Key points

- Donald Trump’s trade tariffs are widely expected by the market to be inflationary.

- But are tariffs more of a bargaining tool for ‘dealmaker’ Trump than a strong inflationary force? Could deglobalisation keep inflation higher than during the last decade?

- Policy uncertainty could potentially cause an economic slowdown in the short term; however, Trump’s deregulatory stance could provide a boost to the US economy as well as the banking and energy sectors.

US President Donald Trump’s trade tariffs are widely expected to have an inflationary effect on the US domestic economy. However, rather than being outright inflationary, we think tariffs are more of a bargaining tool for Trump to achieve certain fiscal objectives. This has led to an increase in policy uncertainty, which could lead to slower economic activity.

Since his inauguration, Trump has imposed tariffs of 25% on imports from Canada and Mexico,[1] and 20% on imports from China.[2] He has also threatened tariffs on the European Union and committed to so-called reciprocal tariffs on a range of other countries.[3] The fear is that tariffs could ramp up the cost of goods for US importers who could pass these on to retailers and, in turn, to end consumers.

Nevertheless, while we believe there are certainly inflationary forces at play in the global economy, such as secular drivers like deglobalisation and decarbonisation, our views on tariffs as a contributing factor are more sanguine. We do not think tariffs will be as inflationary as the market fears.

We do not think tariffs will be as inflationary as the market fears.

External revenue

As part of this deal making, we would highlight Trump’s rhetoric on creating an “external revenue service.” [4] The intention of this is to collect tariffs, duties and revenue from foreign sources to relieve the tax burden on internal sources, i.e. domestic companies.

Trump believes there should be an external revenue service. When it comes to renegotiating tax policy in 2025, we could see tariffs as part of that package – the idea being to generate more revenue from external partners, maybe through broader tariffs, at the same time as cutting taxes internally.

It is indeterminate whether this is inflationary or not, so we are not convinced that tariffs overall will be inflationary. However, we do believe that interest rates around current levels probably make sense for the economy and the yield curve may be a little steeper. Importantly, it has led to policy uncertainty which could potentially lead to an economic downturn in the short term.

Banks

As well as imposing tariffs, Trump is seeking to roll back regulation across a wide range of industries. This has been evidenced by a flurry of executive orders since his inauguration, tackling areas including government spending, defence, immigration and climate.[5]

Banking is another sector that we believe could come under Trump’s deregulatory lens. Prior to Trump’s inauguration, the Federal Reserve announced a cut to a proposed increase to capital requirements under the Basel III regulation.[6] But we think there is a possibility that the Trump administration could water this down further.[7]

During the 2008 global financial crisis, more regulation was required and the banks needed more capital. They have spent over a decade building capital levels and the banks in the US, especially the large banks, are now in very good shape.

If capital requirements are indeed left untouched, we believe financial stocks could help stimulate the economy through increased lending activity. They could also return more capital to shareholders in the form of dividends.

If capital requirements are indeed left untouched, we believe financial stocks could help stimulate the economy through increased lending activity.

Energy

Energy is another sector potentially in line for a cutback in regulation. Trump’s ‘drill, baby, drill’ pledge could increase the domestic supply of oil and natural gas but that could be offset by a tougher diplomatic stance on Iran and Venezuela, restricting supply. [8][9] When you net these two forces, the oil price and natural-gas price appear to be favourable at their current levels.

We are positive on natural-gas players because of the huge electricity demand needed in the US to support the manufacturing renaissance that Trump is seeking to enable through lower taxes on domestic companies. We see this trend continuing.

We would also caution investors about getting too excited about a coming surge in US energy supply. Trump telling the energy companies to ramp up production is like ‘pushing on a string’. Many of these companies have become much more disciplined over the last decade and have increasingly focused on returning capital to shareholders through dividends and buybacks as opposed to increasing production. We believe this is positive for dividend investors.

[1] FT. Donald Trump confirms he will impose 25% tariffs on Mexico and Canada on Tuesday. 3 March 2025.

[2] FT. US to raise tariffs on China and push ahead with Canada and Mexico levies. 28 February 2025.

[3] FT. Donald Trump threatens to impose 25% tariffs on EU goods. 26 February 2025

[4] Guardian. Trump says he will create ‘external revenue service’ to collect tariff income. 14 January 2025.

[5] BBC. What has Trump done since taking power. 29 January 2025.

[6] FT. Federal Reserve halves proposed capital requirement rise for largest US banks. 10 September 2024.

[7] The Banker. Further Basel delays expected as UK and EU wait on Trump. 20 January 2025.

[8] BBC. Trump vows to leave Paris climate agreement and ‘drill, baby, drill’. 21 January 2025.

[9] The National. Trump-led US may tighten oil markets with stricter sanctions on Iran and Venezuela. 6 November 2024.

Key Points

- Donald Trump’s trade tariffs are widely expected by the market to be inflationary.

- But are tariffs more of a bargaining tool for ‘dealmaker’ Trump than a strong inflationary force? Could deglobalization keep inflation higher than during the last decade?

- Policy uncertainty could potentially cause an economic slowdown in the short term; however, Trump’s deregulatory stance could provide a boost to the US economy as well as the banking and energy sectors.

Donald Trump’s trade tariffs are widely expected to have an inflationary effect on the domestic economy. However, rather than being outright inflationary, we think tariffs are more of a bargaining tool for Trump to achieve certain fiscal objectives. This has led to an increase in policy uncertainty, which could lead to slower economic activity.

Since his inauguration, Trump has imposed tariffs of 25% on imports from Canada and Mexico,[1] and 20% on imports from China.[2] He has also threatened tariffs on the European Union and committed to so-called reciprocal tariffs on a range of other countries.[3] The fear is that tariffs could ramp up the cost of goods for US importers who could pass these on to retailers and, in turn, to end consumers.

Nevertheless, while we believe there are certainly inflationary forces at play in the global economy, such as secular drivers like deglobalization and decarbonization, our views on tariffs as a contributing factor are more sanguine. We do not think tariffs will be as inflationary as the market fears.

We do not think tariffs will be as inflationary as the market fears.

External Revenue

As part of this deal making, we would highlight Trump’s rhetoric on creating an “external revenue service.” [4] The intention of this is to collect tariffs, duties and revenue from foreign sources to relieve the tax burden on internal sources, i.e. domestic companies.

Trump believes there should be an external revenue service. When it comes to renegotiating tax policy in 2025, we could see tariffs as part of that package – the idea being to generate more revenue from external partners, maybe through broader tariffs, at the same time as cutting taxes internally.

It is indeterminate whether this is inflationary or not, so we are not convinced that tariffs overall will be inflationary. However, we do believe that interest rates around current levels probably make sense for the economy and the yield curve may be a little steeper. Importantly, it has led to policy uncertainty which could potentially lead to an economic downturn in the short term.

Banks

As well as imposing tariffs, Trump is seeking to roll back regulation across a wide range of industries. This has been evidenced by a flurry of executive orders since his inauguration, tackling areas including government spending, defense, immigration and climate.[5]

Banking is another sector that we believe could come under Trump’s deregulatory lens. Prior to Trump’s inauguration, the Federal Reserve announced a cut to a proposed increase to capital requirements under the Basel III regulation.[6] But we think there is a possibility that the Trump administration could water this down further.[7]

During the 2008 global financial crisis, more regulation was required and the banks needed more capital. They have spent over a decade building capital levels and the banks in the US, especially the large banks, are now in very good shape.

If capital requirements are indeed left untouched, we believe financial stocks could help stimulate the economy through increased lending activity. They could also return more capital to shareholders in the form of dividends.

If capital requirements are indeed left untouched, we believe financial stocks could help stimulate the economy through increased lending activity.

Energy

Energy is another sector potentially in line for a cutback in regulation. Trump’s “drill, baby, drill” pledge could increase the domestic supply of oil and natural gas but that could be offset by a tougher diplomatic stance on Iran and Venezuela, restricting supply. [8][9] When you net these two forces, the oil price and natural-gas price appear to be favorable at their current levels.

We are positive on natural-gas players because of the huge electricity demand needed in the US to support the manufacturing renaissance that Trump is seeking to enable through lower taxes on domestic companies. We see this trend continuing.

We would also caution investors about getting too excited about a coming surge in US energy supply. Trump telling the energy companies to ramp up production is like ‘pushing on a string.’ Many of these companies have become much more disciplined over the last decade and have increasingly focused on returning capital to shareholders through dividends and buybacks as opposed to increasing production. We believe this is positive for dividend investors.

[1] FT. Donald Trump confirms he will impose 25% tariffs on Mexico and Canada on Tuesday. March 3, 2025.

[2] FT. US to raise tariffs on China and push ahead with Canada and Mexico levies. February 28, 2025.

[3] FT. Donald Trump threatens to impose 25% tariffs on EU goods. February 26, 2025

[4] Guardian. Trump says he will create ‘external revenue service’ to collect tariff income. January 14, 2025.

