Key points

- Nature is among the most frequently discussed sustainability topics, and this year the expected evolution and emergence of standards and targets in this area will start to put some structure around nature-related topics.

- We expect there to be further conversations around the risks and opportunities associated with artificial intelligence (AI), particularly from an environmental standpoint.

- Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year.

As we start the new year, there are many environmental, social and governance (ESG)-related topics that we see as being increasingly relevant to investors in 2025. Climate and the energy transition have been important topics of consideration for a few years, and they continue to be prominent, particularly as investors consider transition in the hard-to-abate industries. However, there are several other emerging themes that we anticipate will gain more attention this year.

Nature

Nature is among the most frequently discussed sustainability topics, and in recent years it has steadily grown in importance for investors, particularly as high-profile events, such as the Conference of the Parties (COP), have highlighted the significance of this topic. The introduction of various regulations, such as those related to plastic packaging and waste regulation, as well as the European Union’s (EU) deforestation regulation, have further heightened the materiality of nature for investors.

This year, the expected evolution and emergence of standards and targets in this area should start to put some structure around nature-related topics. The International Sustainability Standards Board (ISSB) is developing standards that will result in a global baseline of sustainability disclosures. The Science-Based Targets Network (SBTN) is currently developing science-based targets for nature both for companies and cities, so that they can comprehensively address their environmental impacts across biodiversity, land and water through the Science Based Targets initiative. Further guidance is expected to be released this year. Additionally, the Taskforce on Nature-related Financial Disclosures (TNFD) has set out recommendations for voluntary nature-related disclosures under the four headings of governance, strategy, risk and impact management, and metrics and targets.

What do these developments mean for us as investors? They do raise the possibility of regular nature-related disclosures by investee companies, meaning we are likely to see more information on this topic. However, this is a complex area, and with little standardisation of measures to report or evaluate this information, we expect that assessing a company’s nature footprint or the financial impact of its nature-related policies will not be straightforward.

In our view, it is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models. Investors will need to develop an understanding of how to consider these disclosures and standards in relation to a company’s business and what should be deemed as good practice.

It is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models.

At Newton, we recognise that a one-size-fits-all approach is not likely to be helpful when considering the impact of nature-related factors on a company’s financials. Therefore, we are building a nature assessment framework to connect the materiality of nature-related factors to a company’s business model.1 The aim of this framework is to help us to identify and analyse companies with material impacts and dependencies, and to understand how robustly they are managing and reducing risks. To determine materiality, we use revenue data, which allows us to have a more granular focus than if we were to use sector or industry mappings. We expect this approach to evolve as our understanding does over the course of this year and beyond.

Artificial intelligence (AI)

AI is set to expand to new areas and enable significant advancements by creating user-friendly connections between people and advanced tech, with productivity and value creation expected to skyrocket across industries. AI is also spreading beyond the technology sector as the second-order impacts are beginning to be felt in areas such as infrastructure, health care, utilities, industrials and nuclear power. There has been significant government support both in the US and in Europe in the form of grants, subsidies and tax incentives offered to boost domestic AI capabilities. As investors weigh the merits of AI, there have also been conversations about its social impacts.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint. Data centres are known to have vast water and energy requirements, and we expect that as more information on this becomes available, there will be greater focus on how data centres can be run efficiently and where they are installed. These factors may well play a part in the investment thesis of a security. This may also spark innovation and create further investment opportunities, such as companies exploring how AI can be powered in a clean, green and speedy way.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint.

Regulatory changes against a shifting geopolitical backdrop

Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year. In the UK, investors will see what impact the Sustainability Disclosure Requirements (SDR) have had on the investment landscape, and the EU is anticipated to streamline its sustainability regulations through an Omnibus Simplification Package to be published early this year. All these developments will have potential implications on the investment landscape from an ESG perspective.

In terms of geopolitics, more voters than ever before participated in elections in 2024 on a global basis. Approximately 49% of the world’s combined population held national elections. The wider implications of these election results are expected to be felt this year.

