Bruce Mehlman, an experienced Washington lobbyist, joins Double Take to discuss the complexities of corporate lobbying in the current political environment, including how businesses are navigating uncertainties and the implications for investors.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Bruce Mehlman, an experienced Washington lobbyist, joins Double Take to discuss the complexities of corporate lobbying in the current political environment, including how businesses are navigating uncertainties and the implications for investors.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Kirsten Bartok Touw, a defence investor and thought leader, joins Double Take to dig into the trenches of US defence spending. She illuminates the need for faster innovation, more autonomous systems and incorporation of commercial technologies.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Kirsten Bartok Touw, a defense investor and thought leader, joins Double Take to dig into the trenches of US defense spending. She illuminates the need for faster innovation, more autonomous systems and incorporation of commercial technologies.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Joe Corrado, a veteran small-cap investor who recently retired from Newton Investment Management, joins Double Take to share his extensive insights on the evolution of small-cap investing and strategies for navigating current market challenges.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Joe Corrado, a veteran small-cap investor who recently retired from Newton Investment Management, joins Double Take to share his extensive insights on the evolution of small-cap investing and strategies for navigating current market challenges.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.

Listen on

Key Points

- The largest technology event of the year introduced several noteworthy innovations that are expected to lead the industry in the coming months.

- Artificial intelligence (AI) is rapidly expanding beyond software into the physical world, as companies across industries harness it to create smarter robots and automated systems that drive unprecedented efficiency, precision and scalability.

- The mobility sector continues to evolve, incorporating advanced autonomous features that improve safety, performance and user experience.

- Electrification is gaining momentum across industries, with innovators meeting growing demands for sustainable, automated and energy-efficient solutions in areas like mining, agriculture and transportation.

The 2025 Consumer Electronics Show (CES), held in Las Vegas in January, showcased cutting-edge innovations, including advanced artificial intelligence (AI), decentralized systems, health technology and humanoid robots, all pointing to the future of living, working and experiencing the world. The overarching message was clear: it is all about AI.

AI has evolved from a standalone category into a technology embedded in nearly every innovation on display. From AI-powered lawn mowers and health diagnostics to next-generation gaming, video editing and customer experience tools, AI has become the core driver of transformation across industries.

One key theme at the conference is the broadening of AI applications. Generative AI—producing new content such as text, images, audio, and video from learned patterns—has been the major driver behind AI’s growth. Agentic AI, which perceives, reasons, plans, and acts autonomously, is now being deployed in more use cases. An AI agent takes inputs and reasons about them and executes actions to pursue objectives. Physical AI involves interacting with the physical environment, such as robots or embedded AI systems that can manipulate objects or navigate spaces, autonomous drones, warehouse robots, and self-driving cars.

Capex: The Race Is On

AI needs facilities, machines and power, and all of that has, in turn, fueled its own new spending involving real estate, building materials, semiconductors and energy. Energy providers have seen a huge boost, because data centers require as much power as a small city. In the AI era, capital expenditure (capex) has come to signify what a company spends on data centers and the components they require. The biggest tech players have increased their capex by tens of billions of dollars this year, and they show no signs of pulling back in 2025.

AI demand is quickly broadening away from enterprise software applications. For example, car manufacturers are likely to maintain two factories: one to build the car, and the other to train autonomous vehicles via simulation and synthetic data—every one million autonomous vehicles may require $2-3 billion in data-center capex to support it. This data-center capacity will be used for data collecting, training, and edge-case development to ensure that autonomous vehicles are functioning at their most efficient and safest levels.

AI Computing and Automation Continues to Mature

CES showcased the rapid evolution of AI and its growing integration into everyday products and services. A major AI company introduced new offerings in personal computing, gaming, robotics and self-driving vehicles. Hardware manufacturers highlighted that advancements in lightweight large language models (LLMs) now enable generative AI capabilities on consumer devices with on-device processing, moving towards ubiquitous AI.

New innovations in personal computing aim to make AI more accessible. A compact AI supercomputer, the size of a modern laptop, can run 200 billion parameter LLMs, empowering professionals and students alike. Users can develop and deploy models on their desktops or in the cloud seamlessly. Advances in PC hardware supporting AI, combined with a large install base ready for an upgrade, suggest a potential PC refresh cycle in 2025.

AI Applications Continue to Progress

As AI hardware gets more efficient, progress on training data and development methods continue to expand AI’s utility. Among the significant announcements at CES was the introduction of models that can generate photorealistic video that developers can use to train their autonomous robots and vehicles at a lower cost than traditional data-collection methods. These models are intended to produce synthetic training data, enabling machines to understand the physical world, much like how LLMs facilitate natural communication for chatbots. This innovation is expected to expand the impacts of AI into robotics research and autonomous driving by addressing the bottleneck of limited data for robotic and self-driving applications.

As vertical specific training data sets proliferate and models become more efficient, agentic AI appears to be much more imminent than previously expected. Numerous attendees highlighted progress in releasing AI assistants, from a system utilizing AI agents to build AI applications that can automate enterprise work, to a simple LLM assisting with the use of household appliances. These AI agents function as knowledge robots capable of reasoning, planning and analyzing large amounts of data to derive real-time insights from various sources such as images, videos and PDF files. While advancements in semiconductors and expansive data center builds have captured a great deal of attention, improvements in data gathering and software architecture have quietly improved model performance to the point where more and more companies are ready to ship to consumers.

Mobility

This year’s transportation industry exhibitors focused on assisted and autonomous driving technologies, with significant advances in autonomous driving. Companies highlighted progress toward level 4 (L4) systems, which can handle unpredictable surroundings without human intervention. Currently, most available systems are L2 and need human backup. Recent US market expansions and potential favorable regulations have renewed the relevance of autonomous vehicles in public markets.

