What is in store for investors in 2025? A group of Newton’s research analysts and portfolio managers met to debate and discuss their top ten predictions for 2025 on key positions that oppose prevailing market trends. Could the ‘magnificent seven’ lose their lustre and become the ‘meagre seven’, ushering in a period where small caps rally and outpace large caps? Could the new US administration break inflation, prompting a Federal Reserve (Fed) rate-cutting cycle that moves interest rates to levels last seen during President-elect Trump’s first term?

These ten debates illustrate Newton’s core ability to unlock opportunity by leveraging our multidimensional research capabilities, where all investors and analysts have a seat at the table to engage in spirited debate on their most out-of-consensus viewpoints.

1. The Trump trade head fake: Will interest rates, inflation and the US dollar all lower in 2025?

Point: Growth and inflation are expected to rise in 2025, which should lead to higher rates, a stronger dollar and an increase in equities. The Fed is more cautious regarding inflation risks and global growth is weaker. While these conditions may persist through the first quarter of 2025, it could be a potential contrarian opportunity to buy bonds, sell dollars and favour global ex-US equities. The fiscal impulse may remain flat next year, and tariffs could eventually lower both growth and inflation, thereby posing downside risks to both. Moreover, the US appears very attractive—whether in bonds, equities or currencies—relative to the rest of the world. Additionally, there is an expressed interest among some incoming administration members for a weaker dollar in the future. Efficiencies in reducing the budget deficit through the proposed US Department of Government Efficiency (DOGE) could lower the term premium in bonds. Naturally, there are risks, primarily from the fiscal side, which could impose constraints via bond-market discipline.

Counterpoint: US economic activity remains strong. Consumer spending has recently risen, and corporate activity could also increase as we head into 2025. The recent election of a new pro-business, lighter regulation administration could further heighten inflation. Higher and more enduring inflation may result in structurally higher interest rates relative to recent history but not as restrictive as today.

2. AI winter is coming: Could overcapacity cause an unwind of the consensus AI trade?

Point: Investment in artificial intelligence (AI) is expected to continue growing, and concerns about oversupply may be overstated. The AI theme is still developing and early in its application. Companies are learning about this technology and experimenting with how it can optimise business functions, which could lead to higher future demand as enterprises further leverage AI. Additionally, agents (software applications capable of running tasks independently) and on-device AI might expand the investment opportunities in this space. AI has the potential to affect personal devices, work devices, cars, and homes, leading to a significant hardware upgrade cycle as AI chips are installed on devices for data analysis and decision-making. It is also important to note that AI influences investment beyond the technology sector, affecting areas such as infrastructure, utilities, industrials and nuclear power.

Counterpoint: Generative AI emerged in the technology industry two years ago, leading to a considerable rise in capital expenditure to construct data centres. Given that building data centres takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilise this capacity. While consumers are currently adopting AI technology, enterprises remain in the testing phase. An excess supply could affect tier 2 and tier 3 cloud companies and GPU-as-a-service (high-performance computing) providers that have smaller customer bases and/or are more exposed to AI training relative to inferencing. Companies with robust customer bases, complete AI computing stacks and greater capacity to generate inference revenue may be better positioned for success.

3. America second: Will Europe outperform the US in the coming year?

Point: The United States appears to have surpassed its peak. US equity valuations are exceptionally high, with the disparity between US and UK/Europe valuations reaching unprecedented levels. This gap is primarily driven by a select group of high-performing and influential companies in the US stock market, commonly referred to as the ‘magnificent seven’. It is crucial to consider that any decline in AI demand would adversely affect these companies and consequently affect US valuations overall. In our assessment, European political conditions are anticipated to improve by 2025, which should positively influence European valuations. Furthermore, there is an acceleration in mergers and acquisitions in the UK, contributing to a more optimistic economic outlook. Finally, the US economy may be more vulnerable than generally perceived, with potential inflation on the horizon, thus positioning Europe to potentially outperform the US in the forthcoming years.

Counterpoint: Europe has underperformed for over a decade. While some anticipate a cyclical rebound, this slower growth could be secular. In the US, GDP grew by 2.5% in 2023 and is expected to grow by 2.6% in 2024.1,2 The US also benefits from significant innovation, potentially boosting further GDP growth. Conversely, Europe saw 0.5% GDP growth in 2023 with an expected 1% growth in 2024.3,4 It is also important to recognise that Europe consists of diverse countries, each facing unique challenges. Input costs across Europe are higher than in the US with more expensive electricity costs and a more fixed labour market. Additionally, valuation should be considered, and on a price-to-earnings/return-on-equity basis, the US is far cheaper than Europe.

4. US housing bulls become homeless: Could US housing sink further still?

Point: Existing home sales are at nearly 30-year lows, and there is a strong possibility that they could fall further in 2025.5 Housing affordability remains a real issue and mortgage rates are not declining, which presents a huge roadblock for improving existing home sales in the US.

Counterpoint: While interest rates remain a headwind, the economy and job outlook could become a more important driver for home sales. There is a lot of pent-up demand for housing, and with current rates being similar to rates in the mid-1990s, pent-up demand may be ready to be released. Existing home sales are unsustainably low, and companies participating in fragmented markets exposed to housing may be market winners.

5. The revenge of environmental, social and governance (ESG): Will companies pick up the banner as regulations come under pressure?

Point: Companies should be motivated to enhance value. At the same time, many consumers are concerned with addressing the needs of future generations, necessitating that companies and politicians consider these interests. With this in mind, ESG will remain relevant, but we may observe a balance in language emphasising value creation through ESG practices. For instance, many initiatives aimed at reducing emissions and environmental footprints are financially driven; the expansion of renewable energy has bolstered job creation and decreased foreign dependencies. Furthermore, the rise of AI and proliferation of data centres will require both supplemental power sources such as renewables, and more efficient power sources.On the social front, multiple studies indicate that diversity correlates with higher corporate returns, fosters innovation, enhances employee satisfaction and can reduce corporate costs. ESG is not merely a box-checking exercise; it is fundamentally about generating monetary value.

Counterpoint: ESG, as an acronym, has been politically charged for some time. The US has retreated from the concept while it has remained relevant in many parts of the world. This divergence highlights the varied standards for ESG across the globe. Additionally, regulators may heavily scrutinise any labelled claims of ESG and diversity, equity, and inclusion, which could lead to potential issues such as ‘greenhushing’ (when a company intentionally downplays information about its environmental efforts). The appointment of the next US Securities and Exchange Commission (SEC) chair will be critical, but it is anticipated that the new administration will be less supportive of shareholder proposals and resolutions compared to the current administration. There is also the possibility that the US may withdraw from United Nations climate initiatives, raising questions about whether China might take its place, and what that could mean geopolitically. Lastly, there is a belief that ESG could become a lesser priority as countries turn their focus to other pressing priorities such as security, reliability and affordability.