[5] BBC. What has Trump done since taking power. January 29, 2025.

[6] FT. Federal Reserve halves proposed capital requirement rise for largest US banks. September 10, 2024.

[7] The Banker. Further Basel delays expected as UK and EU wait on Trump. January 20, 2025.

[8] BBC. Trump vows to leave Paris climate agreement and ‘drill, baby, drill’. January 21, 2025.

[9] The National. Trump-led US may tighten oil markets with stricter sanctions on Iran and Venezuela. November 6, 2024.

Key points

- Growth stocks have posted outsized returns, but a changing economic outlook and elevated valuations could limit future gains.

- Slowing earnings-growth momentum and concerns about lofty valuations lead us to reiterate our view that investors should rebalance toward value-oriented stocks.

- We believe companies with strong and improving fundamentals, attractive valuations and business momentum will prove to be solid investment opportunities and lead to better investment outcomes for our clients.

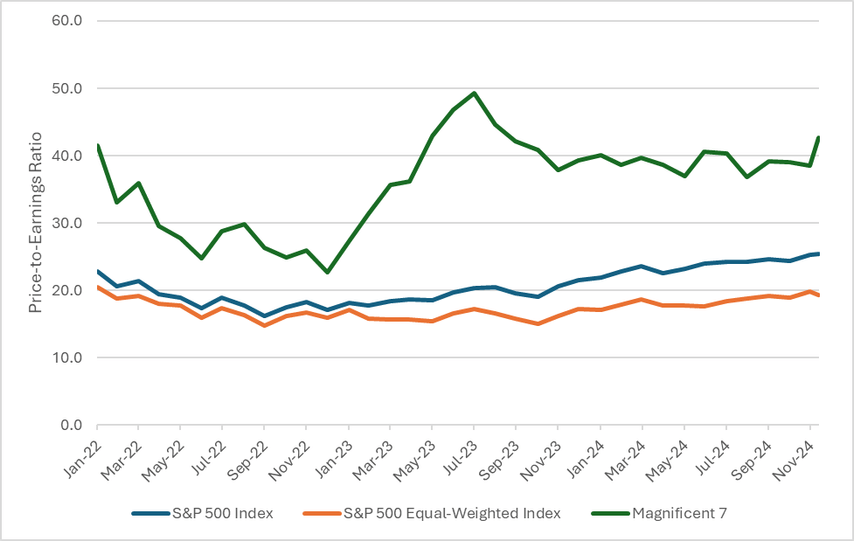

In late 2024, we made a case for US large-cap value investing in The Time Is (Always) Right for Value Investing. We believed that a return to a pre-2008 global financial crisis macro environment would normalize growth/value performance. Second, we observed a rising concentration risk, as equity markets—and investor portfolios—were increasingly exposed to the “magnificent seven” (M7), a narrow group of expensive large-cap growth stocks. We argued for rebalancing, rather than fully rotating, toward US large-cap value as we did not see an obvious catalyst for a change in market leadership.

In our 2025 outlook, we reiterated our recommendation to rebalance as the supporting factors were unchanged in our view. Today, however, we are seeing evidence that some of the key drivers of growth leadership, such as aggressive US monetary-policy easing and US leadership in artificial intelligence (AI) development, are softening. This has led to large cap growth’s performance lagging value year to date. While this period is short, it emphasizes the importance of maintaining a balanced allocation to include US large-cap value.

Investors Starting to Embrace “Higher for Longer”

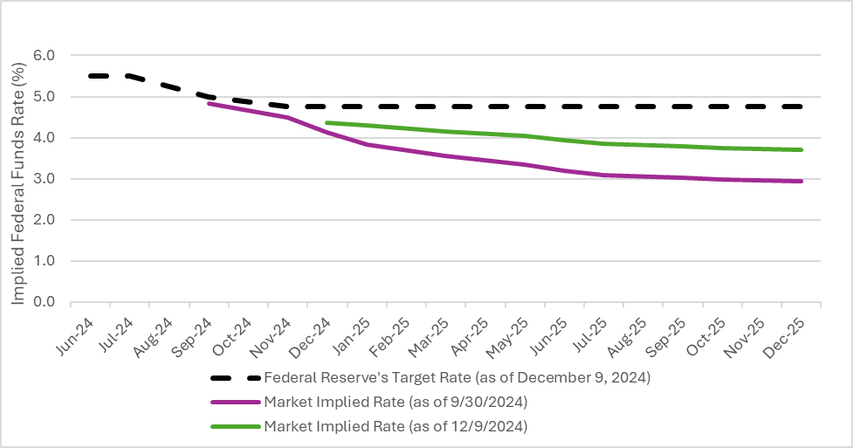

Already in 2025, the Federal Reserve (Fed) held its January meeting and Fed Chair Powell appeared before Congress in February for his semiannual testimony. In both instances, he reiterated that the central bank “doesn’t need to rush to adjust interest rates” and would be “patient before lowering borrowing costs further.” The Fed’s message was quickly reflected in market-based expectations.

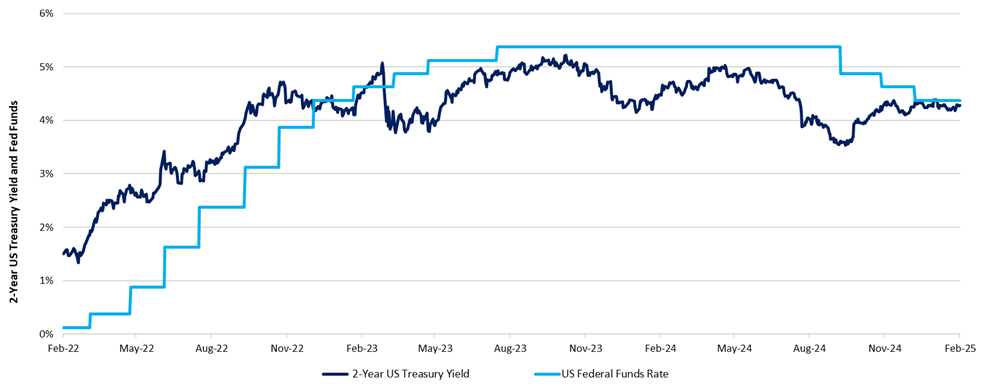

As the chart below illustrates, the 2-year US Treasury yield, which traded below the fed funds rate for over a year on the expectation that interest rates would be moving lower imminently, has recently converged with the fed funds rate.

US Federal Funds Rate vs US 2-year Treasury Yield

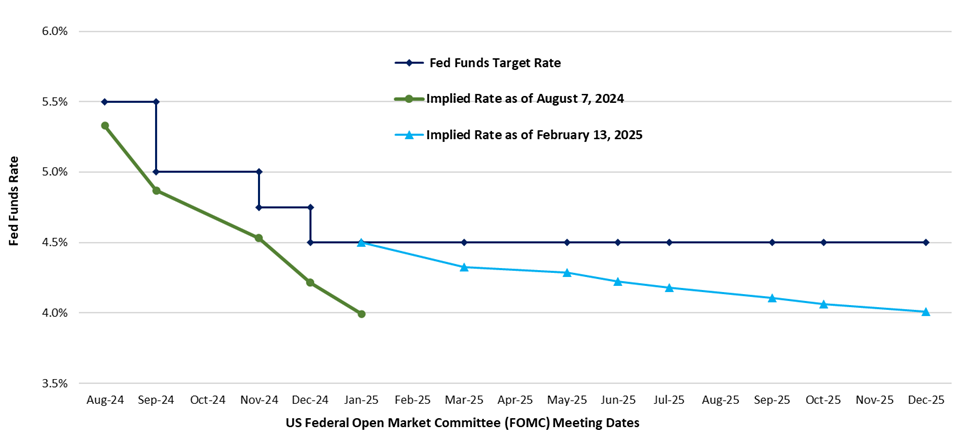

In addition, the market-implied fed funds rate indicates that investors now expect rates to fall later and less than previously thought. In August 2024, the market expected the rate to be 4% by January 2025. However, following the January Fed meeting and Chair Powell’s February testimony, the market now anticipates reaching 4% by December 2025, almost a full year later.

Current Federal Funds Rate vs Market Implied Federal Funds Rate

Changes in interest-rate expectations have typically been a big driver of relative style performance, but it has been particularly pronounced since the global financial crisis. The Fed’s low- and zero-interest rate policy helped growth outperform value in the 12 years leading up to the Covid-19 pandemic, and again after inflation peaked in 2022. With interest-rate expectations beginning to reflect the Fed’s higher-for-longer stance, we think value-oriented securities are poised to deliver competitive returns relative to growth.

Magnificent Seven Taking a Breather?