CES showcased autonomous tech across various industries, including long-haul trucking. One company revealed progress towards L4 autonomous trucking, logging 50,000 miles in August 2024. Several firms announced partnerships to speed up L4 semi-truck deployment. These advancements highlight autonomous vehicle investment impacts beyond consumer ridesharing into multiple sectors.

Autonomous vehicle advancement will require improvements in a number of sensor-oriented sub-industries. Light detection and ranging (LiDAR) technology, a cornerstone of autonomous vehicle systems, is experiencing exponential growth in both capability and adoption. CES demonstrations revealed significant price reductions alongside major performance improvements, driving increased integration by automotive manufacturers for both autonomous features and enhanced safety systems. There were additional tech solutions on display that could help accelerate the speed of performance enhancements and the commercialization of driverless vehicle systems.

Robotics

AI advancements are accelerating the robotics industry, enabling the rapid advancement in humanoid robots. Once confined to science fiction, these human-like machines were displayed at CES as tangible, market-ready innovations. Humanoids are creating a favorable investment opportunity across a wide value chain including AI chipmakers, AI model developers, sensor developers, makers of systems for connected devices, and essential component and material suppliers.

One CEO investing heavily behind the robotics theme spoke about the next frontier of AI being physical AI. He believes that given the innovation in AI, we can now start infusing AI models with synthetically generated physical world data to exponentially drive the usefulness of robots. Historically, the lack of physical world data made it hard for robots to fully understand our world, but with these breakthroughs, use cases and the ability of these robots to efficiently tackle them, it has become much more tangible.

Displays also showed how humanoid robots can handle dangerous and repetitive warehouse tasks, including moving heavy containers. The first commercially available humanoid designed for warehouse tasks is being used in pilot programs in the warehouses of a large online retailer. The robot’s success has driven such high demand that the manufacturer is constructing a dedicated factory targeting annual production of 10,000 units.

Investment Implications of AI-Driven Innovations

CES 2025 showcased AI-driven innovations that have significant investment implications across multiple industries. The rapid advancement of AI-powered computing and automation is driving capital toward semiconductor development, cloud computing, and edge AI technologies. Increased demand for high-performance chips and AI-optimized hardware is expected to accelerate investment in fabrication facilities, supply-chain resilience, and next-generation computing architectures. Smart home automation, robotics and AI-integrated consumer electronics are poised for strong growth, attracting investment in companies developing energy-efficient, adaptive technology. The rise of AI-driven health-care solutions, including autonomous medical devices and real-time health monitoring, suggests expanding opportunities in digital health, telemedicine, and biotechnology sectors.

Autonomous mobility, AI-powered logistics and predictive maintenance are driving investments in automotive technology, with a strong focus on electric and self-driving vehicles. The integration of AI in creative industries, from content generation to real-time analytics, signals increased funding toward AI-driven enterprise software and automation tools that enhance productivity. Sustainability was a key theme, with AI-enabled energy management and smart grid innovations attracting investments in renewable energy, battery technology, and carbon-reduction solutions. As AI adoption accelerates across industries, investors are focusing on companies positioned to benefit from automation, data analytics, and intelligent systems. The shift toward AI-driven business models is likely to reshape market dynamics, emphasizing long-term growth potential in AI infrastructure, software, and industry-specific applications. CES 2025 reinforced AI as a defining investment trend, presenting opportunities in sectors undergoing digital transformation and technological disruption.

As AI adoption accelerates across industries, investors are focusing on companies positioned to benefit from automation, data analytics, and intelligent systems. The shift toward AI-driven business models is likely to reshape market dynamics, emphasizing long-term growth potential in AI infrastructure, software, and industry-specific applications. CES 2025 reinforced AI as a defining investment trend, presenting opportunities in sectors undergoing digital transformation and technological disruption.

Key Points

- We believe investors should consider European infrastructure for greater diversification due to favorable valuations and lower exposure to the expensive artificial intelligence (AI) boom in the US.

- Tailwinds for European utilities include government incentives, sector dislocation and rising investment in energy independence.

- Data-center growth is likely to drive significant power demand, creating long-term revenue growth opportunities for utilities and accelerating green-energy investments.

- The Nordic countries, due to their renewable-energy resources, cold climate and strong regulatory frameworks, are well positioned to benefit from the data center and AI boom.

In last year’s blog post, Coming to America: Investing in Utilities, we highlighted the tailwinds for US utility companies that included significant sector dislocation, government decarbonization incentives and investments in energy. However, the winds of change are at work once again, with the same drivers now appearing in Europe. We believe that investors should consider greater exposure to European infrastructure.

The Death of Equity Diversification–A Decade in Review

Global equities have recently hit a series of new all-time highs, as measured by the MSCI World Index, but returns have been led by a handful of large US growth stocks—the ‘magnificent seven’—whose performance has been driven by the promise of future growth from artificial intelligence (AI). These seven stocks have contributed 30% to global equities’ cumulative return of 155% over the past ten years through December 31, 2024, despite comprising only 11% of the benchmark, on average, during the period. The US has contributed 75% of the total returns with an average weight of 56%, while the US information technology sector has contributed 38% of global equity returns, with an average weight of 19%.

Not surprisingly, over the past ten years the US grew from 51% of the global equity market to 65%, while Europe decreased from 22% to 14%. Information technology increased from 14% to 26% of the MSCI World Index, while the combined weight of the industrials, utilities, energy and materials sectors fell from 27% to 20%.