6. Executive in peace: Could the Trump administration usher in a period of global peace not seen since the Clinton era?

Point: Global peace is a very low probability outcome. Maybe somewhat counterintuitively, countries pursuing more isolationist policies should be a boon for defence spending globally. European countries in NATO have recognised the need to invest in their own defence owing to heightened aggression from Russia. As Trump has made clear, these countries cannot solely depend on the US for blanket defence against Russia, prompting many nations to begin the multi-year process of significantly increasing defence budgets. Additionally, China’s rise has led to heightened defence spending in Asia, which is expected to continue. The Ukraine/Russia conflict has also increased the use of battlefield drones, and there may be significant growth in this market.

Counterpoint: The past sets a precedent, and global peace might prevail once more. We saw how Trump governed from 2017-2020, and he ran his campaign on a very similar strategy this election season. During his first presidential term, the US refrained from entering any new or expanded conflicts. President Trump maintained diplomatic relationships with both North Korean President Kim Jong Un and Russian President Vladimir Putin, and he was committed to the US withdrawal from Afghanistan. Market trends suggest confidence in Trump’s potential to bring about a period of peace, as evidenced by the underperformance of defence stocks following the election. Additionally, Trump has expressed his dedication to mediating an end to the ongoing conflicts in Ukraine and Gaza.

7. David versus Goliath: Will small caps finally find their footing and start a long-term run of beating the ‘magnificent seven’?

Point: Over the last 100 years,US small-cap versus large-cap relative performance is consistently cyclical. We are now in the midst of cycle year 14 of large caps outperforming small caps. Earnings expectations for the Russell 2000 are poised to rise in 2025, and cash flows are improving. It should not take much capital to buoy the index given the low amount of market capitalisation in this arena. Additionally, private equity has been staying private for longer, creating a backlog of companies about to go public and join their small-cap brethren. Current large-cap dominators may be past their prime as these once traditionally capital-light businesses are now capital-intensive, translating to lower multiples.

Counterpoint: The bigger the better. Large-cap companies have outperformed because they have experienced better growth, and small-cap companies will need serious earnings improvement if they are to surpass these giant companies. When looking at the investable universe with an innovation lens, small-cap companies are cheap for a reason. Much of the true market innovation around AI and obesity drugs has been driven by large-cap companies despite the fact that small-cap companies are traditionally the most innovative. Historically, small caps have benefitted from the complacency of large caps, but this is no longer the case. Finally, companies are staying private for longer now, creating an IPO vacuum and minimising the universe of small-cap companies.

8. Make America healthy again: Will health care be the worst sector in 2025?

Point: Between Trump’s nominations for high-level positions, tariffs, further pricing pressure in the sector and subsidy cuts that many believe could come through, it appears every part of health care may be negatively affected. Overwhelming focus has been on the nominations for Trump’s administration, especially the choice of Robert F. Kennedy Jr (RFK) as US health secretary. Given RFK’s past statements, there is a worry that his personal agenda will override evidence-based policy, detracting from health-care and funding priorities. Beyond RFK, it does seem like the upcoming administration is comfortable ratcheting up pricing pressure on drugs, pressuring pharmaceutical companies and all the vendors that support them. Tariffs could also have an impact, to varying degrees, on the medical technology space. Some companies may shift manufacturing or pass this pressure on to consumers. Finally, Republican wins at the federal and state level could influence exchange subsidies and Medicaid rosters as well.

Counterpoint: While there is fear that RFK could upend the health-care system, the health-care sector is at its lowest percentage of the S&P 500® in 20 years while innovation is at an all-time high owing to obesity, immunology, genetic and oncology drug advancements. Kennedy’s rhetoric may be stronger than his eventual policies and, if confirmed, he may have a narrow focus on ingredients in the food supply chain, and the risk/rewards of vaccines. Other appointees for heads of the Food and Drug Administration (FDA), Centers for Disease Control and Prevention (CDC), and the National Institutes of Health (NIH), are all dedicated scientists with no polarising agendas. Overall, there could be some changes ahead surrounding food and some vaccines, but pricing worries and FDA/NIH disruption fears are likely overblown.

9. China in a bull shop: Could China come roaring back and benefit from the Trump administration?

Point: China has significantly reduced its dependency on exporting to the US with its Belt and Road initiative. Exports to the global south now represent roughly half of Chinese exports, while exports to the G7 have nearly halved. There is a misconception that China cannot catch up with Western peers; there are 3.6 million graduates in China each year in STEM subjects (science, technology, engineering and mathematics) versus less than one million in the US.6 These are the skills required for the industries of the future. Additionally, China is increasingly catching up in the semiconductor and AI space, opening many new technology companies. Innovation is especially important, with China filing a significant number of patents compared to the US.

Counterpoint: There are two gravitational forces that may pose concerns for China: a large growth problem and a lack of equity returns. China has trillions of dollars of unsold housing and sells only a fraction of that housing annually. Property still accounts for a high percentage of GDP and home ownership is nearly 100%. This indicates the need for a monumental rebalancing, and a transition from investment-driven growth without affecting other potential growth drivers presents difficulties. Remember, this occurs amid demographic headwinds and high total system leverage. The Chinese Communist Party faces both ideological and practical barriers to aggressive stimulus measures. It appears unlikely to replicate 2008 stimulus levels, and while pension or ‘hukou’ (household registration) reform is possible, it may only stabilise short-term growth. Chinese equities tend to be idiosyncratic and do not provide compound returns owing to significant equity dilution.

10. Tariffs, no biggie: Will a new wave of Trump tariffs be disastrous for the US consumer?

Point: In Trump’s previous presidency, tariffs had little impact on consumers. Tariffs may not always be passed on to the consumer. It is important to consider the competitive dynamics on the industry to which tariffs are being applied. While tariffs could fall heavily on consumers in instances where producers have pricing power, tariffs on undifferentiated products with competitive dynamics could fall heavily on the producer by way of lower margins. It is unlikely that the new administration will implement tariffs in industries where the producers hold pricing power. If aggregate nominal demand grows strongly, corporations could more easily pass on the cost of tariffs to consumers; however, this is not currently the case, and the current economic cycle is mature. Corporations may struggle to pass on tariffs to consumers, with profit pools through the value chain likely taking the bulk of the hit.

Counterpoint: The president-elect has said he believes the current trade system does not benefit American businesses and consumers, so tariffs are a credible threat to both US companies and consumers. Other countries could retaliate, potentially creating a full-blown trade war. Most importantly, tariffs are a headwind for the consumer, the global economy and equities, as they reduce real purchasing power and profit margins. A resulting stronger dollar is also an issue for US profits, and the inflationary effect of higher import prices could lead to a more hawkish Fed given rising inflation expectations. It is expected that these tariffs would be enacted at a time when equity valuations are rich, and do not offer much margin of safety. The transmission mechanism of these costs to the consumer could be through higher borrowing costs, lower asset prices, higher unemployment and higher inflation, lower real wages and a reduction in purchasing power.