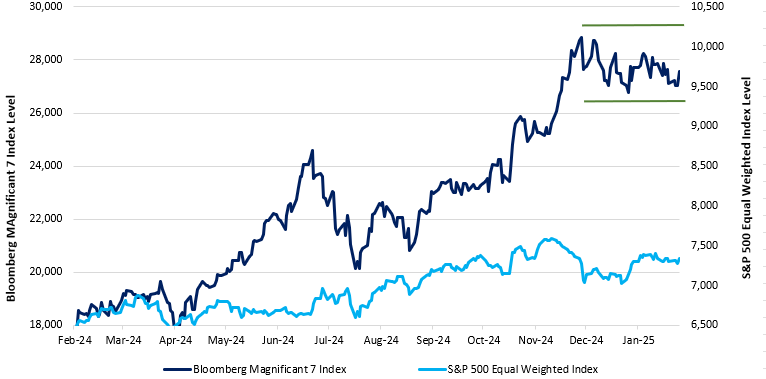

US equity market gains over the past year were driven primarily by the M7. More recently, a subset has separated themselves owing to their leadership in AI innovation, development and spending. Lately, however, these stocks have taken a bit of a breather as investors review their assumptions about US leadership in AI. The key catalyst for this was the emergence of Chinese AI developer DeepSeek, which boasted a new platform that is reportedly more economic and energy-efficient than its US counterparts.

One-Year Performance of the Magnificent Seven vs the S&P 500® Equal-Weighted Index

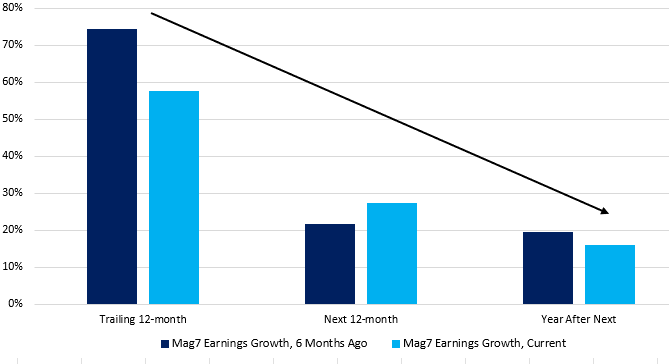

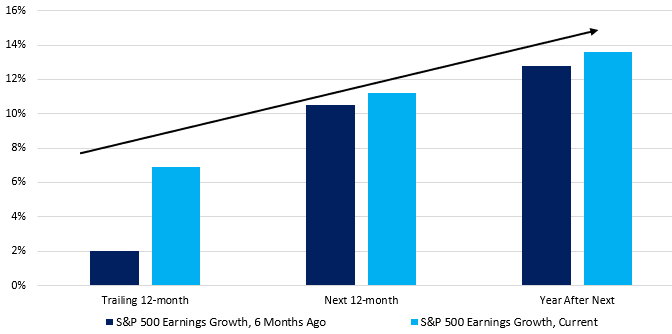

Investors are likely to further scrutinize the M7 companies’ future earnings growth to determine if expected earnings can still support lofty valuations. Looking at the earnings data through the end of January, this pause among the M7 seems warranted. As the chart below illustrates, earnings growth, while still relatively strong, is forecast to decelerate over the coming year.

Earnings Growth Still Strong, but Decelerating

Meanwhile, earnings growth for the broader market is being revised higher from where consensus expected it six months ago and looks set to accelerate higher through 2026, which would support the case to balance out exposure beyond a small set of companies.

Earnings Growth Accelerating

Conclusion

We believe companies and investors continue to adjust to US inflation and interest rates normalizing—not to pre-Covid levels, but to those before the global financial crisis. We expect inflation to remain higher and more persistent than in the previous 12 years, likely prompting the Fed to keep rates elevated. The macro environment, combined with concentration risk in the M7 stocks, changing momentum in earnings growth and concerns about lofty valuations, leads us to reiterate our view that investors should rebalance toward value-oriented stocks. Within the value space, we believe companies with strong and improving fundamentals, attractive valuations and business momentum will prove to be solid investment opportunities and lead to better investment outcomes for our clients. We think our consistent and repeatable investment process is well suited to identify these types of opportunities.

Key points

- DeepSeek’s advancements represent continued innovation in the artificial intelligence (AI) theme and reinforce prospects for lower pricing.

- We expect model competition to remain intense.

- Lower pricing should support new application development; likewise, we believe that innovative software and internet companies may lead the next wave of growth in the theme.

- Longer term, enterprises that embrace AI first may have an edge in differentiating their products and services and may outperform their competitors.

China-based startup DeepSeek took the markets by storm recently, igniting a broad sell-off in US technology stocks with the launch of DeepSeek-R1, the most recent iteration of its generative artificial-intelligence (AI) model. The R1 model has quickly risen in popularity, propelling to the top of the US Apple App Store’s free applications, where it surpassed competitors like OpenAI’s ChatGPT.

DeepSeek has attracted significant attention for its cost-effective and innovative AI approach. This has prompted swirling concerns that the Chinese AI company was able to achieve its efficiencies and high-performance results using less advanced hardware, potentially circumventing US export controls on high-end AI chips.

DeepSeek’s success challenges the prevailing notion that larger models and more computational resources are essential for AI advancement. Ultimately, if DeepSeek’s claims are true and large language models (LLMs) can be trained with fewer AI chips at a fraction of the cost of competitors’ models, there are a myriad of investment implications to consider. Investors fear this could reduce demand for advanced AI chips, as well as for large-scale data centres and extensive power production to support models. While we believe that lower development costs could pose challenges for hardware and semiconductor companies in the medium term, we see greater development and growth opportunities for hyperscalers, software companies and AI consumers beyond the technology sector.

The geopolitical race for innovation

DeepSeek’s AI chatbot was released as an open-source model, meaning its source code is publicly available, so users can customise and distribute it as they see fit, subject to the open-source license. The Chinese startup claims to have trained the chatbot for under $6 million, substantially less than US tech giants have spent on similar models. DeepSeek also claims that it used far fewer and lower-grade chips than its American competitors, thereby building a product that rivals counterparts despite US efforts to restrict exports of semiconductor manufacturing equipment to China.

The DeepSeek story highlights the massive geopolitical race at play for AI dominance and the intensifying competition between the West and China. Should global markets be worried about China’s next big move? China has seemingly demonstrated that when companies release groundbreaking LLMs, it can produce cheaper, albeit slightly less performant, versions. If powerful AI models can be built without the most advanced hardware, high-end chip producers could take a hit.

In our view, we should be prepared for disruption on both the supply side and demand side, and not just from China. For instance, OpenAI has since unveiled new innovations that demonstrate fresh capabilities in driving leading-edge research efforts. Based on past technology cycles, recent news coverage highlights how the theme should continue to evolve at a rapid rate. Investors should anticipate that these advancements may usher in lower prices that could spark the elasticity required to drive new applications and the next wave of growth.

In our view, we should be prepared for disruption on both the supply side and demand side, and not just from China.

Intense competition for model development

While DeepSeek’s ultimate cost structure remains in question, we expect the competitive environment for models to remain intense. We believe this competition should foster lower pricing and drive elasticity, creating new markets that support further long-term growth in the theme.

Despite the prospects for lower cost models and rapid price declines, earnings results continue to highlight rising capital expenditures (capex) from hyperscalers in 2025. We continue to see rapid innovation and expect more companies to move workloads into the cloud to leverage these advancements.

But what does this ultimately mean for data-centre capex, and especially for the energy complex? Based on a comprehensive data-centre tracker built by our research associates, we believe capital spending intentions in the near time are robust, if not improving; several hyperscalers boosted capex in their recent earnings announcements. Some of that rise in capital spending is reportedly for investments in long-lived assets, including land and buildings in new regions, and therefore not indicative of an overbuild in compute capacity. Also, as AI matures, more countries are developing sovereign AI strategies that require new data centres in regions where considerable up-front infrastructure investment boosts capital spending on an interim basis.

A myriad of investment implications

Hyperscalers and software

Based on comments made by two influential US tech companies, we believe it is safe to assume that DeepSeek realised at least some cost advantage in building its model. If this is accurate and the cost of building models drops substantially, we believe that hyperscalers and software companies are likely to benefit.

Lower capital intensity equates to higher returns, and we generally think this dynamic bodes well for hyperscalers. Hence, our view on hyperscalers continues to be positive, though we favour those that are less focused on being vertically integrated. Hyperscalers are driven by compounding growth in data and applications, and we believe lower capital costs support that growth algorithm. Additionally, US hyperscalers could become security gatekeepers, which may reinforce the moat of these large companies as geopolitical forces potentially further ration AI technology between the West and the East.

We also believe these developments may boost certain software companies. We have a positive outlook on infrastructure software providers that deliver tools and applications used in developing AI products. Our view is also favourable on application software and internet companies that may embed AI into their products and services. Edge computing companies may also benefit as lower cost and faster inferencing at the edge becomes more compelling.