As countries find their place in the new geopolitical order and as international relationships are reset, there will no doubt be implications for global trade and consequently for the business environment in which companies operate. We must also consider the impact on international treaties, such as the Paris Agreement or those ratified at COP.

Unlocking opportunity

As we consider these topics, it is clear to us that 2025 is going to be a year of change, and as history has taught us, such change presents both opportunities and risks. We are confident in our approach of combining data-driven insights with qualitative analysis while navigating this environment and providing useful ESG insights to fuel our multidimensional research.

1Note: Scores are only produced where sufficient data is available and may not be available for all equity investments. Where this is the case, the nature analysis will rely predominantly on qualitative research completed by Newton’s responsible investment team.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Key Points

- Nature is among the most frequently discussed sustainability topics, and this year the expected evolution and emergence of standards and targets in this area will start to put some structure around nature-related topics.

- We expect there to be further conversations around the risks and opportunities associated with artificial intelligence (AI), particularly from an environmental standpoint.

- Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year.

As we start the new year, there are many environmental, social and governance (ESG)-related topics that we see as being increasingly relevant to investors in 2025. Climate and the energy transition have been important topics of consideration for a few years, and they continue to be prominent, particularly as investors consider transition in the hard-to-abate industries. However, there are several other emerging themes that we anticipate will gain more attention this year.

Nature

Nature is among the most frequently discussed sustainability topics, and in recent years it has steadily grown in importance for investors, particularly as high-profile events, such as the Conference of the Parties (COP), have highlighted the significance of this topic. The introduction of various regulations, such as those related to plastic packaging and waste regulation, as well as the European Union’s (EU) deforestation regulation, have further heightened the materiality of nature for investors.

This year, the expected evolution and emergence of standards and targets in this area should start to put some structure around nature-related topics. The International Sustainability Standards Board (ISSB) is developing standards that will result in a global baseline of sustainability disclosures. The Science-Based Targets Network (SBTN) is currently developing science-based targets for nature both for companies and cities, so that they can comprehensively address their environmental impacts across biodiversity, land and water through the Science Based Targets initiative. Further guidance is expected to be released this year. Additionally, the Taskforce on Nature-related Financial Disclosures (TNFD) has set out recommendations for voluntary nature-related disclosures under the four headings of governance, strategy, risk and impact management, and metrics and targets.

What do these developments mean for us as investors? They do raise the possibility of regular nature-related disclosures by investee companies, meaning we are likely to see more information on this topic. However, this is a complex area, and with little standardization of measures to report or evaluate this information, we expect that assessing a company’s nature footprint or the financial impact of its nature-related policies will not be straightforward.

In our view, it is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models. Investors will need to develop an understanding of how to consider these disclosures and standards in relation to a company’s business and what should be deemed as good practice.

It is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models.

At Newton, we recognize that a one-size-fits-all approach is not likely to be helpful when considering the impact of nature-related factors on a company’s financials. Therefore, we are building a nature assessment framework to connect the materiality of nature-related factors to a company’s business model.1 The aim of this framework is to help us to identify and analyze companies with material impacts and dependencies, and to understand how robustly they are managing and reducing risks. To determine materiality, we use revenue data, which allows us to have a more granular focus than if we were to use sector or industry mappings. We expect this approach to evolve as our understanding does over the course of this year and beyond.

Artificial Intelligence (AI)

AI is set to expand to new areas and enable significant advancements by creating user-friendly connections between people and advanced tech, with productivity and value creation expected to skyrocket across industries. AI is also spreading beyond the technology sector as the second-order impacts are beginning to be felt in areas such as infrastructure, health care, utilities, industrials and nuclear power. There has been significant government support both in the US and in Europe in the form of grants, subsidies and tax incentives offered to boost domestic AI capabilities. As investors weigh the merits of AI, there have also been conversations about its social impacts.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint. Data centers are known to have vast water and energy requirements, and we expect that as more information on this becomes available, there will be greater focus on how data centers can be run efficiently and where they are installed. These factors may well play a part in the investment thesis of a security. This may also spark innovation and create further investment opportunities, such as companies exploring how AI can be powered in a clean, green and speedy way.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint.