Sources:

1 Statista, Annual growth of the real gross domestic product of the United States from 1990 to 2023, January 2024, https://www.statista.com/statistics/188165/annual-gdp-growth-of-the-united-states-since-1990/#:~:text=In%202023%20the%20real%20gross,and%20high%20growth%20in%202021

2 Federal Reserve Bank Philadelphia, Third Quarter 2024 Survey of Professional Forecasters, August 9, 2024, https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/spf-q3-2024#:~:text=Overall%2C%20the%20forecasters%20revised%20upward,compared%20with%20the%20previous%20survey

3 Statista, Gross domestic product (GDP) growth in Central and Eastern European countries compared to the European Union region from 1991 to 2023, November 2024, https://www.statista.com/statistics/1187041/cee-gdp-change/

4 European Commission, Autumn 2024 Economic Forecast: A gradual rebound in an adverse environment, November 2024, https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/economic-forecasts/autumn-2024-economic-forecast-gradual-rebound-adverse-environment_en#:~:text=This%20Autumn%20Forecast%20projects%20real,unchanged%20for%20the%20euro%20area

5 Fannie Mae, Recent Rate Run-Up Expected to Keep Existing Home Sales Near Historic Lows Through 2025, November 2024, https://www.fanniemae.com/newsroom/fannie-mae-news/recent-rate-run-expected-keep-existing-home-sales-near-historic-lows-through-2025#:~:text=WASHINGTON%2C%20DC%20%E2%80%93%20Existing%20home%20sales,Strategic%20Research%20(ESR)%20Group

6 CSET, The Global Distribution of STEM Graduates: Which Countries Lead the Way?, November 2023, https://cset.georgetown.edu/article/the-global-distribution-of-stem-graduates-which-countries-lead-the-way/#:~:text=The%20WEF%20report%20identified%20China,of%20graduates%20in%20STEM%20fields

What is in store for investors in 2025? A group of Newton’s research analysts and portfolio managers met to debate and discuss their top ten predictions for 2025 on key positions that oppose prevailing market trends. Could the ‘magnificent seven’ lose their luster and become the ‘meager seven,’ ushering in a period where small caps rally and outpace large caps? Could the new US administration break inflation, prompting a Federal Reserve (Fed) rate-cutting cycle that moves interest rates to levels last seen during President-elect Trump’s first term?

These ten debates illustrate Newton’s core ability to unlock opportunity by leveraging our multidimensional research capabilities, where all investors and analysts have a seat at the table to engage in spirited debate on their most out-of-consensus viewpoints.

1. The Trump Trade Head Fake: Will interest rates, inflation and the dollar all lower in 2025?

Point: Growth and inflation are expected to rise in 2025, which should lead to higher rates, a stronger dollar and an increase in equities. The Fed is more cautious regarding inflation risks and global growth is weaker. While these conditions may persist through the first quarter of 2025, it could be a potential contrarian opportunity to buy bonds, sell dollars and favor global ex-US equities. The fiscal impulse may remain flat next year, and tariffs could eventually lower both growth and inflation, thereby posing downside risks to both. Moreover, the US appears very attractive—whether in bonds, equities or currencies—relative to the rest of the world. Additionally, there is an expressed interest among some incoming administration members for a weaker dollar in the future. Efficiencies in reducing the budget deficit through the proposed Department of Government Efficiency (DOGE) could lower the term premium in bonds. Naturally, there are risks, primarily from the fiscal side, which could impose constraints via bond-market discipline.

Counterpoint: US economic activity remains strong. Consumer spending has recently risen, and corporate activity could also increase as we head into 2025. The recent election of a new pro-business, lighter regulation administration could further heighten inflation. Higher and more enduring inflation may result in structurally higher interest rates relative to recent history but not as restrictive as today.

2. AI Winter is Coming: Could overcapacity cause an unwind of the consensus AI trade?

Point: Investment in artificial intelligence (AI) is expected to continue growing, and concerns about oversupply may be overstated. The AI theme is still developing and early in its application. Companies are learning about this technology and experimenting with how it can optimize business functions, which could lead to higher future demand as enterprises further leverage AI. Additionally, agents (software applications capable of running tasks independently) and on-device AI might expand the investment opportunities in this space. AI has the potential to affect personal devices, work devices, cars, and homes, leading to a significant hardware upgrade cycle as AI chips are installed on devices for data analysis and decision-making. It is also important to note that AI influences investment beyond the technology sector, affecting areas such as infrastructure, utilities, industrials and nuclear power.

Counterpoint: Generative AI emerged in the technology industry two years ago, leading to a considerable rise in capital expenditure to construct data centers. Given that building data centers takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilize this capacity. While consumers are currently adopting AI technology, enterprises remain in the testing phase. An excess supply could affect tier 2 and tier 3 cloud companies and GPU-as-a-service (high-performance computing) providers that have smaller customer bases and/or are more exposed to AI training relative to inferencing. Companies with robust customer bases, complete AI computing stacks and greater capacity to generate inference revenue may be better positioned for success.

Given that building data centers takes approximately three to four years, it is anticipated that significant capacity will become available in 2026-2027. However, there is a question as to whether there will be sufficient demand to utilize this capacity.

3. America Second: Will Europe outperform the US in the coming year?

Point: The United States appears to have surpassed its peak. US equity valuations are exceptionally high, with the disparity between US and UK/Europe valuations reaching unprecedented levels. This gap is primarily driven by a select group of high-performing and influential companies in the US stock market, commonly referred to as the ‘magnificent seven.’ It is crucial to consider that any decline in AI demand would adversely affect these companies and consequently affect US valuations overall. In our assessment, European political conditions are anticipated to improve by 2025, which should positively influence European valuations. Furthermore, there is an acceleration in mergers and acquisitions in the UK, contributing to a more optimistic economic outlook. Finally, the US economy may be more vulnerable than generally perceived, with potential inflation on the horizon, thus positioning Europe to potentially outperform the US in the forthcoming years.

Counterpoint: Europe has underperformed for over a decade. While some anticipate a cyclical rebound, this slower growth could be secular. In the US, GDP grew by 2.5% in 2023 and is expected to grow by 2.6% in 2024.1,2 The US also benefits from significant innovation, potentially boosting further GDP growth. Conversely, Europe saw 0.5% GDP growth in 2023 with an expected 1% growth in 2024.3,4 It is also important to recognize that Europe consists of diverse countries, each facing unique challenges. Input costs across Europe are higher than in the US with more expensive electricity costs and a more fixed labor market. Additionally, valuation should be considered, and on a price-to-earnings/return-on-equity basis, the US is far cheaper than Europe.

4. US Housing Bulls Become Homeless: Could US housing sink further still?

Point: Existing home sales are at nearly 30-year lows, and there is a strong possibility that they could fall further in 2025.5 Housing affordability remains a real issue and mortgage rates are not declining, which presents a huge roadblock for improving existing home sales in the US.

Counterpoint: While interest rates remain a headwind, the economy and job outlook could become a more important driver for home sales. There is a lot of pent-up demand for housing, and with current rates being similar to rates in the mid-1990s, pent-up demand may be ready to be released. Existing home sales are unsustainably low, and companies participating in fragmented markets exposed to housing may be market winners.

5. The Revenge of Environmental, Social and Governance (ESG): Will companies pick up the banner as regulations come under pressure?