Late last year, prior to DeepSeek’s recent announcement, our research analysts had expressed their bullish take on consumption software, owing to improved comparables and a desire to bet on more AI application development in 2025. Additionally, during research visits in December, our analysts gathered evidence that more companies believed that their AI products were ready to ship. Assuming that DeepSeek’s claims are true, the Jevon’s paradox argument—which suggests that increased efficiency can lead to increased demand—crystalises our positive view of software in 2025; if hardware costs are coming down to train LLMs and to ship them and for the increased adoption of AI products, there should be more AI products shipping in 2025 and 2026.

Hardware and semiconductors

On hardware and semiconductors, we are a bit more guarded as we believe the risk to both sectors has increased over the medium term.

On the hardware front, we have uncertainty around whether a significant reduction in compute costs would lead to a proportional increase in demand on a shorter-term basis. Lower capital intensity may yield excess compute capacity for a period of time before demand elasticity kicks in.

Beyond technology

AI is a foundational technology capable of reshaping various industries and the economy over time. AI technology has expansive potential beyond traditional chatbots. Tech giants and others are exploring broader AI applications, including autonomous vehicles, robotics and digital twins. We believe that many of the biggest winners from the AI theme are likely to be the companies that apply it in non-technology industries, e.g., in manufacturing, health care and financials. These companies are likely to use declining costs of AI innovation to pull those applications in to propel revenue growth.

Longer term, AI-driven labour automation and the cost advantage for companies adopting AI pose risks to jobs in certain industries, including sales, marketing and administrative functions. In our view, companies that have higher costs in those areas relative to their peers may disproportionately benefit from the adoption of AI, unfortunately at the expense of workers.

We harness our multidimensional research capabilities to help us identify potential winners within and beyond the tech ecosystem, while understanding broader investment implications.

Regulatory and geopolitical policy changes

We are monitoring the regulatory and geopolitical environment for potential policy moves that may shift competitive advantages and prompt changes to fundamentals.

For instance, the construction of data centres in the European Union is driven by stringent regulations aimed at protecting European consumer data. Despite potential shifts in AI models, the core need for secure data storage remains unchanged. This regulatory environment necessitates a proactive approach to monitor and adapt to new policies, ensuring that businesses can navigate these changes effectively.

In US regulatory developments, President Trump issued an executive order in January aiming to reduce regulations and accelerate progress in AI. Trump’s order rescinded former President Biden’s 2023 executive order that sought to tighten regulations on advanced computer chips, potentially restricting shipments of AI chips to certain countries beyond US allies. While we expect the political and regulatory environment to remain dynamic, we expect AI companies to remain under increased scrutiny regarding their compliance with export restrictions and operational transparency.

Cyber risks are also a key consideration, as downloading AI applications can introduce new avenues for cyber attacks. Social risks, including trust and misinformation, are also heightened in this context. As regulatory developments continue to unfold, it is crucial for investors to stay informed and prepared for the evolving challenges and opportunities.

The ever-evolving AI industry

At Newton, we utilise our global multidimensional research capabilities to stay abreast of the latest technology innovations, in China and elsewhere. In the case of DeepSeek, our fundamental research analysts have been assessing the credibility of headlines and the potential impact of news on hardware, software, power generation and power infrastructure investments. Our quantitative team has identified 21 past instances since 1990 when top constituents of the S&P 500 were down 15% or more in one day; they have been examining those instances to assess what the past might reveal about future market performance. Members of our specialist team have consulted with a former director for China economics on the White House National Security Council; they have reviewed media interviews by the hedge fund sponsoring DeepSeek to evaluate the credibility of the claims and assess the geopolitical implications.

DeepSeek’s latest innovation highlights the dynamic and rapidly evolving nature of AI technology. The competitive landscape is intensifying, and as companies continue to innovate and adapt, the potential for lower costs and increased efficiency could drive new applications and growth opportunities across various industries. Investors should remain vigilant and prepared for the ongoing changes likely to shape the future of AI and its impact on the global market.

Key Points

- DeepSeek’s advancements represent continued innovation in the artificial intelligence (AI) theme and reinforce prospects for lower pricing.

- We expect model competition to remain intense.

- Lower pricing should support new application development; likewise, we believe that innovative software and internet companies may lead the next wave of growth in the theme.

- Longer term, enterprises that embrace AI first may have an edge in differentiating their products and services and may outperform their competitors.

China-based startup DeepSeek took the markets by storm recently, igniting a broad sell-off in US technology stocks with the launch of DeepSeek-R1, the most recent iteration of its generative artificial-intelligence (AI) model. The R1 model has quickly risen in popularity, propelling to the top of the US Apple App Store’s free applications, where it surpassed competitors like OpenAI’s ChatGPT.

DeepSeek has attracted significant attention for its cost-effective and innovative AI approach. This has prompted swirling concerns that the Chinese AI company was able to achieve its efficiencies and high-performance results using less advanced hardware, potentially circumventing US export controls on high-end AI chips.

DeepSeek’s success challenges the prevailing notion that larger models and more computational resources are essential for AI advancement. Ultimately, if DeepSeek’s claims are true and large language models (LLMs) can be trained with fewer AI chips at a fraction of the cost of competitors’ models, there are a myriad of investment implications to consider. Investors fear this could reduce demand for advanced AI chips, as well as for large-scale data centers and extensive power production to support models. While we believe that lower development costs could pose challenges for hardware and semiconductor companies in the medium term, we see greater development and growth opportunities for hyperscalers, software companies and AI consumers beyond the technology sector.

The Geopolitical Race for Innovation

DeepSeek’s AI chatbot was released as an open-source model, meaning its source code is publicly available, so users can customize and distribute it as they see fit, subject to the open-source license. The Chinese startup claims to have trained the chatbot for under $6 million, substantially less than US tech giants have spent on similar models. DeepSeek also claims that it used far fewer and lower-grade chips than its American competitors, thereby building a product that rivals counterparts despite US efforts to restrict exports of semiconductor manufacturing equipment to China.

The DeepSeek story highlights the massive geopolitical race at play for AI dominance and the intensifying competition between the West and China. Should global markets be worried about China’s next big move? China has seemingly demonstrated that when companies release groundbreaking LLMs, it can produce cheaper, albeit slightly less performant, versions. If powerful AI models can be built without the most advanced hardware, high-end chip producers could take a hit.

In our view, we should be prepared for disruption on both the supply side and demand side, and not just from China. For instance, OpenAI has since unveiled new innovations that demonstrate fresh capabilities in driving leading-edge research efforts. Based on past technology cycles, recent news coverage highlights how the theme should continue to evolve at a rapid rate. Investors should anticipate that these advancements may usher in lower prices that could spark the elasticity required to drive new applications and the next wave of growth.

In our view, we should be prepared for disruption on both the supply side and demand side, and not just from China.

Intense Competition for Model Development

While DeepSeek’s ultimate cost structure remains in question, we expect the competitive environment for models to remain intense. We believe this competition should foster lower pricing and drive elasticity, creating new markets that support further long-term growth in the theme.

Despite the prospects for lower cost models and rapid price declines, earnings results continue to highlight rising capital expenditures (capex) from hyperscalers in 2025. We continue to see rapid innovation and expect more companies to move workloads into the cloud to leverage these advancements.

But what does this ultimately mean for data-center capex, and especially for the energy complex? Based on a comprehensive data-center tracker built by our research associates, we believe capital spending intentions in the near time are robust, if not improving; several hyperscalers boosted capex in their recent earnings announcements. Some of that rise in capital spending is reportedly for investments in long-lived assets, including land and buildings in new regions, and therefore not indicative of an overbuild in compute capacity. Also, as AI matures, more countries are developing sovereign AI strategies that require new data centers in regions where considerable up-front infrastructure investment boosts capital spending on an interim basis.

A Myriad of Investment Implications

Hyperscalers and Software

Based on comments made by two influential US tech companies, we believe it is safe to assume that DeepSeek realized at least some cost advantage in building its model. If this is accurate and the cost of building models drops substantially, we believe that hyperscalers and software companies are likely to benefit.

Lower capital intensity equates to higher returns, and we generally think this dynamic bodes well for hyperscalers. Hence, our view on hyperscalers continues to be positive, though we favor those that are less focused on being vertically integrated. Hyperscalers are driven by compounding growth in data and applications, and we believe lower capital costs support that growth algorithm. Additionally, US hyperscalers could become security gatekeepers, which may reinforce the moat of these large companies as geopolitical forces potentially further ration AI technology between the West and the East.

We also believe these developments may boost certain software companies. We have a positive outlook on infrastructure software providers that deliver tools and applications used in developing AI products. Our view is also favorable on application software and internet companies that may embed AI into their products and services. Edge computing companies may also benefit as lower cost and faster inferencing at the edge becomes more compelling.

Late last year, prior to DeepSeek’s recent announcement, our research analysts had expressed their bullish take on consumption software, owing to improved comparables and a desire to bet on more AI application development in 2025. Additionally, during research visits in December, our analysts gathered evidence that more companies believed that their AI products were ready to ship. Assuming that DeepSeek’s claims are true, the Jevon’s paradox argument—which suggests that increased efficiency can lead to increased demand—crystalizes our positive view of software in 2025; if hardware costs are coming down to train LLMs and to ship them and for the increased adoption of AI products, there should be more AI products shipping in 2025 and 2026.