The narrowness of the market rally was even more pronounced in the US, where the magnificent seven stocks contributed 29% of the S&P 500® Index’s cumulative 242% return over the previous ten years through December 31, 2024. The information technology sector grew from 19% of the S&P 500 to 33% over the same period and contributed 42% of S&P 500’s return despite an average weight of 25%. Together, the weight of the industrials, utilities, energy and materials sectors has fallen from 25% of the S&P 500 ten years ago to 15.5% at the end of 2024. The four infrastructure-exposed sectors started 5% bigger than information technology and ended 17% smaller.

New record highs would suggest that the entire US equity market is expensive. However, lack of market breadth has been the key story of the equity rally. The substantial weighting of these stocks has posed a challenge for investors who rely on the S&P 500 for diversification. Specifically, infrastructure stocks have become notably underrepresented within a typical S&P 500 equity allocation.

We suggest that investors seeking greater diversification should consider the infrastructure sector and specifically should look to European infrastructure where valuations have not been amplified by the expensive AI power boom.

2024 in Review

In the year since we published Coming to America: Investing in Utilities, in which we laid out our case for infrastructure investment within the US, the valuation dispersion between US and European utilities has grown. Over the calendar year 2024, the S&P 500 utilities sector appreciated 27% while European utilities were flat. A key driver of the US appreciation and relative outperformance was the significant capital expenditure of US mega-cap technology companies to support the build-out of the AI ecosystem. These investments in infrastructure, especially related to power, show no signs of stopping. Independent power producers and electric-utilities companies have been among the biggest beneficiaries due to the rising demand for electricity. Hyperscalers’ willingness to secure power at above-market rates also plays a role as they seek to ensure the powering of large data centers in support of their AI aspirations.

So, why do we believe now is a good time to allocate to Europe?

European Competitiveness

The key reasons we believe there is opportunity for active managers in European utilities are identical to the reasons we were bullish on the US in 2024:

- Government incentives aimed at decarbonization can provide tailwinds for renewables-exposed utilities.

- We believe there is a significant sector dislocation in European utilities, potentially unlocking opportunity for active managers.

- We believe electrification and investments in energy independence may continue to drive European electric and gas utilities.

European Government Support

We believe that infrastructure support for AI is a global goal essential for maintaining competitiveness in leading-edge technology. In addition, due to data privacy concerns, we believe countries will want to control their own technology and data, which will require them to build data centers domestically. Europe has fallen behind technology leaders in the US and China, and European officials have become more vocal about the need to act. In January 2025, the areas we feel could provide support for European utilities, initially through sentiment and then through revenue and earnings growth, were outlined in the European Commission’s report, A Competitiveness Compass for the EU. In the report, the Commission concludes that Europe “must act now to regain its competitiveness and secure its prosperity.” It cites Europe’s inability to keep pace with other major economies over the past two decades, especially relative to the US in advanced technology owing to a lack of innovation and high regulations.[1] The report outlines key areas of focus and newly instituted acts for the next five years to “reignite economic dynamism,” which we believe will benefit European utilities and other infrastructure companies:

AI Factories Initiative, Q1 2025, and EU Cloud and AI Development Act, Q4 2025-Q1 2026: “Europe needs the computing, cloud and data infrastructures that AI leadership requires…the initiative establishes ‘AI factories’ to boost Europe’s computing power… the Commission will mobilize public and private initiative to establish new AI Gigafactories specialized in training of very large AI models enabling key AI ecosystems throughout the EU.”

Digital Networks Act, Q4 2025: “Closing the innovation gap will require investment in state-of-the-art digital infrastructure, including modern fiber networks, wireless and satellite solutions, investments in 6G and cloud computing capabilities… To correct course, a Digital Networks Act will propose solutions to improve market incentives to build the digital networks of the future.”

Industrial Decarbonization Accelerator Act, Q4 2025, and Electrification Action Plan and European Grids Package, Q1 2026: “This dependence (reliance on fossil fuel for 2/3 of its energy) can only be reduced over time, as a greater share of energy is produced from decarbonized generation in Europe. The EU must thus accelerate the clean energy transition and promote electrification” and “Europe must invest more in modernizing and expanding its network of energy transmission and distribution infrastructure, accelerating investment in electricity, hydrogen and carbon dioxide transport networks as well as storage systems.”