Point: Companies should be motivated to enhance value. At the same time, many consumers are concerned with addressing the needs of future generations, necessitating that companies and politicians consider these interests. With this in mind, ESG will remain relevant, but we may observe a balance in language emphasizing value creation through ESG practices. For instance, many initiatives aimed at reducing emissions and environmental footprints are financially driven; the expansion of renewable energy has bolstered job creation and decreased foreign dependencies. Furthermore, the rise of AI and proliferation of data centers will require both supplemental power sources such as renewables, and more efficient power sources. On the social front, multiple studies indicate that diversity correlates with higher corporate returns, fosters innovation, enhances employee satisfaction and can reduce corporate costs. ESG is not merely a box-checking exercise; it is fundamentally about generating monetary value.

Counterpoint: ESG, as an acronym, has been politically charged for some time. The US has retreated from the concept while it has remained relevant in many parts of the world. This divergence highlights the varied standards for ESG across the globe. Additionally, regulators may heavily scrutinize any labelled claims of ESG and diversity, equity, and inclusion, which could lead to potential issues such as ‘greenhushing’ (when a company intentionally downplays information about its environmental efforts). The appointment of the next US Securities and Exchange Commission (SEC) chair will be critical, but it is anticipated that the new administration will be less supportive of shareholder proposals and resolutions compared to the current administration. There is also the possibility that the US may withdraw from United Nations climate initiatives, raising questions about whether China might take its place, and what that could mean geopolitically. Lastly, there is a belief that ESG could become a lesser priority as countries turn their focus to other pressing priorities such as security, reliability and affordability.

6. Executive in Peace: Could the Trump Administration usher in a period of global peace not seen since the Clinton era?

Point: Global peace is a very low probability outcome. Maybe somewhat counterintuitively, countries pursuing more isolationist policies should be a boon for defense spending globally. European countries in NATO have recognized the need to invest in their own defense owing to heightened aggression from Russia. As Trump has made clear, these countries cannot solely depend on the US for blanket defense against Russia, prompting many nations to begin the multi-year process of significantly increasing defense budgets. Additionally, China’s rise has led to heightened defense spending in Asia, which is expected to continue. The Ukraine/Russia conflict has also increased the use of battlefield drones, and there may be significant growth in this market.

Counterpoint: The past sets a precedent, and global peace might prevail once more. We saw how Trump governed from 2017-2020, and he ran his campaign on a very similar strategy this election season. During his first presidential term, the US refrained from entering any new or expanded conflicts. President Trump maintained diplomatic relationships with both North Korean President Kim Jong Un and Russian President Vladimir Putin, and he was committed to the US withdrawal from Afghanistan. Market trends suggest confidence in Trump’s potential to bring about a period of peace, as evidenced by the underperformance of defense stocks following the election. Additionally, Trump has expressed his dedication to mediating an end to the ongoing conflicts in Ukraine and Gaza.

The past sets a precedent, and global peace might prevail once more. We saw how Trump governed from 2017-2020, and he ran his campaign on a very similar strategy this election season.

7. David versus Goliath: Will small caps finally find their footing and start a long-term run of beating the ‘magnificent seven’?

Point: Over the last 100 years, US small-cap versus large-cap relative performance is consistently cyclical. We are now in the midst of cycle year 14 of large caps outperforming small caps. Earnings expectations for the Russell 2000 are poised to rise in 2025, and cash flows are improving. It should not take much capital to buoy the index given the low amount of market capitalization in this arena. Additionally, private equity has been staying private for longer, creating a backlog of companies about to go public and join their small-cap brethren. Current large-cap dominators may be past their prime as these once traditionally capital-light businesses are now capital-intensive, translating to lower multiples.

Counterpoint: The bigger the better. Large-cap companies have outperformed because they have experienced better growth, and small-cap companies will need serious earnings improvement if they are to surpass these giant companies. When looking at the investable universe with an innovation lens, small-cap companies are cheap for a reason. Much of the true market innovation around AI and obesity drugs has been driven by large-cap companies despite the fact that small-cap companies are traditionally the most innovative. Historically, small caps have benefitted from the complacency of large caps, but this is no longer the case. Finally, companies are staying private for longer now, creating an IPO vacuum and minimizing the universe of small-cap companies.

8. Make America Healthy Again: Will health care be the worst sector in 2025?

Point: Between Trump’s nominations for high-level positions, tariffs, further pricing pressure in the sector and subsidy cuts that many believe could come through, it appears every part of health care may be negatively affected. Overwhelming focus has been on the nominations for Trump’s administration, especially the choice of Robert F. Kennedy Jr (RFK) as health secretary. Given RFK’s past statements, there is a worry that his personal agenda will override evidence-based policy, detracting from health-care and funding priorities. Beyond RFK, it does seem like the upcoming administration is comfortable ratcheting up pricing pressure on drugs, pressuring pharmaceutical companies and all the vendors that support them. Tariffs could also have an impact, to varying degrees, on the medical technology space. Some companies may shift manufacturing or pass this pressure on to consumers. Finally, Republican wins at the federal and state level could influence exchange subsidies and Medicaid rosters as well.

Counterpoint: While there is fear that RFK could upend the health-care system, the health-care sector is at its lowest percentage of the S&P 500® in 20 years while innovation is at an all-time high owing to obesity, immunology, genetic and oncology drug advancements. Kennedy’s rhetoric may be stronger than his eventual policies and, if confirmed, he may have a narrow focus on ingredients in the food supply chain, and the risk/rewards of vaccines. Other appointees for heads of the Food and Drug Administration (FDA), Centers for Disease Control and Prevention (CDC), and the National Institutes of Health (NIH), are all dedicated scientists with no polarizing agendas. Overall, there could be some changes ahead surrounding food and some vaccines, but pricing worries and FDA/NIH disruption fears are likely overblown.

9. China in a Bull Shop: Could China come roaring back and benefit from the Trump administration?

Point: China has significantly reduced its dependency on exporting to the US with the Belt and Road initiative. Exports to the global south now represent roughly half of Chinese exports, while exports to the G7 have nearly halved. There is a misconception that China cannot catch up with Western peers; there are 3.6 million graduates in China each year in STEM subjects (Science, Technology, Engineering and Mathematics) versus less than one million in the US.6 These are the skills required for the industries of the future. Additionally, China is increasingly catching up in the semiconductor and AI space, opening many new technology companies. Innovation is especially important, with China filing a significant number of patents compared to the US.

Counterpoint: There are two gravitational forces that may pose concerns for China: a large growth problem and a lack of equity returns. China has trillions of dollars of unsold housing and sells only a fraction of that housing annually. Property still accounts for a high percentage of GDP and home ownership is nearly 100%. This indicates the need for a monumental rebalancing, and a transition from investment-driven growth without affecting other potential growth drivers presents difficulties. Remember, this occurs amid demographic headwinds and high total system leverage. The Chinese Communist Party faces both ideological and practical barriers to aggressive stimulus measures. It appears unlikely to replicate 2008 stimulus levels, and while pension or ‘hukou’ (household registration) reform is possible, it may only stabilize short-term growth. Chinese equities tend to be idiosyncratic and do not provide compound returns owing to significant equity dilution.

There are two gravitational forces that may pose concerns for China: a large growth problem and a lack of equity returns.