Hardware and Semiconductors

On hardware and semiconductors, we are a bit more guarded as we believe the risk to both sectors has increased over the medium term.

On the hardware front, we have uncertainty around whether a significant reduction in compute costs would lead to a proportional increase in demand on a shorter-term basis. Lower capital intensity may yield excess compute capacity for a period of time before demand elasticity kicks in.

Beyond Technology

AI is a foundational technology capable of reshaping various industries and the economy over time. AI technology has expansive potential beyond traditional chatbots. Tech giants and others are exploring broader AI applications, including autonomous vehicles, robotics and digital twins. We believe that many of the biggest winners from the AI theme are likely to be the companies that apply it in non-technology industries, e.g., in manufacturing, health care and financials. These companies are likely to use declining costs of AI innovation to pull those applications in to propel revenue growth.

Longer term, AI-driven labor automation and the cost advantage for companies adopting AI pose risks to jobs in certain industries, including sales, marketing and administrative functions. In our view, companies that have higher costs in those areas relative to their peers may disproportionately benefit from the adoption of AI, unfortunately at the expense of workers.

We harness our multidimensional research capabilities to help us identify potential winners within and beyond the tech ecosystem, while understanding broader investment implications.

Regulatory and Geopolitical Policy Changes

We are monitoring the regulatory and geopolitical environment for potential policy moves that may shift competitive advantages and prompt changes to fundamentals.

For instance, the construction of data centers in the European Union is driven by stringent regulations aimed at protecting European consumer data. Despite potential shifts in AI models, the core need for secure data storage remains unchanged. This regulatory environment necessitates a proactive approach to monitor and adapt to new policies, ensuring that businesses can navigate these changes effectively.

In US regulatory developments, President Trump issued an executive order in January aiming to reduce regulations and accelerate progress in AI. Trump’s order rescinded former President Biden’s 2023 executive order that sought to tighten regulations on advanced computer chips, potentially restricting shipments of AI chips to certain countries beyond US allies. While we expect the political and regulatory environment to remain dynamic, we expect AI companies to remain under increased scrutiny regarding their compliance with export restrictions and operational transparency.

Cyber risks are also a key consideration, as downloading AI applications can introduce new avenues for cyber attacks. Social risks, including trust and misinformation, are also heightened in this context. As regulatory developments continue to unfold, it is crucial for investors to stay informed and prepared for the evolving challenges and opportunities.

The Ever-Evolving AI Industry

At Newton, we utilize our global multidimensional research capabilities to stay abreast of the latest technology innovations, in China and elsewhere. In the case of DeepSeek, our fundamental research analysts have been assessing the credibility of headlines and the potential impact of news on hardware, software, power generation and power infrastructure investments. Our quantitative team has identified 21 past instances since 1990 when top constituents of the S&P 500 were down 15% or more in one day; they have been examining those instances to assess what the past might reveal about future market performance. Members of our specialist team have consulted with a former director for China economics on the White House National Security Council; they have reviewed media interviews by the hedge fund sponsoring DeepSeek to evaluate the credibility of the claims and assess the geopolitical implications.

DeepSeek’s latest innovation highlights the dynamic and rapidly evolving nature of AI technology. The competitive landscape is intensifying, and as companies continue to innovate and adapt, the potential for lower costs and increased efficiency could drive new applications and growth opportunities across various industries. Investors should remain vigilant and prepared for the ongoing changes likely to shape the future of AI and its impact on the global market.

Key Points

- We continue to see the potential for volatility, with rising inflationary pressures, geopolitical risks and monetary policy acting as key factors shaping market dynamics.

- Companies that pay and grow dividends tend to be more resilient in downturns as investors seek stability in uncertain times.

- As the market evolves, we will remain focused on delivering steady income and growth potential, ensuring we are prepared for what the year ahead may bring.

2024 has been characterized by pronounced volatility, affecting everything from interest-rate fluctuations and inflation expectations to the economic implications of artificial intelligence and shifting political landscapes. Heading into 2025, much of this uncertainty is likely to persist. With inflation remaining above pre-pandemic levels and geopolitical tensions continuing, the market faces continued dislocation. Amid these challenges, we remain steadfast in our balanced, risk-adjusted and dividend-focused approach, which is designed to deliver stability and competitive returns in volatile environments.

Inflation Unfolding

From a global perspective, the current environment is characterized by disinflationary growth, with inflation rates decreasing from the peak levels of 2022. However, there are concerns that inflation could pick up again in 2025, primarily due to President-elect Trump’s anticipated tariffs and their impact on the prices of goods and services. We anticipate that inflation should remain above consensus expectations, gradually rising from mid-2025 and ending the year between 2.5% and 3%.

The Second Act: A Stage Set for Uncertainty

Trump’s second term introduces additional ambiguity surrounding the future of interest-rate adjustments. While Jerome Powell remains Federal Reserve (Fed) Chair until 2026, Trump’s proposed policies could complicate interest-rate positioning for the central bank. We believe the Fed will largely overlook the increase in inflation, particularly if there is no substantial response from wages, indicating no second-round effects.

The market has already begun pricing in fewer interest-rate cuts as pro-growth policies could slow the rate-cutting process. We foresee the Fed’s cutting cycle in 2025 to be shallow and potentially paused early, with the federal funds rate likely settling around 3.75-4% by year end, aligning with current market pricing. We expect 10-year yields to trade near 4.5%, above the consensus forecast of 4.1%.

The risks to inflation and yields hinge on economic growth trends. If disinflationary growth deteriorates into deflation, we could see commodity prices fall, especially oil, which would likely push yields lower. Conversely, if the Trump administration pressures the Fed for aggressive easing and increases fiscal spending, bond markets may react negatively, causing yield-curve steepening and market volatility. Both scenarios are plausible in 2025.1

Heading into the coming year, we remain vigilant, understanding that continued volatility could lead to periods of heightened uncertainty, as well as opportunities for well-positioned investment strategies. We acknowledge the higher probability that inflation could persist, but we are prepared to manage these risks through our portfolio construction and broad risk controls.

As inflationary pressures and market volatility are expected to persist into 2025, a dividend-focused approach may prove even more valuable. In our view, dividends offer an essential hedge against inflation and provide a more reliable income stream, marking them as a key component of our strategy in uncertain times.

The Changing Appeal of Dividend Yield

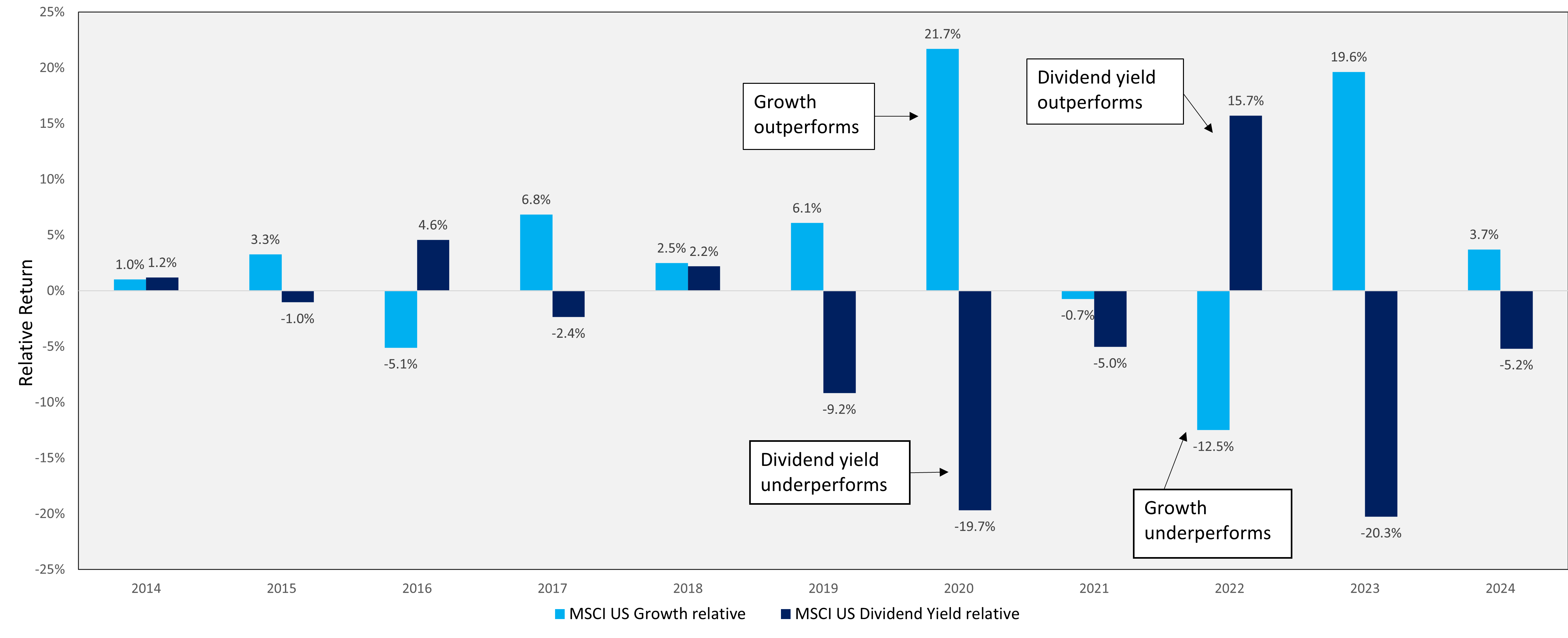

The demand of dividend-paying stocks is influenced by broad market investor sentiment. For much of 2024, dividend-paying stocks underperformed as investors favored high-growth companies. The shift from risk-on to risk-off and back to risk-on exemplifies the market’s current uncertainty.