Valuations Favor Europe

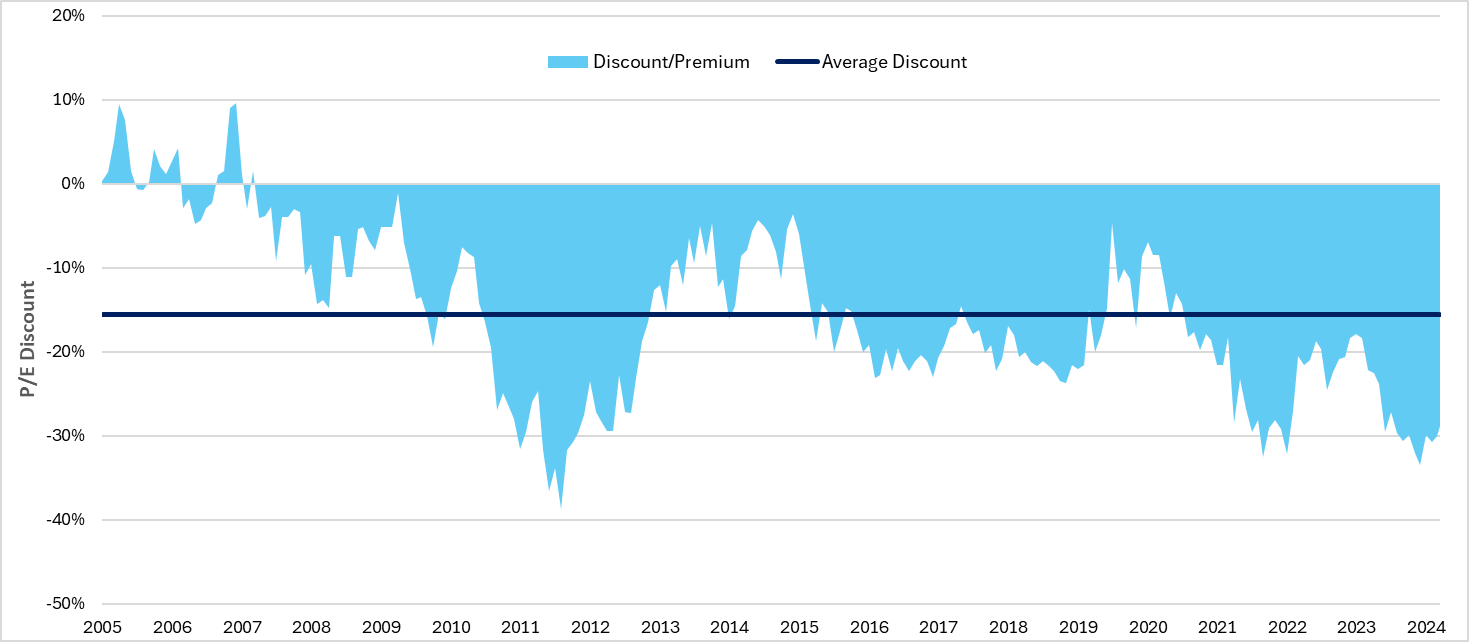

In the past 11 months, price-to-earnings (P/E) ratios of US utilities have rerated by 17% versus 3% for their European counterparts. European utilities currently trade at a 31% P/E discount relative to US utilities, which is more than twice as large as the long-term average of 15%.

European Utilities P/E Discount (-) / Premium (+) Relative to US Utilities

Yield Spreads

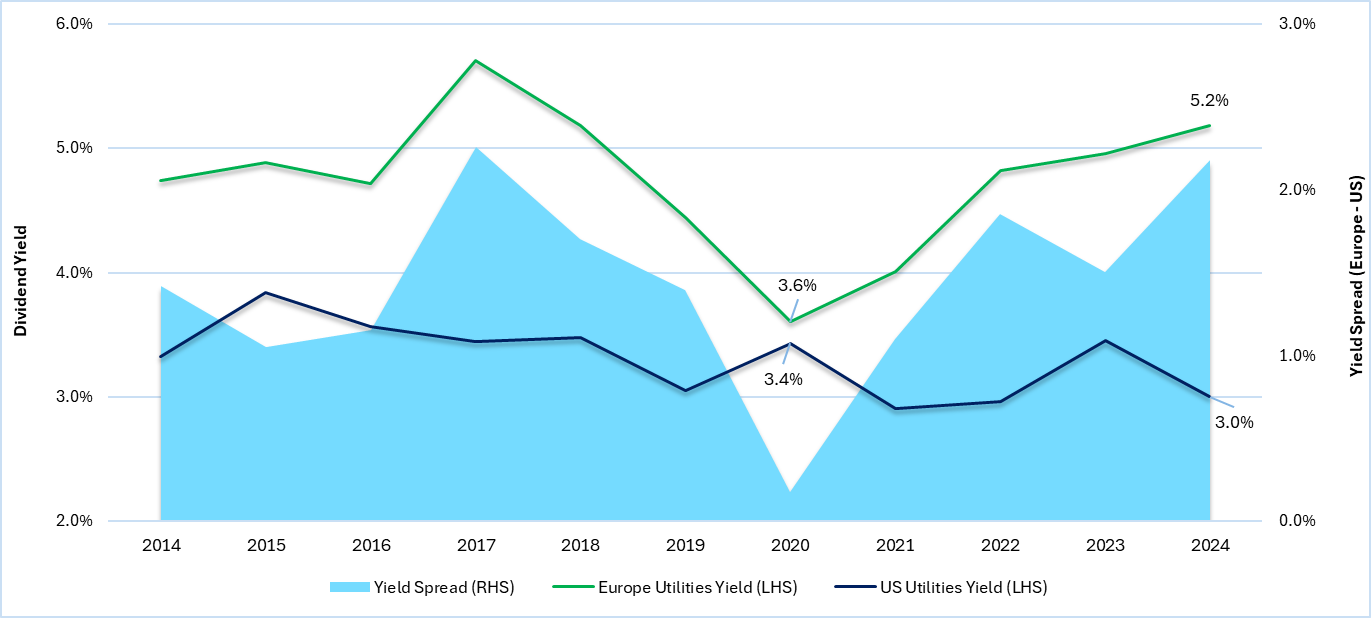

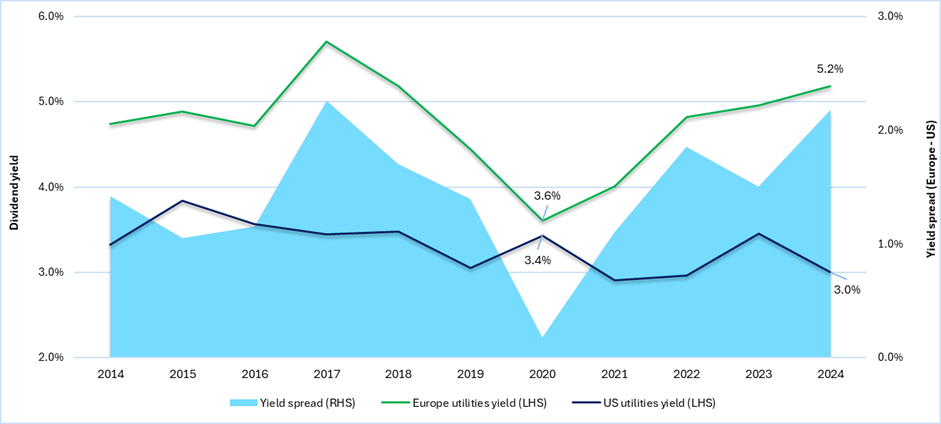

Given the movement in markets, the spread between dividend yields of European and US utilities has moved from 20 basis points (bps) to 220 bps over the past four years, creating opportunities to find promising value investment opportunities in the European utilities sector. This is especially pertinent given the secular tailwinds we expect in the coming year(s), which are identical to the tailwinds that are currently playing out in US markets and driving shares across the infrastructure space.