Regulatory Changes Against a Shifting Geopolitical Backdrop

Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year. In the UK, investors will see what impact the Sustainability Disclosure Requirements (SDR) have had on the investment landscape, and the EU is anticipated to streamline its sustainability regulations through an Omnibus Simplification Package to be published early this year. All these developments will have potential implications on the investment landscape from an ESG perspective.

In terms of geopolitics, more voters than ever before participated in elections in 2024 on a global basis. Approximately 49% of the world’s combined population held national elections. The wider implications of these election results are expected to be felt this year.

As countries find their place in the new geopolitical order and as international relationships are reset, there will no doubt be implications for global trade and consequently for the business environment in which companies operate. We must also consider the impact on international treaties, such as the Paris Agreement or those ratified at COP.

Unlocking Opportunity

As we consider these topics, it is clear to us that 2025 is going to be a year of change, and as history has taught us, such change presents both opportunities and risks. We are confident in our approach of combining data-driven insights with qualitative analysis while navigating this environment and providing useful ESG insights to fuel our multidimensional research.

1 Scores are only produced where sufficient data is available and may not be available for all equity investments. Where this is the case, the nature analysis will rely predominantly on qualitative research completed by Newton’s responsible investment team.

Key points

- Nature is among the most frequently discussed sustainability topics, and this year the expected evolution and emergence of standards and targets in this area will start to put some structure around nature-related topics.

- We expect there to be further conversations around the risks and opportunities associated with artificial intelligence (AI), particularly from an environmental standpoint.

- Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year.

As we start the new year, there are many environmental, social and governance (ESG)-related topics that we see as being increasingly relevant to investors in 2025. Climate and the energy transition have been important topics of consideration for a few years, and they continue to be prominent, particularly as investors consider transition in the hard-to-abate industries. However, there are several other emerging themes that we anticipate will gain more attention this year.

Nature

Nature is among the most frequently discussed sustainability topics, and in recent years it has steadily grown in importance for investors, particularly as high-profile events, such as the Conference of the Parties (COP), have highlighted the significance of this topic. The introduction of various regulations, such as those related to plastic packaging and waste regulation, as well as the European Union’s (EU) deforestation regulation, have further heightened the materiality of nature for investors.

This year, the expected evolution and emergence of standards and targets in this area should start to put some structure around nature-related topics. The International Sustainability Standards Board (ISSB) is developing standards that will result in a global baseline of sustainability disclosures. The Science-Based Targets Network (SBTN) is currently developing science-based targets for nature both for companies and cities, so that they can comprehensively address their environmental impacts across biodiversity, land and water through the Science Based Targets initiative. Further guidance is expected to be released this year. Additionally, the Taskforce on Nature-related Financial Disclosures (TNFD) has set out recommendations for voluntary nature-related disclosures under the four headings of governance, strategy, risk and impact management, and metrics and targets.

What do these developments mean for us as investors? They do raise the possibility of regular nature-related disclosures by investee companies, meaning we are likely to see more information on this topic. However, this is a complex area, and with little standardisation of measures to report or evaluate this information, we expect that assessing a company’s nature footprint or the financial impact of its nature-related policies will not be straightforward.

In our view, it is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models. Investors will need to develop an understanding of how to consider these disclosures and standards in relation to a company’s business and what should be deemed as good practice.

It is likely this year that nature moves from being a topic that investors seek to better understand, to one for which there is a recognition that investment conversations need to go deeper towards determining the optimal standards for different business models.

At Newton, we recognise that a one-size-fits-all approach is not likely to be helpful when considering the impact of nature-related factors on a company’s financials. Therefore, we are building a nature assessment framework to connect the materiality of nature-related factors to a company’s business model.1 The aim of this framework is to help us to identify and analyse companies with material impacts and dependencies, and to understand how robustly they are managing and reducing risks. To determine materiality, we use revenue data, which allows us to have a more granular focus than if we were to use sector or industry mappings. We expect this approach to evolve as our understanding does over the course of this year and beyond.