As demonstrated in the chart below, the preference for dividend yield tends to undergo fluctuations over time. During phases when dividend-paying stocks lose their appeal, often due to a heightened focus on growth stocks, carefully designed risk controls can help investors adeptly navigate the shifting market sentiments, ensuring that portfolios remain resilient and well-positioned for long-term success

Shifting Investor Preference between Growth and Dividend Yield: MSCI Relative Returns

(December 31, 2014 – September 30, 2024)

Source: MSCI, as of September 30, 2024.

Why Dividends Are Set to Shine

The opportunity set within the S&P 500® has grown as more high-growth sectors, particularly information technology, health care and industrials, have seen an increased adoption of dividend payments. As of September 2024, around 80% of S&P 500 companies pay dividends, with 24% of those in the technology sector, up from 13% a decade ago. This shift highlights that growth and income can go hand in hand.2

Dividend-focused investing is particularly compelling in today’s market. Companies that pay and grow dividends tend to be more resilient in downturns as investors seek stability in uncertain times. These companies also have the ability to increase payouts in line with or above inflation, making them an appealing choice for income-focused investors. In a low interest-rate environment, where bond yields are less attractive, dividend paying stocks become even more compelling. With inflation remaining above pre-pandemic levels and potentially moving higher, these stocks are an effective hedge, further enhancing their appeal. Dividends remain a powerful tool for mitigating volatility, providing steady income and serving as a hedge against inflation.

Equities hold a unique advantage in their ability to adjust for inflation, unlike bond yields which remain static. Despite the current dividend yield standing at approximately 2.1%, and bond yields at around 4.2%, the S&P 500 has returned 28.1% year to date (through November 30, 2024), far surpassing the bond yield. This stark difference underscores the potential of equities not only to keep pace with inflation but also to significantly outstrip it, thereby preserving and enhancing the investor’s buying power. In contrast, bond holders may see their purchasing power eroded in an inflationary environment, making dividend-paying equities an even more compelling choice for those seeking both income and growth.

Looking Ahead to 2025

As we look to the year ahead, we continue to see the potential for volatility, with rising inflationary pressures, geopolitical risks and monetary policy as key factors shaping market dynamics. The ever-shifting developments surrounding these factors could drive uncertainty, but they may also create opportunities for investors focused on high-quality companies with reliable dividends. We remain committed to identifying these companies, maintaining a disciplined, dividend-focused approach as we traverse the uncertainty that lies ahead. As the market continues to evolve, we will remain focused on delivering steady income and growth potential, ensuring we are prepared for what the year ahead may bring.

1 Source: BNY Advisors Investment Institute.

2 https://www.ftinstitutionalemea.com/articles/2024/equity/four-reasons-dividends-matter-now

What is in store for investors in 2025? A group of Newton’s research analysts and portfolio managers met to debate and discuss their top ten predictions for 2025 on key positions that oppose prevailing market trends. Could the ‘magnificent seven’ lose their lustre and become the ‘meagre seven’, ushering in a period where small caps rally and outpace large caps? Could the new US administration break inflation, prompting a Federal Reserve (Fed) rate-cutting cycle that moves interest rates to levels last seen during President-elect Trump’s first term?

These ten debates illustrate Newton’s core ability to unlock opportunity by leveraging our multidimensional research capabilities, where all investors and analysts have a seat at the table to engage in spirited debate on their most out-of-consensus viewpoints.

1. The Trump trade head fake: Will interest rates, inflation and the US dollar all lower in 2025?

Point: Growth and inflation are expected to rise in 2025, which should lead to higher rates, a stronger dollar and an increase in equities. The Fed is more cautious regarding inflation risks and global growth is weaker. While these conditions may persist through the first quarter of 2025, it could be a potential contrarian opportunity to buy bonds, sell dollars and favour global ex-US equities. The fiscal impulse may remain flat next year, and tariffs could eventually lower both growth and inflation, thereby posing downside risks to both. Moreover, the US appears very attractive—whether in bonds, equities or currencies—relative to the rest of the world. Additionally, there is an expressed interest among some incoming administration members for a weaker dollar in the future. Efficiencies in reducing the budget deficit through the proposed US Department of Government Efficiency (DOGE) could lower the term premium in bonds. Naturally, there are risks, primarily from the fiscal side, which could impose constraints via bond-market discipline.

Counterpoint: US economic activity remains strong. Consumer spending has recently risen, and corporate activity could also increase as we head into 2025. The recent election of a new pro-business, lighter regulation administration could further heighten inflation. Higher and more enduring inflation may result in structurally higher interest rates relative to recent history but not as restrictive as today.

2. AI winter is coming: Could overcapacity cause an unwind of the consensus AI trade?

Point: Investment in artificial intelligence (AI) is expected to continue growing, and concerns about oversupply may be overstated. The AI theme is still developing and early in its application. Companies are learning about this technology and experimenting with how it can optimise business functions, which could lead to higher future demand as enterprises further leverage AI. Additionally, agents (software applications capable of running tasks independently) and on-device AI might expand the investment opportunities in this space. AI has the potential to affect personal devices, work devices, cars, and homes, leading to a significant hardware upgrade cycle as AI chips are installed on devices for data analysis and decision-making. It is also important to note that AI influences investment beyond the technology sector, affecting areas such as infrastructure, utilities, industrials and nuclear power.

Counterpoint: Generative AI emerged in the technology industry two years ago, leading to a considerable rise in capital expenditure to construct data centres. Given that building data centres takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilise this capacity. While consumers are currently adopting AI technology, enterprises remain in the testing phase. An excess supply could affect tier 2 and tier 3 cloud companies and GPU-as-a-service (high-performance computing) providers that have smaller customer bases and/or are more exposed to AI training relative to inferencing. Companies with robust customer bases, complete AI computing stacks and greater capacity to generate inference revenue may be better positioned for success.

3. America second: Will Europe outperform the US in the coming year?

Point: The United States appears to have surpassed its peak. US equity valuations are exceptionally high, with the disparity between US and UK/Europe valuations reaching unprecedented levels. This gap is primarily driven by a select group of high-performing and influential companies in the US stock market, commonly referred to as the ‘magnificent seven’. It is crucial to consider that any decline in AI demand would adversely affect these companies and consequently affect US valuations overall. In our assessment, European political conditions are anticipated to improve by 2025, which should positively influence European valuations. Furthermore, there is an acceleration in mergers and acquisitions in the UK, contributing to a more optimistic economic outlook. Finally, the US economy may be more vulnerable than generally perceived, with potential inflation on the horizon, thus positioning Europe to potentially outperform the US in the forthcoming years.

Counterpoint: Europe has underperformed for over a decade. While some anticipate a cyclical rebound, this slower growth could be secular. In the US, GDP grew by 2.5% in 2023 and is expected to grow by 2.6% in 2024.1,2 The US also benefits from significant innovation, potentially boosting further GDP growth. Conversely, Europe saw 0.5% GDP growth in 2023 with an expected 1% growth in 2024.3,4 It is also important to recognise that Europe consists of diverse countries, each facing unique challenges. Input costs across Europe are higher than in the US with more expensive electricity costs and a more fixed labour market. Additionally, valuation should be considered, and on a price-to-earnings/return-on-equity basis, the US is far cheaper than Europe.

4. US housing bulls become homeless: Could US housing sink further still?

Point: Existing home sales are at nearly 30-year lows, and there is a strong possibility that they could fall further in 2025.5 Housing affordability remains a real issue and mortgage rates are not declining, which presents a huge roadblock for improving existing home sales in the US.

Counterpoint: While interest rates remain a headwind, the economy and job outlook could become a more important driver for home sales. There is a lot of pent-up demand for housing, and with current rates being similar to rates in the mid-1990s, pent-up demand may be ready to be released. Existing home sales are unsustainably low, and companies participating in fragmented markets exposed to housing may be market winners.

5. The revenge of environmental, social and governance (ESG): Will companies pick up the banner as regulations come under pressure?