Dividend Yields and Spread: US vs. Europe

Based on the strength of the US utilities sector driven by the AI power boom, and relative valuations, we have increased our conviction within Europe.

Data Centers Should Create Value

Data-center power demand is surging as the need for greater computing power grows, driven by digitalization, cloud migration and AI. AI is a major contributor to this demand due to its significantly higher power-density requirements stemming from the latest generation of graphics processing unit (GPU) chipsets.

While the growth in data-center build-out may likely be strongest in the US, Europe has ample opportunity to grow its market and further stimulate its technology ecosystem in three key areas:

Increased electricity demand: Data centers are likely to drive a significant rise in power consumption, creating long-term revenue growth opportunities for utilities.

Acceleration of green-energy investments: The shift toward sustainability will spur investment in renewable energy, grid modernization and energy storage solutions.

New infrastructure development: Expanding transmission networks and upgrading substations will be necessary, creating opportunities for infrastructure projects.

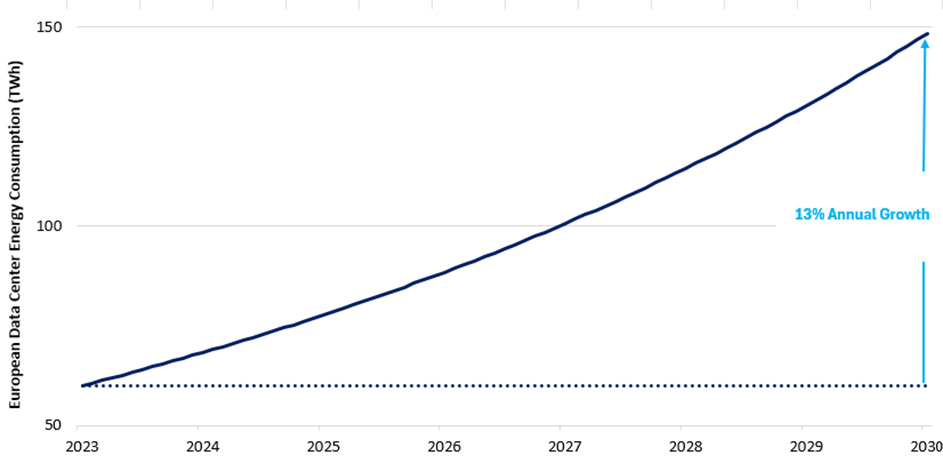

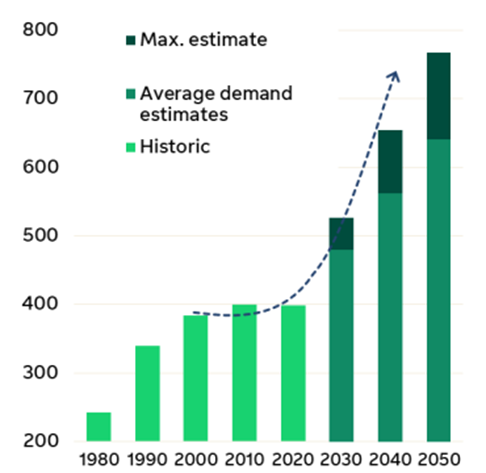

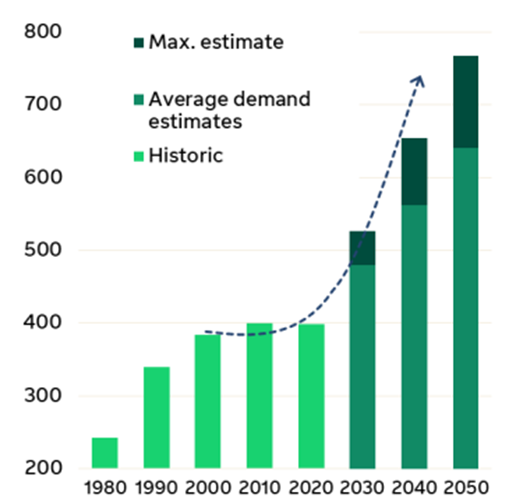

Power Demand for Data Centers is Projected to Rise Materially in Europe

Utility companies that proactively invest in renewable energy, grid capacity and innovative solutions like demand response and energy storage should be well positioned to capitalize on data-center growth. Strategic partnerships with data-center operators and governments will also be crucial to ensuring a stable and sustainable power supply. The most successful European utilities will likely be those that can balance rapid infrastructure expansion with the transition to renewable energy sources, while navigating complex regulatory environments and managing water resources effectively.

Nordic Countries to Benefit

We believe the Nordic countries (Sweden, Norway, Finland, Denmark and Iceland) are exceptionally well positioned to capitalize on the data-center and AI boom for several compelling reasons.

Norway and Sweden have extensive hydropower infrastructure, providing stable, renewable baseload power. Denmark is a leader in wind energy, with offshore wind farms supplying growing portions of its grid. Finland has a diverse energy mix including nuclear, hydro and biomass, which allows data centers to meet their sustainability commitments due to the renewable-rich mix.