Artificial intelligence (AI)

AI is set to expand to new areas and enable significant advancements by creating user-friendly connections between people and advanced tech, with productivity and value creation expected to skyrocket across industries. AI is also spreading beyond the technology sector as the second-order impacts are beginning to be felt in areas such as infrastructure, health care, utilities, industrials and nuclear power. There has been significant government support both in the US and in Europe in the form of grants, subsidies and tax incentives offered to boost domestic AI capabilities. As investors weigh the merits of AI, there have also been conversations about its social impacts.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint. Data centres are known to have vast water and energy requirements, and we expect that as more information on this becomes available, there will be greater focus on how data centres can be run efficiently and where they are installed. These factors may well play a part in the investment thesis of a security. This may also spark innovation and create further investment opportunities, such as companies exploring how AI can be powered in a clean, green and speedy way.

We expect there to be further conversations around the risks and opportunities associated with AI this year, particularly from an environmental standpoint.

Regulatory changes against a shifting geopolitical backdrop

Significant changes in terms of regulation as well as geopolitics are expected to start to take shape this year. In the UK, investors will see what impact the Sustainability Disclosure Requirements (SDR) have had on the investment landscape, and the EU is anticipated to streamline its sustainability regulations through an Omnibus Simplification Package to be published early this year. All these developments will have potential implications on the investment landscape from an ESG perspective.

In terms of geopolitics, more voters than ever before participated in elections in 2024 on a global basis. Approximately 49% of the world’s combined population held national elections. The wider implications of these election results are expected to be felt this year.

As countries find their place in the new geopolitical order and as international relationships are reset, there will no doubt be implications for global trade and consequently for the business environment in which companies operate. We must also consider the impact on international treaties, such as the Paris Agreement or those ratified at COP.

Unlocking opportunity

As we consider these topics, it is clear to us that 2025 is going to be a year of change, and as history has taught us, such change presents both opportunities and risks. We are confident in our approach of combining data-driven insights with qualitative analysis while navigating this environment and providing useful ESG insights to fuel our multidimensional research.

1 Note: Scores are only produced where sufficient data is available and may not be available for all equity investments. Where this is the case, the nature analysis will rely predominantly on qualitative research completed by Newton’s responsible investment team.

Key points

- Nature and biodiversity are growing in importance for investors, particularly as high-profile events and the introduction of various regulations have heightened their materiality.

- Biodiversity COP16, which recently took place in Cali, Colombia, highlighted key nature-related issues which could have significant investment implications, but also brought to light the progress yet to be made in terms of implementation.

- Our approach enables us to focus on our understanding of the risks and opportunities related to nature, by assessing the impacts and dependencies as part of our investment research process.1

- We are building on this approach to create a nature assessment framework to connect materiality to the management of companies.

Increasing focus on nature

Nature and biodiversity, along with climate, are among the most frequently discussed sustainability topics. The Dasgupta Review, an independent review on the economics of biodiversity commissioned by the UK Treasury and published in 2021, highlighted the macro-level connection between nature and economics, and brought these issues to the forefront. Since then, significant events such as the fines imposed on chemical manufacturer 3M for water pollution linked to ‘forever chemicals’ have emphasised the importance of nature and biodiversity. The introduction of various regulations, including those related to plastic packaging and waste regulation, as well as the European Union deforestation regulation, have further heightened the materiality of nature and biodiversity.

According to our analysis of data from environmental reporting organisation CDP (formerly the Carbon Disclosure Project), 2025 is set to be a critical milestone for corporate sustainability targets, with nearly 40% of close to 1,000 targets analysed committed to setting specific goals for next year. While a signal of encouraging momentum, it brings to light the potential risks involved in measuring companies’ performance in meeting these targets, and the extent to which failures would undermine collective efforts to protect nature and biodiversity at a global scale.

COP16 – a turning point?

The 16th meeting of the Conference of the Parties (COP) to the Convention on Biological Diversity (CBD) took place recently in Cali, Colombia, a location known for its rich biodiversity. The conference continued the momentum from the previous biodiversity COP in 2022, which underlined the need to preserve biodiversity following the implementation of the Kunming-Montreal Global Biodiversity Framework (GBF), a set of international goals which aim to halt and reverse nature loss.