Point: Companies should be motivated to enhance value. At the same time, many consumers are concerned with addressing the needs of future generations, necessitating that companies and politicians consider these interests. With this in mind, ESG will remain relevant, but we may observe a balance in language emphasising value creation through ESG practices. For instance, many initiatives aimed at reducing emissions and environmental footprints are financially driven; the expansion of renewable energy has bolstered job creation and decreased foreign dependencies. Furthermore, the rise of AI and proliferation of data centres will require both supplemental power sources such as renewables, and more efficient power sources.On the social front, multiple studies indicate that diversity correlates with higher corporate returns, fosters innovation, enhances employee satisfaction and can reduce corporate costs. ESG is not merely a box-checking exercise; it is fundamentally about generating monetary value.

Counterpoint: ESG, as an acronym, has been politically charged for some time. The US has retreated from the concept while it has remained relevant in many parts of the world. This divergence highlights the varied standards for ESG across the globe. Additionally, regulators may heavily scrutinise any labelled claims of ESG and diversity, equity, and inclusion, which could lead to potential issues such as ‘greenhushing’ (when a company intentionally downplays information about its environmental efforts). The appointment of the next US Securities and Exchange Commission (SEC) chair will be critical, but it is anticipated that the new administration will be less supportive of shareholder proposals and resolutions compared to the current administration. There is also the possibility that the US may withdraw from United Nations climate initiatives, raising questions about whether China might take its place, and what that could mean geopolitically. Lastly, there is a belief that ESG could become a lesser priority as countries turn their focus to other pressing priorities such as security, reliability and affordability.

6. Executive in peace: Could the Trump administration usher in a period of global peace not seen since the Clinton era?

Point: Global peace is a very low probability outcome. Maybe somewhat counterintuitively, countries pursuing more isolationist policies should be a boon for defence spending globally. European countries in NATO have recognised the need to invest in their own defence owing to heightened aggression from Russia. As Trump has made clear, these countries cannot solely depend on the US for blanket defence against Russia, prompting many nations to begin the multi-year process of significantly increasing defence budgets. Additionally, China’s rise has led to heightened defence spending in Asia, which is expected to continue. The Ukraine/Russia conflict has also increased the use of battlefield drones, and there may be significant growth in this market.

Counterpoint: The past sets a precedent, and global peace might prevail once more. We saw how Trump governed from 2017-2020, and he ran his campaign on a very similar strategy this election season. During his first presidential term, the US refrained from entering any new or expanded conflicts. President Trump maintained diplomatic relationships with both North Korean President Kim Jong Un and Russian President Vladimir Putin, and he was committed to the US withdrawal from Afghanistan. Market trends suggest confidence in Trump’s potential to bring about a period of peace, as evidenced by the underperformance of defence stocks following the election. Additionally, Trump has expressed his dedication to mediating an end to the ongoing conflicts in Ukraine and Gaza.

7. David versus Goliath: Will small caps finally find their footing and start a long-term run of beating the ‘magnificent seven’?

Point: Over the last 100 years,US small-cap versus large-cap relative performance is consistently cyclical. We are now in the midst of cycle year 14 of large caps outperforming small caps. Earnings expectations for the Russell 2000 are poised to rise in 2025, and cash flows are improving. It should not take much capital to buoy the index given the low amount of market capitalisation in this arena. Additionally, private equity has been staying private for longer, creating a backlog of companies about to go public and join their small-cap brethren. Current large-cap dominators may be past their prime as these once traditionally capital-light businesses are now capital-intensive, translating to lower multiples.

Counterpoint: The bigger the better. Large-cap companies have outperformed because they have experienced better growth, and small-cap companies will need serious earnings improvement if they are to surpass these giant companies. When looking at the investable universe with an innovation lens, small-cap companies are cheap for a reason. Much of the true market innovation around AI and obesity drugs has been driven by large-cap companies despite the fact that small-cap companies are traditionally the most innovative. Historically, small caps have benefitted from the complacency of large caps, but this is no longer the case. Finally, companies are staying private for longer now, creating an IPO vacuum and minimising the universe of small-cap companies.

8. Make America healthy again: Will health care be the worst sector in 2025?

Point: Between Trump’s nominations for high-level positions, tariffs, further pricing pressure in the sector and subsidy cuts that many believe could come through, it appears every part of health care may be negatively affected. Overwhelming focus has been on the nominations for Trump’s administration, especially the choice of Robert F. Kennedy Jr (RFK) as US health secretary. Given RFK’s past statements, there is a worry that his personal agenda will override evidence-based policy, detracting from health-care and funding priorities. Beyond RFK, it does seem like the upcoming administration is comfortable ratcheting up pricing pressure on drugs, pressuring pharmaceutical companies and all the vendors that support them. Tariffs could also have an impact, to varying degrees, on the medical technology space. Some companies may shift manufacturing or pass this pressure on to consumers. Finally, Republican wins at the federal and state level could influence exchange subsidies and Medicaid rosters as well.

Counterpoint: While there is fear that RFK could upend the health-care system, the health-care sector is at its lowest percentage of the S&P 500® in 20 years while innovation is at an all-time high owing to obesity, immunology, genetic and oncology drug advancements. Kennedy’s rhetoric may be stronger than his eventual policies and, if confirmed, he may have a narrow focus on ingredients in the food supply chain, and the risk/rewards of vaccines. Other appointees for heads of the Food and Drug Administration (FDA), Centers for Disease Control and Prevention (CDC), and the National Institutes of Health (NIH), are all dedicated scientists with no polarising agendas. Overall, there could be some changes ahead surrounding food and some vaccines, but pricing worries and FDA/NIH disruption fears are likely overblown.

9. China in a bull shop: Could China come roaring back and benefit from the Trump administration?

Point: China has significantly reduced its dependency on exporting to the US with its Belt and Road initiative. Exports to the global south now represent roughly half of Chinese exports, while exports to the G7 have nearly halved. There is a misconception that China cannot catch up with Western peers; there are 3.6 million graduates in China each year in STEM subjects (science, technology, engineering and mathematics) versus less than one million in the US.6 These are the skills required for the industries of the future. Additionally, China is increasingly catching up in the semiconductor and AI space, opening many new technology companies. Innovation is especially important, with China filing a significant number of patents compared to the US.

Counterpoint: There are two gravitational forces that may pose concerns for China: a large growth problem and a lack of equity returns. China has trillions of dollars of unsold housing and sells only a fraction of that housing annually. Property still accounts for a high percentage of GDP and home ownership is nearly 100%. This indicates the need for a monumental rebalancing, and a transition from investment-driven growth without affecting other potential growth drivers presents difficulties. Remember, this occurs amid demographic headwinds and high total system leverage. The Chinese Communist Party faces both ideological and practical barriers to aggressive stimulus measures. It appears unlikely to replicate 2008 stimulus levels, and while pension or ‘hukou’ (household registration) reform is possible, it may only stabilise short-term growth. Chinese equities tend to be idiosyncratic and do not provide compound returns owing to significant equity dilution.

10. Tariffs, no biggie: Will a new wave of Trump tariffs be disastrous for the US consumer?

Point: In Trump’s previous presidency, tariffs had little impact on consumers. Tariffs may not always be passed on to the consumer. It is important to consider the competitive dynamics on the industry to which tariffs are being applied. While tariffs could fall heavily on consumers in instances where producers have pricing power, tariffs on undifferentiated products with competitive dynamics could fall heavily on the producer by way of lower margins. It is unlikely that the new administration will implement tariffs in industries where the producers hold pricing power. If aggregate nominal demand grows strongly, corporations could more easily pass on the cost of tariffs to consumers; however, this is not currently the case, and the current economic cycle is mature. Corporations may struggle to pass on tariffs to consumers, with profit pools through the value chain likely taking the bulk of the hit.

Counterpoint: The president-elect has said he believes the current trade system does not benefit American businesses and consumers, so tariffs are a credible threat to both US companies and consumers. Other countries could retaliate, potentially creating a full-blown trade war. Most importantly, tariffs are a headwind for the consumer, the global economy and equities, as they reduce real purchasing power and profit margins. A resulting stronger dollar is also an issue for US profits, and the inflationary effect of higher import prices could lead to a more hawkish Fed given rising inflation expectations. It is expected that these tariffs would be enacted at a time when equity valuations are rich, and do not offer much margin of safety. The transmission mechanism of these costs to the consumer could be through higher borrowing costs, lower asset prices, higher unemployment and higher inflation, lower real wages and a reduction in purchasing power.