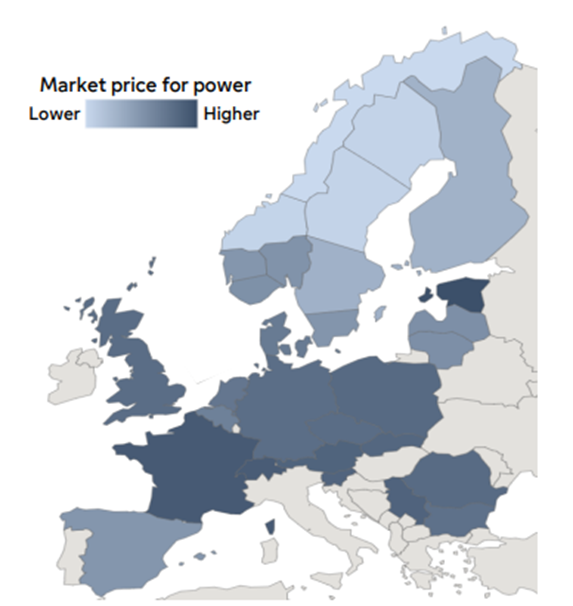

The Nordic Region is a Source for Competitive and Clean Energy

Nordic Power Demand is Driven by Decarbonization and Electrification

Cold ambient temperatures for six to eight months of the year dramatically reduce cooling costs, which typically account for 40% of data-center energy consumption. Several facilities in the region use “free cooling” techniques, drawing cold air or water directly from the environment, representing significant operational cost savings compared to facilities in warmer regions.

Strong regulatory frameworks provide assurance for long-term infrastructure investments, and there is low geopolitical risk compared to many other regions. Additionally, transparent business practices as well as strong workforce education levels and technical expertise, contribute to political and economic stability in the region.

The region boasts excellent fiber-optic infrastructure connecting to major European markets and proximity to submarine cable landing stations for international connectivity. Its strategic position linking Europe to North American markets also enhances its connectivity advantage. Sweden’s “Node Pole” region has attracted major investments from US tech companies.

Norway offers low electricity prices, often 50% lower than the EU average, and 98% renewable generation. Finland provides tax incentives specifically for data centers and direct connections to Russian and Baltic markets. Denmark benefits from strong interconnection with the German grid, providing stability. Iceland has unique geothermal energy resources and 100% renewable electricity.

Seeking Greener Pastures

The global economy is increasingly driven by rapid advancements in technology and infrastructure, with AI and data centers at the forefront. As the demand for energy and technological connectivity grows, strategic investments in infrastructure, particularly renewable energy and grid modernization, become crucial. In our view, Europe, with its government support, competitive advantages and commitment to decarbonization, is well positioned to capitalize on these trends.

In our view, utilities and infrastructure companies that embrace innovation and sustainability should thrive in this evolving landscape. The Nordic countries, with their renewable energy resources, favorable climates and regulatory stability, stand out as leaders in this sector. Investors seeking diversification and growth opportunities should consider the potential of European infrastructure, as it offers promising return potential and can contribute to a more resilient future.

In summary, the intersection of technology and infrastructure presents a unique opportunity for growth and innovation. By investing wisely and strategically, Europe can regain its competitive edge and pave the way for a prosperous future.

[1] Source: European Commission, https://commission.europa.eu/document/download/10017eb1-4722-4333-add2-e0ed18105a34_en

Key points

- We believe investors should consider European infrastructure for greater diversification due to favourable valuations and lower exposure to the expensive artificial intelligence (AI) boom in the US.

- Tailwinds for European utilities include government incentives, sector dislocation and rising investment in energy independence.

- Data-centre growth is likely to drive significant power demand, creating long-term revenue growth opportunities for utilities and accelerating green-energy investments.

- The Nordic countries, due to their renewable-energy resources, cold climate and strong regulatory frameworks, are well-positioned to benefit from the data centre and AI boom.

In 2024, we believed there were tailwinds for US utility companies that included significant sector dislocation, government decarbonisation incentives and investments in energy. However, the winds of change are at work once again, with the same drivers now appearing in Europe. We believe that investors should consider greater exposure to European infrastructure.

The death of equity diversification – A decade in review

Global equities have recently hit a series of new all-time highs, as measured by the MSCI World Index, but returns have been led by a handful of large US growth stocks—the ‘magnificent seven’—whose performance has been driven by the promise of future growth from artificial intelligence (AI). These seven stocks have contributed 30% to global equities’ cumulative return of 155% over the past ten years to 31 December 2024, despite comprising only 11% of the benchmark, on average, during the period. The US has contributed 75% of the total returns with an average weight of 56%, while the US information technology sector has contributed 38% of global equity returns, with an average weight of 19%.

Not surprisingly, over the past ten years the US grew from 51% of the global equity market to 65%, while Europe decreased from 22% to 14%. Information technology increased from 14% to 26% of the MSCI World Index while the combined weight of the industrials, utilities, energy and materials sectors fell from 27% to 20%.

The narrowness of the market rally was even more pronounced in the US, where the magnificent seven stocks contributed 29% of the S&P 500® Index’s cumulative 242% return over the ten years through to 31 December 2024. The information technology sector grew from 19% of the S&P 500 to 33% over the same period and contributed 42% of S&P 500’s return despite an average weight of 25%. Together, the weight of the industrials, utilities, energy and materials sectors has fallen from 25% of the S&P 500 ten years ago to 15.5% at the end of 2024. The four infrastructure-exposed sectors started 5% bigger than information technology and ended 17% smaller.