One of the target headlines set through the GBF was the ‘30 by 30’ initiative, a conservation target calling for 30% of the earth’s land and water to be conserved by 2030 through the establishment of protected areas and other area-based conservation measures. A key aim of COP16 was to turn these ambitions into action by outlining the necessary steps for countries and establishing a framework for monitoring progress.

Priority areas for COP16 included achieving financial commitments for conservation, addressing concerns around biopiracy (the exploitation of biological resources by corporations and researchers), and ensuring the involvement of indigenous communities in decision-making processes.

COP16 highlighted several pivotal discussions for investors as biodiversity becomes increasingly integral to sustainable finance and regulatory landscapes:

- Resource mobilisation and financing gap: There is estimated to be a $700bn financing gap – the amount required to restore nature – which underscores a major opportunity and obligation for private sector engagement in biodiversity.2 While some private pledges have been made, the scale of financing required indicates that current efforts are insufficient.

- Leadership and policy stability: The divide between developed and developing countries on financing and governance approaches will affect the regulatory backdrop for biodiversity investments. A lack of decisive leadership may delay the establishment of consistent standards and frameworks, which are critical for investor confidence. There is a range of investor standards which evolve in parallel, such as the Science-Based Targets for Nature, the Taskforce on Nature-related Financial Disclosures (TNFD), and the International Sustainability Standards Board research consultation. These emphasise the connection between nature and climate, with the two often being described as ‘two sides of the same coin’, and companies will need to organise their integration efforts across both fronts.

- Mandatory reporting and corporate engagement: A key focus of COP16 was the need for governments to provide more clarity on how they will implement their targets, and countries were expected to submit updates to their National Biodiversity Strategies and Action Plans (NBSAPs). These plans may directly affect private and public capital allocation, as governments continue to address the material risks of biodiversity loss. Investors should watch for how these NBSAPs evolve, as they may lead to reporting requirements like climate disclosures, such as those of the TNFD. As NBSAPs are implemented, businesses will increasingly be expected to understand their impacts and dependencies on biodiversity and incorporate considerations into their operations, which will require additional expertise and supply-chain adjustments, with potential changes to capital-expenditure decisions.

- Market and product innovation: As discussions about biodiversity credits and other nature finance mechanisms continue, investors can look forward to the development of new financial products and instruments. These innovations could provide alternative returns while supporting environmental objectives, similar to carbon credits, but specifically tailored for biodiversity outcomes.

The discussions at COP16 mark a pivotal moment that could see the shift in biodiversity finance from a niche interest to a mainstream investment priority. However, although billed as the ‘implementation COP’, COP16 has fallen short of expectations. While notable progress was made on key issues like benefit sharing from genetic resource use, critical agreements on resource mobilisation and monitoring frameworks were not reached. This gap casts doubt on the feasibility of achieving the ambitious 2030 biodiversity targets unless significant strides are made at the upcoming interim meeting in Bangkok next year, ahead of COP17 in Armenia in 2026.

The discussions at COP16 mark a pivotal moment that could see the shift in biodiversity finance from a niche interest to a mainstream investment priority.

Despite these challenges, the evolving regulatory landscape presents investors with the opportunity to position themselves at the forefront of this growing sector. By recognising and acting on these developments, investors can contribute to and benefit from the transition towards sustainable biodiversity finance.

Linking nature to investments

Given the increased complexity of nature, we have established a dedicated working group to better understand the topic and to develop our approach. This enables us to focus on our understanding of the risks and opportunities related to nature,3 by assessing the impacts and dependencies as part of our investment research process. It also informs other responsible-investment-related thematic research,4 and we hope that in the future it can be used to meet specific client demands and expectations on nature, including considering real-world outcomes.

Impacts on nature are not fungible like emissions. For example, the loss of one species cannot be offset by conservation gains made in another, and polluting water sources in two different regions can have completely different impacts on the biodiversity in those areas. This means that geospatial and location-based aspects are important to consider.