10. Tariffs, No Biggie: Will a new wave of Trump tariffs be disastrous for the US consumer?

Point: In Trump’s previous presidency, tariffs had little impact on consumers. Tariffs may not always be passed on to the consumer. It is important to consider the competitive dynamics on the industry to which tariffs are being applied. While tariffs could fall heavily on consumers in instances where producers have pricing power, tariffs on undifferentiated products with competitive dynamics could fall heavily on the producer by way of lower margins. It is unlikely that the new administration will implement tariffs in industries where the producers hold pricing power. If aggregate nominal demand grows strongly, corporations could more easily pass on the cost of tariffs to consumers; however, this is not currently the case, and the current economic cycle is mature. Corporations may struggle to pass on tariffs to consumers, with profit pools through the value chain likely taking the bulk of the hit.

Counterpoint: The president elect has said he believes the current trade system does not benefit American businesses and consumers, so tariffs are a credible threat to both US companies and consumers. Other countries could retaliate, potentially creating a full-blown trade war. Most importantly, tariffs are a headwind for the consumer, the global economy and equities, as they reduce real purchasing power and profit margins. A resulting stronger dollar is also an issue for US profits, and the inflationary effect of higher import prices could lead to a more hawkish Fed given rising inflation expectations. It is expected that these tariffs would be enacted at a time when equity valuations are rich, and do not offer much margin of safety. The transmission mechanism of these costs to the consumer could be through higher borrowing costs, lower asset prices, higher unemployment and higher inflation, lower real wages and a reduction in purchasing power.

Sources:

1 Statista, Annual growth of the real gross domestic product of the United States from 1990 to 2023, January 2024, https://www.statista.com/statistics/188165/annual-gdp-growth-of-the-united-states-since-1990/#:~:text=In%202023%20the%20real%20gross,and%20high%20growth%20in%202021

2 Federal Reserve Bank Philadelphia, Third Quarter 2024 Survey of Professional Forecasters, August 9, 2024, https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/spf-q3-2024#:~:text=Overall%2C%20the%20forecasters%20revised%20upward,compared%20with%20the%20previous%20survey

3 Statista, Gross domestic product (GDP) growth in Central and Eastern European countries compared to the European Union region from 1991 to 2023, November 2024, https://www.statista.com/statistics/1187041/cee-gdp-change/

4 European Commission, Autumn 2024 Economic Forecast: A gradual rebound in an adverse environment, November 2024, https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/economic-forecasts/autumn-2024-economic-forecast-gradual-rebound-adverse-environment_en#:~:text=This%20Autumn%20Forecast%20projects%20real,unchanged%20for%20the%20euro%20area

5 Fannie Mae, Recent Rate Run-Up Expected to Keep Existing Home Sales Near Historic Lows Through 2025, November 2024, https://www.fanniemae.com/newsroom/fannie-mae-news/recent-rate-run-expected-keep-existing-home-sales-near-historic-lows-through-2025#:~:text=WASHINGTON%2C%20DC%20%E2%80%93%20Existing%20home%20sales,Strategic%20Research%20(ESR)%20Group

6 CSET, The Global Distribution of STEM Graduates: Which Countries Lead the Way?, November 2023, https://cset.georgetown.edu/article/the-global-distribution-of-stem-graduates-which-countries-lead-the-way/#:~:text=The%20WEF%20report%20identified%20China,of%20graduates%20in%20STEM%20fields

What is your outlook for the UK economy?

Things are getting better. There has been a reduction in income tax and national insurance as a percentage of earnings, and average earnings growth is above inflation. In addition, household cash flow is expected to increase by around 10% this year1 and the next inflation print should be just over 2%. The Bank of England raised its forecast for UK economic growth, and in both continental Europe and the UK interest-rate cuts are set to come soon. Finally, investment spend is also on the rise.

How is UK merger and acquisition activity looking?

Bids for UK-listed companies in the year to date (28 May 2024) were US$77bn whereas last year the total bid count was just US$25bn,2 with interest mostly from overseas buyers. Normally if you have an undervalued market relative to overseas you are going to start to see more bid activity either from private equity or overseas players. We have started to see that.

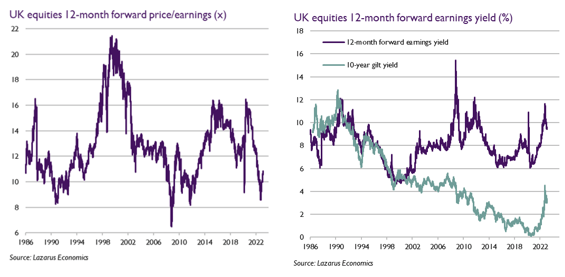

Is the UK still cheap relative to other equity markets?

The UK is still cheap. At around 11x earnings on a 12-month forward price-to-earnings (P/E) basis, the UK is at the lower end of its range over the last 20 years.3 This is in stark contrast to the US which is on 21x earnings on a P/E basis.4 In the US, ‘big tech’ is trading well above its long run average. Heavy flows into the US equity market have been driven by artificial intelligence (AI) optimism, but in many cases that enthusiasm looks to be priced in.

The result of all this is that tech valuations in terms of P/E are off the scale relative to history. AI is probably a positive, but will it monetise in the way it has been assumed in valuations? I would say not. You have an expensive US market, expensive tech, momentum-driven retail flows, and a lot of tech company directors selling shares.5 When viewed together these are cautionary signals.

Who owns UK equities now?

UK equities are under-owned by domestic asset owners. UK pension funds have an average allocation to domestic equities of just 2.8% – a sharp contrast with Japan where the figure is 49.8%, and with the US where it is 63.5%.6 This is despite the UK and Japan occupying similar weights in the MSCI World index, of 4.5% and 4.4%, respectively. There is a government-led effort underway to get more people to buy UK equities7 and pension funds are under pressure to increase allocations.8 The fact that more UK stocks are held by overseas rather than domestic investors is unusual, and highlights we are at rock bottom when it comes to exposure in the UK. Hopefully, this will be a trigger for things to improve.

Who are the potential new buyers of UK equities other than the companies themselves?

The fact that Europe and the UK are expected to cut interest rates before the US means there will potentially be more interest from the US in buying UK equities. We think that trend will continue for both the UK and Europe. We also think the marginal buyer from overseas is becoming more positive. Foreign investors took a step back because of Brexit and the situation in Ukraine, but, despite the upcoming general election, we do not think political risk in the UK is particularly high because the main parties are relatively similar from a stock market perspective.

In terms of UK domestic buyers, they are coming from such a low base. They could be encouraged as they see their own market rise and be tempted to reverse their underweight positions. As mentioned, the government is pushing harder to stimulate domestic investment through the likes of British ISAs (individual savings accounts) and solvency rules, so that could offer some support. Meanwhile, the growth of defined contribution (DC) pensions could also boost equities overall over time.

The Newton UK Income strategy can invest a certain amount in overseas equities. Can you explain the rationale for this and why it is important?

The team has the potential to invest up to 20% of the portfolio overseas. We think this gives us access to the best global options and thematic and sector ideas that cannot be accessed in the UK. A current sector example is chemicals in Europe. With input from our team of global analysts and global income portfolio managers, looking overseas allows us to access best-in-class stocks while still hitting our yield objectives.

That said, do you look at opportunities within the FTSE 250?