Sources:

1 Statista, Annual growth of the real gross domestic product of the United States from 1990 to 2023, January 2024, https://www.statista.com/statistics/188165/annual-gdp-growth-of-the-united-states-since-1990/#:~:text=In%202023%20the%20real%20gross,and%20high%20growth%20in%202021

2 Federal Reserve Bank Philadelphia, Third Quarter 2024 Survey of Professional Forecasters, August 9, 2024, https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/spf-q3-2024#:~:text=Overall%2C%20the%20forecasters%20revised%20upward,compared%20with%20the%20previous%20survey

3 Statista, Gross domestic product (GDP) growth in Central and Eastern European countries compared to the European Union region from 1991 to 2023, November 2024, https://www.statista.com/statistics/1187041/cee-gdp-change/

4 European Commission, Autumn 2024 Economic Forecast: A gradual rebound in an adverse environment, November 2024, https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/economic-forecasts/autumn-2024-economic-forecast-gradual-rebound-adverse-environment_en#:~:text=This%20Autumn%20Forecast%20projects%20real,unchanged%20for%20the%20euro%20area

5 Fannie Mae, Recent Rate Run-Up Expected to Keep Existing Home Sales Near Historic Lows Through 2025, November 2024, https://www.fanniemae.com/newsroom/fannie-mae-news/recent-rate-run-expected-keep-existing-home-sales-near-historic-lows-through-2025#:~:text=WASHINGTON%2C%20DC%20%E2%80%93%20Existing%20home%20sales,Strategic%20Research%20(ESR)%20Group

6 CSET, The Global Distribution of STEM Graduates: Which Countries Lead the Way?, November 2023, https://cset.georgetown.edu/article/the-global-distribution-of-stem-graduates-which-countries-lead-the-way/#:~:text=The%20WEF%20report%20identified%20China,of%20graduates%20in%20STEM%20fields

What is in store for investors in 2025? A group of Newton’s research analysts and portfolio managers met to debate and discuss their top ten predictions for 2025 on key positions that oppose prevailing market trends. Could the ‘magnificent seven’ lose their luster and become the ‘meager seven,’ ushering in a period where small caps rally and outpace large caps? Could the new US administration break inflation, prompting a Federal Reserve (Fed) rate-cutting cycle that moves interest rates to levels last seen during President-elect Trump’s first term?

These ten debates illustrate Newton’s core ability to unlock opportunity by leveraging our multidimensional research capabilities, where all investors and analysts have a seat at the table to engage in spirited debate on their most out-of-consensus viewpoints.

1. The Trump Trade Head Fake: Will interest rates, inflation and the dollar all lower in 2025?

Point: Growth and inflation are expected to rise in 2025, which should lead to higher rates, a stronger dollar and an increase in equities. The Fed is more cautious regarding inflation risks and global growth is weaker. While these conditions may persist through the first quarter of 2025, it could be a potential contrarian opportunity to buy bonds, sell dollars and favor global ex-US equities. The fiscal impulse may remain flat next year, and tariffs could eventually lower both growth and inflation, thereby posing downside risks to both. Moreover, the US appears very attractive—whether in bonds, equities or currencies—relative to the rest of the world. Additionally, there is an expressed interest among some incoming administration members for a weaker dollar in the future. Efficiencies in reducing the budget deficit through the proposed Department of Government Efficiency (DOGE) could lower the term premium in bonds. Naturally, there are risks, primarily from the fiscal side, which could impose constraints via bond-market discipline.

Counterpoint: US economic activity remains strong. Consumer spending has recently risen, and corporate activity could also increase as we head into 2025. The recent election of a new pro-business, lighter regulation administration could further heighten inflation. Higher and more enduring inflation may result in structurally higher interest rates relative to recent history but not as restrictive as today.

2. AI Winter is Coming: Could overcapacity cause an unwind of the consensus AI trade?

Point: Investment in artificial intelligence (AI) is expected to continue growing, and concerns about oversupply may be overstated. The AI theme is still developing and early in its application. Companies are learning about this technology and experimenting with how it can optimize business functions, which could lead to higher future demand as enterprises further leverage AI. Additionally, agents (software applications capable of running tasks independently) and on-device AI might expand the investment opportunities in this space. AI has the potential to affect personal devices, work devices, cars, and homes, leading to a significant hardware upgrade cycle as AI chips are installed on devices for data analysis and decision-making. It is also important to note that AI influences investment beyond the technology sector, affecting areas such as infrastructure, utilities, industrials and nuclear power.

Counterpoint: Generative AI emerged in the technology industry two years ago, leading to a considerable rise in capital expenditure to construct data centers. Given that building data centers takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilize this capacity. While consumers are currently adopting AI technology, enterprises remain in the testing phase. An excess supply could affect tier 2 and tier 3 cloud companies and GPU-as-a-service (high-performance computing) providers that have smaller customer bases and/or are more exposed to AI training relative to inferencing. Companies with robust customer bases, complete AI computing stacks and greater capacity to generate inference revenue may be better positioned for success.

Given that building data centers takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilize this capacity.

3. America Second: Will Europe outperform the US in the coming year?

Point: The United States appears to have surpassed its peak. US equity valuations are exceptionally high, with the disparity between US and UK/Europe valuations reaching unprecedented levels. This gap is primarily driven by a select group of high-performing and influential companies in the US stock market, commonly referred to as the ‘magnificent seven.’ It is crucial to consider that any decline in AI demand would adversely affect these companies and consequently affect US valuations overall. In our assessment, European political conditions are anticipated to improve by 2025, which should positively influence European valuations. Furthermore, there is an acceleration in mergers and acquisitions in the UK, contributing to a more optimistic economic outlook. Finally, the US economy may be more vulnerable than generally perceived, with potential inflation on the horizon, thus positioning Europe to potentially outperform the US in the forthcoming years.

Counterpoint: Europe has underperformed for over a decade. While some anticipate a cyclical rebound, this slower growth could be secular. In the US, GDP grew by 2.5% in 2023 and is expected to grow by 2.6% in 2024.1,2 The US also benefits from significant innovation, potentially boosting further GDP growth. Conversely, Europe saw 0.5% GDP growth in 2023 with an expected 1% growth in 2024.3,4 It is also important to recognize that Europe consists of diverse countries, each facing unique challenges. Input costs across Europe are higher than in the US with more expensive electricity costs and a more fixed labor market. Additionally, valuation should be considered, and on a price-to-earnings/return-on-equity basis, the US is far cheaper than Europe.

4. US Housing Bulls Become Homeless: Could US housing sink further still?

Point: Existing home sales are at nearly 30-year lows, and there is a strong possibility that they could fall further in 2025.5 Housing affordability remains a real issue and mortgage rates are not declining, which presents a huge roadblock for improving existing home sales in the US.

Counterpoint: While interest rates remain a headwind, the economy and job outlook could become a more important driver for home sales. There is a lot of pent-up demand for housing, and with current rates being similar to rates in the mid-1990s, pent-up demand may be ready to be released. Existing home sales are unsustainably low, and companies participating in fragmented markets exposed to housing may be market winners.

5. The Revenge of Environmental, Social and Governance (ESG): Will companies pick up the banner as regulations come under pressure?

Point: Companies should be motivated to enhance value. At the same time, many consumers are concerned with addressing the needs of future generations, necessitating that companies and politicians consider these interests. With this in mind, ESG will remain relevant, but we may observe a balance in language emphasizing value creation through ESG practices. For instance, many initiatives aimed at reducing emissions and environmental footprints are financially driven; the expansion of renewable energy has bolstered job creation and decreased foreign dependencies. Furthermore, the rise of AI and proliferation of data centers will require both supplemental power sources such as renewables, and more efficient power sources. On the social front, multiple studies indicate that diversity correlates with higher corporate returns, fosters innovation, enhances employee satisfaction and can reduce corporate costs. ESG is not merely a box-checking exercise; it is fundamentally about generating monetary value.

Counterpoint: ESG, as an acronym, has been politically charged for some time. The US has retreated from the concept while it has remained relevant in many parts of the world. This divergence highlights the varied standards for ESG across the globe. Additionally, regulators may heavily scrutinize any labelled claims of ESG and diversity, equity, and inclusion, which could lead to potential issues such as ‘greenhushing’ (when a company intentionally downplays information about its environmental efforts). The appointment of the next US Securities and Exchange Commission (SEC) chair will be critical, but it is anticipated that the new administration will be less supportive of shareholder proposals and resolutions compared to the current administration. There is also the possibility that the US may withdraw from United Nations climate initiatives, raising questions about whether China might take its place, and what that could mean geopolitically. Lastly, there is a belief that ESG could become a lesser priority as countries turn their focus to other pressing priorities such as security, reliability and affordability.

6. Executive in Peace: Could the Trump Administration usher in a period of global peace not seen since the Clinton era?

Point: Global peace is a very low probability outcome. Maybe somewhat counterintuitively, countries pursuing more isolationist policies should be a boon for defense spending globally. European countries in NATO have recognized the need to invest in their own defense owing to heightened aggression from Russia. As Trump has made clear, these countries cannot solely depend on the US for blanket defense against Russia, prompting many nations to begin the multi-year process of significantly increasing defense budgets. Additionally, China’s rise has led to heightened defense spending in Asia, which is expected to continue. The Ukraine/Russia conflict has also increased the use of battlefield drones, and there may be significant growth in this market.