe it will be all the more important to avoid short-term distractions and remain focused on investing in the right securities, in the right asset classes, at the right time.

We proved that you can land wherever you want, rather than where you are able to…We opened the door to a new era.

Shinichiro Sakai, project manager of the SLIM project, Japan Aerospace Exploration Agency

1 Japan lands on Moon but glitch threatens mission, BBC News, 19 January 2024.

2 Markets in Q1: the wild ride towards rate cuts, Reuters, 29 March 2024.

3 Gasoline, shelter costs boost US prices; inflation still slowing, Reuters, 12 March 2024.

4 Feb US payrolls show labor market healthy but not overly tight, Reuters, 8 March 2024.

5 Fed sees three rate cuts in 2024 but a more shallow easing path, Reuters, 21 March 2024.

6 Swiss central bank cuts rates in surprise move, getting ahead of global peers, Reuters, 21 March 2024.

7 Gross Domestic Product, Fourth Quarter and Year 2023 (Third Estimate), GDP by Industry, and Corporate Profits, US Bureau of Economic Analysis, 28 March 2024.

8 ECB lays ground for June rate cut as inflation falls, Reuters, 7 March 2024.

9 Euro zone business activity close to stabilising in March, PMI survey shows, Reuters, 21 March 2024.

10 UK economy returns to modest growth at start of 2024, Reuters, 13 March 2024.

11 UK inflation ‘moving in right direction’ for rate cuts, Bank of England says, 21 March 2024.

12 Bank of Japan scraps radical policy, makes first rate hike in 17 years, Reuters, 19 March 2024.

13 Japan union group announces biggest wage hikes in 33 years, presaging shift at central bank, Reuters, 15 March 2024.

14 China’s consumer prices suffer biggest fall since 2009 as deflation risks stalk economy, Reuters, 8 February 2024.

15 China’s tumbling prices push some exporters to the brink, Reuters, 5 February 2024.

16 China’s parliament to unveil more stimulus this week, bold reforms unlikely, Reuters, 3 March 2024.

Download this articleAll data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important information

These opinions should not be construed as investment or other advice and are subject to change. This document is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Issued in the UK by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management Limited is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. This material may be distributed by BNY Mellon Investment Management EMEA (BNYM IM EMEA) in the UK to professional investors. BNYM IM EMEA, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023. This material is for Australian wholesale clients only and is not intended for distribution to, nor should it be relied upon by, retail clients. This information has not been prepared to take into account the investment objectives, financial objectives or particular needs of any particular person. Before making an investment decision you should carefully consider, with or without the assistance of a financial adviser, whether such an investment strategy is appropriate in light of your particular investment needs, objectives and financial circumstances. Newton Investment Management Limited is exempt from the requirement to hold an Australian financial services licence in respect of the financial services it provides to wholesale clients in Australia and is authorised and regulated by the Financial Conduct Authority of the UK under UK laws, which differ from Australian laws. Newton Investment Management Limited (Newton) is authorised and regulated in the UK by the Financial Conduct Authority (FCA), 12 Endeavour Square, London, E20 1JN. Newton is providing financial services to wholesale clients in Australia in reliance on ASIC Corporations (Repeal and Transitional) Instrument 2016/396, a copy of which is on the website of the Australian Securities and Investments Commission, www. asic.gov.au. The instrument exempts entities that are authorised and regulated in the UK by the FCA, such as Newton, from the need to hold an Australian financial services license under the Corporations Act 2001 for certain financial services provided to Australian wholesale clients on certain conditions. Financial services provided by Newton are regulated by the FCA under the laws and regulatory requirements of the United Kingdom, which are different to the laws applying in Australia. MAR006069