We think that it is important to break down nature impacts into components using the direct drivers outlined by the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services, a leading authority on the science of biodiversity and public policy responses. Unlike climate, we cannot focus on only one measure. Although aggregate measures such as the potentially disappeared fraction of species and mean species abundance exist, we believe these mask the underlying crucial details that provide investment insight, such as materiality and how companies are managing risks.

We believe in a materiality-driven approach; we want to be able to identify and analyse companies with material impacts and dependencies, and understand how robustly they are managing and reducing risks. Given that the entire economic system is based on using natural resources and ecosystems, there can be differences in the extent and type of materiality, but it is extremely difficult to take an exclusionary approach to this.

We believe in a materiality-driven approach; we want to be able to identify and analyse companies with material impacts and dependencies, and understand how robustly they are managing and reducing risks.

Where clients may specifically look to achieve outcomes related to nature, we think that taking into account materiality and using this to assess companies’ practices is the best way to seek these outcomes in listed markets. Solutions providers are typically private or small components of larger conglomerates; however, investors can engage with companies which have a material impact on nature and invest in those doing the most to mitigate this.

Assessing companies on nature

Using this approach, we are building a nature assessment framework5 to connect materiality to the management of companies. To determine materiality, we use revenue data, which allows us to have a more granular focus than if we were to use sector or industry mappings.

Building on this, we can assess companies to identify those with the most robust practices by breaking nature down into its tangible components, such as water scarcity, water quality and deforestation. This requires a deep understanding of each of these components, which is where it provides the most investment insight relevant to decision-making, research and engagement.

We consider that our analytics capability is a differentiator as it allows us to build an understanding of how to use unstructured and inconsistently disclosed data in a way that can be meaningful to investments. This approach has been built to evolve as our understanding does.

- Newton manages a variety of investment strategies. How ESG analysis is integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved. Newton does not currently view certain types of investments as presenting ESG risks and opportunities and believes it is not practicable to evaluate such risks and opportunities for certain other investments. Where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions.

- Source: Biodiversity Finance Trends Dashboard 2024, Department for Environment Food & Rural Affairs, GOV.UK: https://www.gov.uk/government/publications/biodiversity-finance-trends-2024/biodiversity-finance-trends-dashboard-2024-accessible-version

- Newton manages a variety of investment strategies. How ESG analysis is integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved. Newton does not currently view certain types of investments as presenting ESG risks and opportunities and believes it is not practicable to evaluate such risks and opportunities for certain other investments. Where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions.

- Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic structure the security has been assigned to.

- Scores are only produced where sufficient data is available and may not be available for all equity investments. Where this is the case, the nature analysis will rely predominantly on qualitative research completed by Newton’s responsible investment team.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Key points

- Nature and biodiversity are growing in importance for investors, particularly as high-profile events and the introduction of various regulations have heightened their materiality.

- Biodiversity COP16, which recently took place in Cali, Colombia, highlighted key nature-related issues which could have significant investment implications, but also brought to light the progress yet to be made in terms of implementation.

- Our approach enables us to focus on our understanding of the risks and opportunities related to nature, by assessing the impacts and dependencies as part of our investment research process.1

- We are building on this approach to create a nature assessment framework to connect materiality to the management of companies.

Increasing focus on nature

Nature and biodiversity, along with climate, are among the most frequently discussed sustainability topics. The Dasgupta Review, an independent review on the economics of biodiversity commissioned by the UK Treasury and published in 2021, highlighted the macro-level connection between nature and economics, and brought these issues to the forefront. Since then, significant events such as the fines imposed on chemical manufacturer 3M for water pollution linked to ‘forever chemicals’ have emphasised the importance of nature and biodiversity. The introduction of various regulations, including those related to plastic packaging and waste regulation, as well as the European Union deforestation regulation, have further heightened the materiality of nature and biodiversity.

According to our analysis of data from environmental reporting organisation CDP (formerly the Carbon Disclosure Project), 2025 is set to be a critical milestone for corporate sustainability targets, with nearly 40% of close to 1,000 targets analysed committed to setting specific goals for next year. While a signal of encouraging momentum, it brings to light the potential risks involved in measuring companies’ performance in meeting these targets, and the extent to which failures would undermine collective efforts to protect nature and biodiversity at a global scale.