We do look at this area and do own some FTSE 250 stocks. However, liquidity in the FTSE 250 market is not as good as it was. Having the opportunity to invest outside the UK enables us to find attractive overseas stocks that are more liquid. That means we do not have to dip too far down the market cap spectrum.

What is your outlook for UK dividends?

We expect UK dividends to grow and rise more than inflation over the next few years, led by financials and energy stocks. UK equities offer attractive high yields that we believe are durable and will grow from here.

Where are you finding sources of income in the UK market?

We are looking to buy companies that are growing and that we think can outperform in an economic recovery. We have no exposure to utilities and we are underweight consumer staples as we think these still have defensive bond proxy characteristics which are unattractive in the current environment. We see more growth potential from financials like banks, as well as industrial stocks and oil where we see good distribution yields and expect to see both dividend and earnings growth.

Most income is coming from financials, industrials, materials, consumer discretionary and energy. These sectors are sensitive to economic growth, and I think earnings prospects are likely to improve rather than go in the other direction. Overall, we are positioning the portfolio to seek to outperform a rising market, and are aiming to benefit from what we think will be a recovery and economic growth as interest rates come down.

Do you see the recent upturn of bank stocks continuing? Could falling interest rates affect this?

The short answer is yes. Banks are cheap. Interest rates are likely to fall but bond yields should have already priced that in. It has been beneficial for banks to come out of the quantitative easing and zero-interest rate policy environment since the global financial crisis. I think bank returns on equity are durable, and if we get some economic growth coming through that could help loan growth. Furthermore, they have built up capital and are paying out high dividends with further buybacks to come. Overall, we think the bank rally has further to go. The key risk is an economic slowdown or recession. We do not see that happening in the short to medium term.

Sources

1. Lazarus Economics, ONS, March 2024.

2. Deutsche Numis, May 2024

3. Factset, Goldman Sachs Global Investment Research, March 2024.

4. Ibid.

5. Business Insider. Nvidia’s directors bagged $80 million last week in a selling spree following the company’s blowout results. 29 February 2024; Bloomberg UK. Zuckerberg sold nearly half a billion dollars of Meta stock in last two months. 3 January 2024; QZ.com. Jeff Bezos has now sold billions worth of Amazon stock – and saved millions by moving to Florida. Updated 21 February 2024.

6. Capital Markets Industry Taskforce, 31 December 2023.

7. FT. ‘British Isa’ aims to boost ailing equities. 6 March 2024.

8. Gov.uk. Chancellor backs British business with pension fund reforms. 2 March 2024.

What is your outlook for the UK economy?

Things are getting better. There has been a reduction in income tax and national insurance as a percentage of earnings, and average earnings growth is above inflation. In addition, household cash flow is expected to increase by around 10% this year1 and the next inflation print should be just over 2%. The Bank of England raised its forecast for UK economic growth, and in both continental Europe and the UK interest-rate cuts are set to come soon. Finally, investment spend is also on the rise.

How is UK merger and acquisition activity looking?

Bids for UK-listed companies in the year to date (28 May 2024) were US$77bn whereas last year the total bid count was just US$25bn,2 with interest mostly from overseas buyers. Normally if you have an undervalued market relative to overseas you are going to start to see more bid activity either from private equity or overseas players. We have started to see that.

Is the UK still cheap relative to other equity markets?

The UK is still cheap. At around 11x earnings on a 12-month forward price-to-earnings (P/E) basis, the UK is at the lower end of its range over the last 20 years.3 This is in stark contrast to the US which is on 21x earnings on a P/E basis.4 In the US, ‘big tech’ is trading well above its long run average. Heavy flows into the US equity market have been driven by artificial intelligence (AI) optimism, but in many cases that enthusiasm looks to be priced in.

The result of all this is that tech valuations in terms of P/E are off the scale relative to history. AI is probably a positive, but will it monetise in the way it has been assumed in valuations? I would say not. You have an expensive US market, expensive tech, momentum-driven retail flows, and a lot of tech company directors selling shares.5 When viewed together these are cautionary signals.

Who owns UK equities now?

UK equities are under-owned by domestic asset owners. UK pension funds have an average allocation to domestic equities of just 2.8% – a sharp contrast with Japan where the figure is 49.8%, and with the US where it is 63.5%.6 This is despite the UK and Japan occupying similar weights in the MSCI World index, of 4.5% and 4.4%, respectively. There is a government-led effort underway to get more people to buy UK equities7 and pension funds are under pressure to increase allocations.8 The fact that more UK stocks are held by overseas rather than domestic investors is unusual, and highlights we are at rock bottom when it comes to exposure in the UK. Hopefully, this will be a trigger for things to improve.

Who are the potential new buyers of UK equities other than the companies themselves?

The fact that Europe and the UK are expected to cut interest rates before the US means there will potentially be more interest from the US in buying UK equities. We think that trend will continue for both the UK and Europe. We also think the marginal buyer from overseas is becoming more positive. Foreign investors took a step back because of Brexit and the situation in Ukraine, but, despite the upcoming general election, we do not think political risk in the UK is particularly high because the main parties are relatively similar from a stock market perspective.

In terms of UK domestic buyers, they are coming from such a low base. They could be encouraged as they see their own market rise and be tempted to reverse their underweight positions. As mentioned, the government is pushing harder to stimulate domestic investment through the likes of British ISAs (individual savings accounts) and solvency rules, so that could offer some support. Meanwhile, the growth of defined contribution (DC) pensions could also boost equities overall over time.

UK equity strategies sometimes invest a certain amount in overseas equities. Can you explain the rationale for this and why it is important?

We think this can provide access to the best global options and thematic and sector ideas that cannot be accessed in the UK. A current sector example is chemicals in Europe. With input from our team of global analysts and global income portfolio managers, looking overseas allows us to access best-in-class stocks while still focusing on our yield objectives.

That said, do you look at opportunities within the FTSE 250?

We do look at this area and do own some FTSE 250 stocks. However, liquidity in the FTSE 250 market is not as good as it was. Having the opportunity to invest outside the UK enables us to find attractive overseas stocks that are more liquid. That means we do not have to dip too far down the market cap spectrum.

What is your outlook for UK dividends?

We expect UK dividends to grow and rise more than inflation over the next few years, led by financials and energy stocks. UK equities offer attractive high yields that we believe are durable and will grow from here.

Where are you finding sources of income in the UK market?

We are looking to buy companies that are growing and that we think can outperform in an economic recovery. We have no exposure to utilities and we are underweight consumer staples as we think these still have defensive bond proxy characteristics which are unattractive in the current environment. We see more growth potential from financials like banks, as well as industrial stocks and oil where we see good distribution yields and expect to see both dividend and earnings growth.

Most income is coming from financials, industrials, materials, consumer discretionary and energy. These sectors are sensitive to economic growth, and I think earnings prospects are likely to improve rather than go in the other direction. Overall, we are positioning the portfolio to seek to outperform a rising market, and are aiming to benefit from what we think will be a recovery and economic growth as interest rates come down.

Do you see the recent upturn of bank stocks continuing? Could falling interest rates affect this?