New record highs would suggest that the entire US equity market is expensive. However, lack of market breadth has been the key story of the equity rally. The substantial weighting of these stocks has posed a challenge for investors who rely on the S&P 500 for diversification. Specifically, infrastructure stocks have become notably underrepresented within a typical S&P 500 equity allocation.

We suggest that investors seeking greater diversification should consider the infrastructure sector and specifically should look to European infrastructure where valuations have not been amplified by the expensive AI power boom.

2024 in review

The valuation dispersion between US and European utilities has recently grown. Over the calendar year 2024, the S&P 500 utilities sector has appreciated 27% while European utilities were flat. A key driver of the US appreciation and relative outperformance was the significant capital expenditure of US mega-cap technology companies to support the build-out of the AI ecosystem. These investments in infrastructure, especially related to power, show no signs of stopping. Independent power producers and electric-utilities companies have been among the biggest beneficiaries due to the rising demand for electricity. Hyperscalers’ willingness to secure power at above-market rates also plays a role as they seek to ensure the powering of large data centres in support of their AI aspirations.

So, why do we believe now is a good time to allocate to Europe?

European competitiveness

The key reasons we believe there is opportunity for active managers in European utilities are identical to the reasons we were bullish on the US in 2024:

- Government incentives aimed at decarbonisation can provide tailwinds for renewables-exposed utilities.

- We believe there is a significant sector dislocation in European utilities, potentially unlocking opportunity for active managers.

- We believe electrification and investments in energy independence may continue to drive European electric and gas utilities.

European government support

We believe that infrastructure support for AI is a global goal essential for maintaining competitiveness in leading-edge technology. In addition, due to data privacy concerns, we believe countries will want to control their own technology and data, which will require them to build data centres domestically. Europe has fallen behind technology leaders in the US and China, and European officials have become more vocal about the need to act. In January 2025, the areas we feel could provide support for European utilities, initially through sentiment and then through revenue and earnings growth, were outlined in the European Commission’s report, A Competitiveness Compass for the EU. In the report, the Commission concludes that Europe “must act now to regain its competitiveness and secure its prosperity”. It cites Europe’s inability to keep pace with other major economies over the past two decades, especially relative to the US in advanced technology owing to a lack of innovation and high regulations.[1] The report outlines key areas of focus and newly instituted acts for the next five years to “reignite economic dynamism”, which we believe will benefit European utilities and other infrastructure companies:

AI Factories Initiative, Q1 2025, and EU Cloud and AI Development Act, Q4 2025-Q1 2026: “Europe needs the computing, cloud and data infrastructures that AI leadership requires…the initiative establishes ‘AI factories’ to boost Europe’s computing power… the Commission will mobilise public and private initiative to establish new AI Gigafactories specialised in training of very large AI models enabling key AI ecosystems throughout the EU.”

Digital Networks Act, Q4 2025: “Closing the innovation gap will require investment in state-of-the-art digital infrastructure, including modern fibre networks, wireless and satellite solutions, investments in 6G and cloud computing capabilities… To correct course, a Digital Networks Act will propose solutions to improve market incentives to build the digital networks of the future.”

Industrial Decarbonisation Accelerator Act, Q4 2025, and Electrification Action Plan and European Grids Package, Q1 2026: “This dependence (reliance on fossil fuel for 2/3 of its energy) can only be reduced over time, as a greater share of energy is produced from decarbonised generation in Europe. The EU must thus accelerate the clean energy transition and promote electrification” and “Europe must invest more in modernising and expanding its network of energy transmission and distribution infrastructure, accelerating investment in electricity, hydrogen and carbon dioxide transport networks as well as storage systems.”

Valuations favour Europe

In the past 11 months, price-to-earnings (P/E) ratios of US utilities have rerated by 17% versus 3% for their European counterparts. European utilities currently trade at a 31% P/E discount relative to US utilities, which is more than twice as large as the long-term average of 15%.

European utilities P/E discount (-) /premium (+) relative to US utilities

Yield spreads

Given the movement in markets, the spread between dividend yields of European and US utilities has moved from 20 basis points (bps) to 220 bps over the past four years, creating opportunities to find promising value investment opportunities in the European utilities sector. This is especially pertinent given the secular tailwinds we expect in the coming year(s), which are identical to the tailwinds that are currently playing out in US markets and driving shares across the infrastructure space.

Dividend yields and spread: US versus Europe

Based on the strength of the US utilities sector driven by the AI power boom, and relative valuations, we have increased our conviction within Europe.

Data centres should create value

Data-centre power demand is surging as the need for greater computing power grows, driven by digitalisation, cloud migration and AI. AI is a major contributor to this demand due to its significantly higher power-density requirements stemming from the latest generation of graphics processing unit (GPU) chipsets.

While the growth in data-centre build-out is likely to be strongest in the US, Europe has ample opportunity to grow its market and further stimulate its technology ecosystem in three key areas:

Increased electricity demand: Data centres are likely to drive a significant rise in power consumption, creating long-term revenue growth opportunities for utilities.

Acceleration of green-energy investments: The shift toward sustainability will spur investment in renewable energy, grid modernisation and energy storage solutions.

New infrastructure development: Expanding transmission networks and upgrading substations will be necessary, creating opportunities for infrastructure projects.