COP16 – a turning point?

The 16th meeting of the Conference of the Parties (COP) to the Convention on Biological Diversity (CBD) took place recently in Cali, Colombia, a location known for its rich biodiversity. The conference continued the momentum from the previous biodiversity COP in 2022, which underlined the need to preserve biodiversity following the implementation of the Kunming-Montreal Global Biodiversity Framework (GBF), a set of international goals which aim to halt and reverse nature loss.

One of the target headlines set through the GBF was the ‘30 by 30’ initiative, a conservation target calling for 30% of the earth’s land and water to be conserved by 2030 through the establishment of protected areas and other area-based conservation measures. A key aim of COP16 was to turn these ambitions into action by outlining the necessary steps for countries and establishing a framework for monitoring progress.

Priority areas for COP16 included achieving financial commitments for conservation, addressing concerns around biopiracy (the exploitation of biological resources by corporations and researchers), and ensuring the involvement of indigenous communities in decision-making processes.

COP16 highlighted several pivotal discussions for investors as biodiversity becomes increasingly integral to sustainable finance and regulatory landscapes:

- Resource mobilisation and financing gap: There is estimated to be a $700bn financing gap – the amount required to restore nature – which underscores a major opportunity and obligation for private sector engagement in biodiversity.2 While some private pledges have been made, the scale of financing required indicates that current efforts are insufficient.

- Leadership and policy stability: The divide between developed and developing countries on financing and governance approaches will affect the regulatory backdrop for biodiversity investments. A lack of decisive leadership may delay the establishment of consistent standards and frameworks, which are critical for investor confidence. There is a range of investor standards which evolve in parallel, such as the Science-Based Targets for Nature, the Taskforce on Nature-related Financial Disclosures (TNFD), and the International Sustainability Standards Board research consultation. These emphasise the connection between nature and climate, with the two often being described as ‘two sides of the same coin’, and companies will need to organise their integration efforts across both fronts.

- Mandatory reporting and corporate engagement: A key focus of COP16 was the need for governments to provide more clarity on how they will implement their targets, and countries were expected to submit updates to their National Biodiversity Strategies and Action Plans (NBSAPs). These plans may directly affect private and public capital allocation, as governments continue to address the material risks of biodiversity loss. Investors should watch for how these NBSAPs evolve, as they may lead to reporting requirements like climate disclosures, such as those of the TNFD. As NBSAPs are implemented, businesses will increasingly be expected to understand their impacts and dependencies on biodiversity and incorporate considerations into their operations, which will require additional expertise and supply-chain adjustments, with potential changes to capital-expenditure decisions.

- Market and product innovation: As discussions about biodiversity credits and other nature finance mechanisms continue, investors can look forward to the development of new financial products and instruments. These innovations could provide alternative returns while supporting environmental objectives, similar to carbon credits, but specifically tailored for biodiversity outcomes.

The discussions at COP16 mark a pivotal moment that could see the shift in biodiversity finance from a niche interest to a mainstream investment priority. However, although billed as the ‘implementation COP’, COP16 has fallen short of expectations. While notable progress was made on key issues like benefit sharing from genetic resource use, critical agreements on resource mobilisation and monitoring frameworks were not reached. This gap casts doubt on the feasibility of achieving the ambitious 2030 biodiversity targets unless significant strides are made at the upcoming interim meeting in Bangkok next year, ahead of COP17 in Armenia in 2026.

The discussions at COP16 mark a pivotal moment that could see the shift in biodiversity finance from a niche interest to a mainstream investment priority.

Despite these challenges, the evolving regulatory landscape presents investors with the opportunity to position themselves at the forefront of this growing sector. By recognising and acting on these developments, investors can contribute to and benefit from the transition towards sustainable biodiversity finance.