The short answer is yes. Interest rates are likely to fall but bond yields should have already priced that in. It has been beneficial for banks to come out of the quantitative easing and zero-interest rate policy environment since the global financial crisis. I think bank returns on equity are durable, and if we get some economic growth coming through that could help loan growth. Furthermore, they have built up capital and are paying out high dividends with further buybacks to come. Overall, we think the bank rally has further to go. The key risk is an economic slowdown or recession. We do not see that happening in the short to medium term.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Sources:

- Lazarus Economics, ONS, March 2024.

- Deutsche Numis, May 2024

- Factset, Goldman Sachs Global Investment Research, March 2024.

- Ibid.

- Business Insider. Nvidia’s directors bagged $80 million last week in a selling spree following the company’s blowout results. 29 February 2024; Bloomberg UK. Zuckerberg sold nearly half a billion dollars of Meta stock in last two months. 3 January 2024; QZ.com. Jeff Bezos has now sold billions worth of Amazon stock – and saved millions by moving to Florida. Updated 21 February 2024.

- Capital Markets Industry Taskforce, 31 December 2023.

- FT. ‘British Isa’ aims to boost ailing equities. 6 March 2024.

- Gov.uk. Chancellor backs British business with pension fund reforms. 2 March 2024.

Key points

- It looks more likely now that US interest rates have peaked.

- We expect UK interest rates to follow suit and for inexpensive, economically sensitive companies to continue to benefit.

Predicting the precise time when sentiment turns is fraught with difficulty, but there is a good chance that this happened with the release of October’s US inflation data. After many months of rising bond yields and falling stock valuations, US consumer-price data came in marginally lower than expected; the S&P 500 Index rallied 2%, and US Treasury yields dropped sharply.1 The gains in the UK’s FTSE 100 Index were lighter but the composition was more interesting. Shares likely to benefit from falling rates and improved economic activity were shaken from the slumber of the last couple of years. These included property companies, housebuilders, industrials and financials. UK consumer-price inflation data continued the trend, dropping from 6.7% in September to 4.6% in October,2 again undershooting economists’ expectations.

The change in mood was certainly welcome to us as managers of a UK equity income strategy. For several months we have been using our clients’ money to buy these attractively valued shares, waiting for the moment when others might also spot these potentially profitable opportunities and join us.

The gloom of the last two years has been broadcast at high volume. War, higher inflation leading to higher rates, falling asset prices and the constant threat of a recession which has never quite arrived have been the constant story for the last few years. However, all difficult times end eventually and when they do, investors look forward and risk appetites increase. The point of change can be when some of the most outsized gains in the stock market can be made. Conversely, these are vicious rotations for those with entrenched bearish positioning.

To understand why inflation is dropping, it is worth considering its origin. For this, I offer you my apologies in advance as I ask you to return in your mind to the time of the pandemic, since it is here where the origins of this inflation began.

Two distinct economic events occurred during the pandemic, and they both caused inflation: there was the impact of new money created through government largesse, and the impact on the availability of goods owing to disruption to supply chains. The effects of both may be receding, but while the first may take some years to work off, the second is rather more likely to be transient. The receding effects of both are likely to mean that interest rates have peaked, and a global recession may be avoided.

First, let’s consider the impact of new money. Governments across the developed world handed over money to anyone who seemed worthy, with few strings attached. In the UK, we had the furlough scheme and small business loans, most of which will never be repaid, and a large proportion of which were acquired fraudulently. In the US, money was deposited directly into the accounts of every US citizen; even US citizens living in the UK received a gift from President Donald Trump to add to their furlough money. Deposits sat dormant in bank accounts during lockdowns as there were few things interesting to spend upon. However, as soon as lockdown finished, inflation jumped. Lots of new money but no new goods and services is a recipe for rising prices. Only when all the new deposits created have stopped chasing the limited supply of goods and services should inflation caused through this effect cease.

Secondly, the pandemic caused disruption to supply chains which was also inflationary. Fewer people were able to work in factories and offices, ports were understaffed, and travel of goods and people were restricted. In an intensely specialised world, with parts for finished goods coming from many different countries, it would only take one or two bottlenecks to cause chaos, which duly ensued. The natural response to worries around supply was hoarding. While consumers hoarded toilet rolls, industrial companies did the same with everything they thought might conceivably be useful: oil, paper, building materials, chemicals and semiconductors. The consequence was shortages of just about everything and a resulting spike in prices.

Now for the good news: supply chains are rapidly normalising. A range of early cyclical companies have experienced unprecedented reductions in demand – chemicals companies and semiconductors have never had such a dearth in new orders. We differ from mainstream thought sharply here. This is not a sign of recession, but rather a normalisation process as customers work off their pandemic inventories. We believe the removal of cost and excess stock from supply chains should turn out to be very deflationary, and economically stimulative.

Deposits in the banking system still remain as the result of government excesses, which may mean that rates do not return to their pre-pandemic lows. However, it looks more likely now that US interest rates have peaked. The bond market agrees with us, with US 10-year yields dropping sharply following the release of the US inflation data. We would expect UK rates to follow, and for inexpensive, economically sensitive companies held in our UK Equity Income strategy to continue to benefit.

Sources:

- Financial Times as at 14/11/2023

- Office of National Statistics, CPI.

We discuss the outlook for UK equities.

Key points

- We believe UK equities still have a lot to offer.

- Even weighed against a gloomy economic outlook, we find a 10% 12-month forward earnings yield compelling.

While some turbulence has recently returned to equity markets as a result of turmoil in the banking sector, UK stocks had started 2023 on a strong footing, with the FTSE All-Share Index reaching new all-time highs. This was despite an uncertain outlook with sticky inflation, negative GDP (gross domestic product) revisions, and companies guiding with caution. Against this backdrop, we remain optimistic for UK equities, and here we explain why.

The UK market has long traded at a discount to its global peers and, in fact, has underperformed the S&P 500 index by a staggering 60% and 230% on a five and 10-year basis respectively.1 While some of this underperformance may be explained by the slightly lower relative earnings profile of the UK market as well as the numerous political distractions (such as Brexit and last year’s mini-budget calamity), this does not fully explain the extent of the UK market’s underperformance over this period. At the time of writing, the FTSE All-Share Index trades at a near all-time low 10x price-to-earnings multiple.2 Even weighed against a gloomy economic outlook, we find a 10%3 12-month forward earnings yield compelling and, in our opinion, leaves scope for the FTSE All-Share to continue its advance.

Many UK companies generate a high proportion of their sales overseas

It is often said that the UK GDP outlook is one of the gloomiest in the developed world, but UK-listed companies can often grow independently of UK GDP. In fact, the majority of FTSE 100 and FTSE 250 company sales (c.82% and c.57% respectively) come from outside the UK,4 and we find the growth profiles of many companies are more dialled into structural drivers which are far longer-term in nature and so should be more resilient through the cycle. This includes exposure to the vibrant health-care sector, the ever-evolving shift to digitalisation and, increasingly, the demand to find more energy and environmentally efficient solutions.