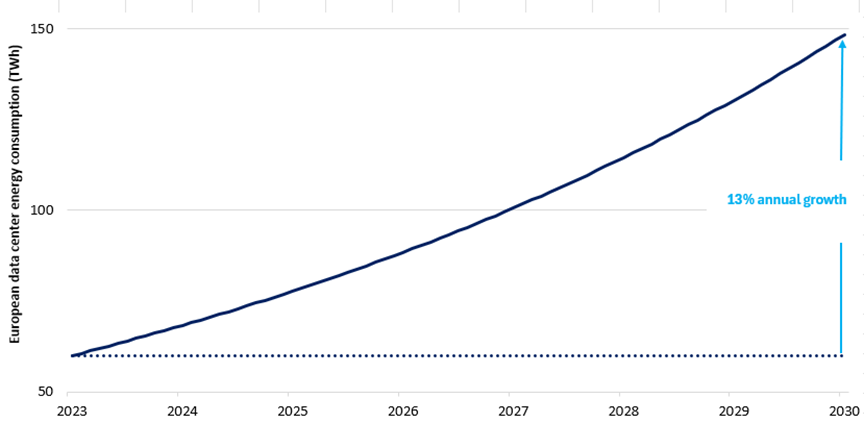

Power demand for data centres is projected to rise materially in Europe

Utility companies that proactively invest in renewable energy, grid capacity and innovative solutions like demand response and energy storage should be well positioned to capitalise on data-centre growth. Strategic partnerships with data-centre operators and governments will also be crucial to ensuring a stable and sustainable power supply. The most successful European utilities are likely to be those that can balance rapid infrastructure expansion with the transition to renewable energy sources, while navigating complex regulatory environments and managing water resources effectively.

Nordic countries to benefit

We believe the Nordic countries (Sweden, Norway, Finland, Denmark and Iceland) are exceptionally well positioned to capitalise on the data-centre and AI boom for several compelling reasons.

Norway and Sweden have extensive hydropower infrastructure, providing stable, renewable baseload power. Denmark is a leader in wind energy, with offshore wind farms supplying growing portions of its grid. Finland has a diverse energy mix including nuclear, hydro and biomass, which allows data centres to meet their sustainability commitments due to the renewable-rich mix.

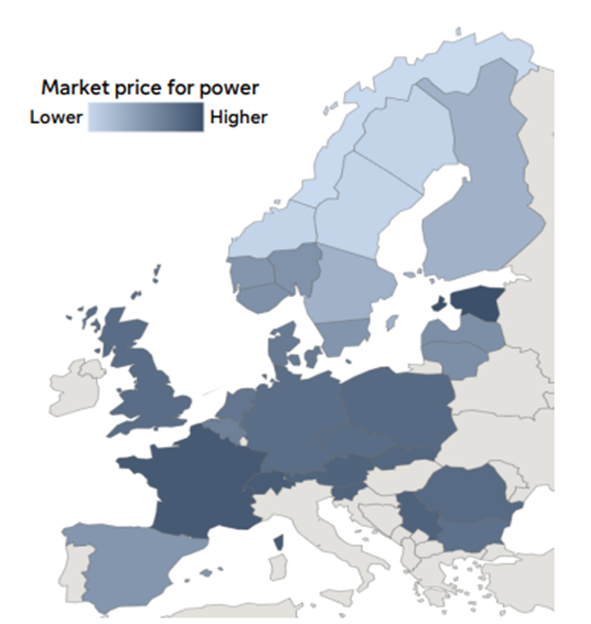

The Nordic region is a source for competitive and clean energy

Nordic power demand is driven by decarbonisation and electrification

Cold ambient temperatures for six to eight months of the year dramatically reduce cooling costs, which typically account for 40% of data-centre energy consumption. Several facilities in the region use ‘free cooling’ techniques, drawing cold air or water directly from the environment, representing significant operational cost savings compared to facilities in warmer regions.

Strong regulatory frameworks provide assurance for long-term infrastructure investments, and there is low geopolitical risk compared to many other regions. Additionally, transparent business practices as well as strong workforce education levels and technical expertise, contribute to political and economic stability in the region.

The region boasts excellent fibre-optic infrastructure connecting to major European markets and proximity to submarine cable landing stations for international connectivity. Its strategic position linking Europe to North American markets also enhances its connectivity advantage. Sweden’s ‘Node Pole’ region has attracted major investments from US tech companies.

Norway offers low electricity prices, often 50% lower than the EU average, and 98% renewable generation. Finland provides tax incentives specifically for data centres and direct connections to Russian and Baltic markets. Denmark benefits from strong interconnection with the German grid, providing stability. Iceland has unique geothermal energy resources and 100% renewable electricity.

Seeking greener pastures

The global economy is increasingly driven by rapid advancements in technology and infrastructure, with AI and data centres at the forefront. As the demand for energy and technological connectivity grows, strategic investments in infrastructure, particularly renewable energy and grid modernisation, become crucial. In our view, Europe, with its government support, competitive advantages and commitment to decarbonisation, is well positioned to capitalise on these trends.

In our view, utilities and infrastructure companies that embrace innovation and sustainability should thrive in this evolving landscape. The Nordic countries, with their renewable energy resources, favourable climates and regulatory stability, stand out as leaders in this sector. Investors seeking diversification and growth opportunities should consider the potential of European infrastructure, as it offers promising return potential and can contribute to a more resilient future.

In summary, the intersection of technology and infrastructure presents a unique opportunity for growth and innovation. By investing wisely and strategically, Europe can regain its competitive edge and pave the way for a prosperous future.

[1] Source: European Commission, https://commission.europa.eu/document/download/10017eb1-4722-4333-add2-e0ed18105a34_en

Paul Stimers, partner at Holland & Knight and founder of the Quantum Industry Coalition, joins Double Take to jump into the quantum advantage, cybersecurity implications and the future of this groundbreaking technology.

The podcast is intended for investment professionals ONLY and should not be construed as investment advice or a recommendation. Any stock examples discussed are given in the context of the theme being explored and the views expressed are those of the presenters at the time of recording.