Attractive UK dividend yield

The UK is often compared to the US, and it is the case that the sales-growth profile of UK companies can look lacklustre in comparison, particularly given the significant difference in technology stock exposure. However, generally UK companies tend to prioritise healthy margins over unprofitable sales growth which, as we come out of an extended period of ‘free money’, we believe could be seen more favourably. Companies which are well invested, with minimal capital intensity and the ability to generate sustainably high returns and cash flow should attract investors. Companies of this type are typically able to pay out a greater quantum of excess cash to shareholders while still maintaining healthy balance sheets, something which is reflected in the more attractive UK dividend yield.

As active managers with a bottom-up stock-picking approach, we can select companies with the most attractive growth prospects, highest quality attributes and most compelling valuations. The high weighting of more ‘conventional’ and cyclical businesses such as banks and commodities often distorts the perception of quality within the UK, but our ability to invest differently from the benchmark means we select those companies that we believe have the best chance of generating strong returns in future.

It is this combination of sustainable earnings growth, with limited correlation to GDP, discounted valuations relative to global peers and a higher focus on earnings and cash flow that gives us a positive outlook for UK equities and makes us believe the asset class still has a lot to offer.

Sources:

- Bloomberg, 20/2/2013 –17/02/2023, 20/02/2018 – 17/2/2023

- Lazarus Economics

- Lazarus Economics

- FTSE Russell https://www.ftserussell.com/blogs/overseas-revenues-boon-ftse-100-performance

Looking back on a year of multiple crises.

“The basic rule of a crisis is that you don’t come out of it the same. If you get through it, you come out better or worse, but not the same.” This observation by Pope Francis has interesting implications for all of us but particularly for UK equity investors as 2022 has been the year of crises.

European war, energy-price spikes, inflation, rising interest rates, sterling weakness, looming recession and political disarray, as well as the longer-duration issue of climate change, have featured throughout 2022. Crises bring about change, and in 2022 the domino effects of these crises have been far-reaching. They have not only affected investment strategies and returns but have also challenged the investment philosophies themselves: active versus passive, conventional versus sustainable, growth versus value.

The most notable event in 2022 was unquestionably Russia’s invasion of Ukraine. The disruption of energy and food supplies, and the implications for energy prices and for defence spending created a negative impact wave leading to higher inflation, higher interest rates, lower economic growth and, consequently, lower equity prices. Sustainability was put on the back foot, with a general backing off of hawkishness on carbon emissions in favour of energy security, and a more positive assessment of the moral dilemmas around investing in defence.

In a potentially linked outcome, COP27 made no real progress on reducing carbon emissions. The war in Ukraine also put pressure on governments as they sought to mitigate the impact on their constituents. The UK did not fare well in this regard. 2022 has been the year of three prime ministers. Governance issues eliminated the first, economic incompetence the second, while the third, post the brief panic on bond yields and mortgage rates, has returned to defensive fiscal orthodoxy.

From a UK equity perspective, the investment impact of all this change has been substantial. Stocks negatively sensitive to higher interest rates, notably growth stocks, underperformed. The weak performance of the domestic economy alongside weak sterling hit the FTSE 250, while the FTSE 100 offered more resilience given its global tilt and its exposure to ‘invasion winners’ such as oils and mining, as well as financials which benefited from higher rates. In terms of investment styles, value (often ‘old economy’ – defence, tobacco, oil) outperformed growth, while conventional outperformed sustainable for similar reasons. Passive generally outperformed active, even though one could have assumed passive funds, which are commonly algorithms of the past, may have struggled with the extent of disruption. However, UK active investment managers’ continued bias towards growth and mid-cap stocks has largely proved costly.

In conclusion, it is worth noting that, despite everything, the FTSE 100 has remained almost flat in 2022. This is perhaps because the starting point, post Brexit and the pandemic, was already depressed. As we look towards 2023, the low equity valuations reflected in the index continue to suggest a gloomy outlook. However, outcomes are difficult to predict as the key crises of Ukraine and the threat of recession can still play out in different ways.

Meanwhile, reassessment of portfolio styles is likely to continue as negative investment performance challenges established trends towards growth and sustainability investing. Crises do tend to generate change and, consequently, change the perceptions of investors, although as active managers will attest, judging that change is not always easy. The burden of potential for investors to capitalise on this change remains as they seek to deliver positive returns versus the passive competition. Most will be hoping that 2023 is a less interesting year.

THIS ARTICLE FIRST APPEARED IN FT ADVISER

Looking back on a year of multiple crises.

“The basic rule of a crisis is that you don’t come out of it the same. If you get through it, you come out better or worse, but not the same.” This observation by Pope Francis has interesting implications for all of us but particularly for UK equity investors as 2022 has been the year of crises.

European war, energy-price spikes, inflation, rising interest rates, sterling weakness, looming recession and political disarray, as well as the longer-duration issue of climate change, have featured throughout 2022. Crises bring about change, and in 2022 the domino effects of these crises have been far-reaching. They have not only affected investment strategies and returns but have also challenged the investment philosophies themselves: active versus passive, conventional versus sustainable, growth versus value.

The most notable event in 2022 was unquestionably Russia’s invasion of Ukraine. The disruption of energy and food supplies, and the implications for energy prices and for defense spending created a negative impact wave leading to higher inflation, higher interest rates, lower economic growth and, consequently, lower equity prices. Sustainability was put on the back foot, with a general backing off of hawkishness on carbon emissions in favor of energy security, and a more positive assessment of the moral dilemmas around investing in defense.

In a potentially linked outcome, COP27 made no real progress on reducing carbon emissions. The war in Ukraine also put pressure on governments as they sought to mitigate the impact on their constituents. The UK did not fare well in this regard. 2022 has been the year of three prime ministers. Governance issues eliminated the first, economic incompetence the second, while the third, post the brief panic on bond yields and mortgage rates, has returned to defensive fiscal orthodoxy.

From a UK equity perspective, the investment impact of all this change has been substantial. Stocks negatively sensitive to higher interest rates, notably growth stocks, underperformed. The weak performance of the domestic economy alongside weak sterling hit the FTSE 250, while the FTSE 100 offered more resilience given its global tilt and its exposure to ‘invasion winners’ such as oils and mining, as well as financials which benefited from higher rates. In terms of investment styles, value (often ‘old economy’ – defense, tobacco, oil) outperformed growth, while conventional outperformed sustainable for similar reasons. Passive generally outperformed active, even though one could have assumed passive funds, which are commonly algorithms of the past, may have struggled with the extent of disruption. However, UK active investment managers’ continued bias towards growth and mid-cap stocks has largely proved costly.

In conclusion, it is worth noting that, despite everything, the FTSE 100 has remained almost flat in 2022. This is perhaps because the starting point, post Brexit and the pandemic, was already depressed. As we look towards 2023, the low equity valuations reflected in the index continue to suggest a gloomy outlook. However, outcomes are difficult to predict as the key crises of Ukraine and the threat of recession can still play out in different ways.

Meanwhile, reassessment of portfolio styles is likely to continue as negative investment performance challenges established trends towards growth and sustainability investing. Crises do tend to generate change and, consequently, change the perceptions of investors, although as active managers will attest, judging that change is not always easy. The burden of potential for investors to capitalize on this change remains as they seek to deliver positive returns versus the passive competition. Most will be hoping that 2023 is a less interesting year.

THIS ARTICLE FIRST APPEARED IN FT ADVISER