Linking nature to investments

Given the increased complexity of nature, we have established a dedicated working group to better understand the topic and to develop our approach. This enables us to focus on our understanding of the risks and opportunities related to nature,3 by assessing the impacts and dependencies as part of our investment research process. It also informs other responsible-investment-related thematic research,4 and we hope that in the future it can be used to meet specific client demands and expectations on nature, including considering real-world outcomes.

Impacts on nature are not fungible like emissions. For example, the loss of one species cannot be offset by conservation gains made in another, and polluting water sources in two different regions can have completely different impacts on the biodiversity in those areas. This means that geospatial and location-based aspects are important to consider.

We think that it is important to break down nature impacts into components using the direct drivers outlined by the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services, a leading authority on the science of biodiversity and public policy responses. Unlike climate, we cannot focus on only one measure. Although aggregate measures such as the potentially disappeared fraction of species and mean species abundance exist, we believe these mask the underlying crucial details that provide investment insight, such as materiality and how companies are managing risks.

We believe in a materiality-driven approach; we want to be able to identify and analyse companies with material impacts and dependencies, and understand how robustly they are managing and reducing risks. Given that the entire economic system is based on using natural resources and ecosystems, there can be differences in the extent and type of materiality, but it is extremely difficult to take an exclusionary approach to this.

We believe in a materiality-driven approach; we want to be able to identify and analyse companies with material impacts and dependencies, and understand how robustly they are managing and reducing risks.

Where clients may specifically look to achieve outcomes related to nature, we think that taking into account materiality and using this to assess companies’ practices is the best way to seek these outcomes in listed markets. Solutions providers are typically private or small components of larger conglomerates; however, investors can engage with companies which have a material impact on nature and invest in those doing the most to mitigate this.

Assessing companies on nature

Using this approach, we are building a nature assessment framework5 to connect materiality to the management of companies. To determine materiality, we use revenue data, which allows us to have a more granular focus than if we were to use sector or industry mappings.

Building on this, we can assess companies to identify those with the most robust practices by breaking nature down into its tangible components, such as water scarcity, water quality and deforestation. This requires a deep understanding of each of these components, which is where it provides the most investment insight relevant to decision-making, research and engagement.

We consider that our analytics capability is a differentiator as it allows us to build an understanding of how to use unstructured and inconsistently disclosed data in a way that can be meaningful to investments. This approach has been built to evolve as our understanding does.

- Newton manages a variety of investment strategies. How ESG analysis is integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved. Newton does not currently view certain types of investments as presenting ESG risks and opportunities and believes it is not practicable to evaluate such risks and opportunities for certain other investments. Where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions.

- Source: Biodiversity Finance Trends Dashboard 2024, Department for Environment Food & Rural Affairs, GOV.UK: https://www.gov.uk/government/publications/biodiversity-finance-trends-2024/biodiversity-finance-trends-dashboard-2024-accessible-version

- Newton manages a variety of investment strategies. How ESG analysis is integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved. Newton does not currently view certain types of investments as presenting ESG risks and opportunities and believes it is not practicable to evaluate such risks and opportunities for certain other investments. Where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions.

- Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic structure the security has been assigned to.

- Scores are only produced where sufficient data is available and may not be available for all equity investments. Where this is the case, the nature analysis will rely predominantly on qualitative research completed by Newton’s responsible investment team.

Key points

- Last year, the Tokyo Stock Exchange (TSE) announced stricter listing requirements and disclosure rules, with the aim of reversing the ‘value-trap’ reputation of the Japanese market.

- The TSE’s request for companies to disclose their plans to improve their capital efficiency has been misinterpreted by some as a focus simply on the price-to-book ratio (PBR).

- The changes have been somewhat effective in driving up the volume of disclosures, but the quality of disclosures generally leaves much room for improvement, in our view.

- However, disclosure alone will not be sufficient to change valuations; companies will have to appropriately assess and act on the reasons for current valuation levels.

What do recent reforms mean for Japanese companies?

Japanese corporate governance reforms have generated significant market interest over the years. These reforms have included the adoption and subsequent revisions of the stewardship code and corporate governance code which promoted board independence and diversity, and aimed to make boards more accountable and increase alignment with shareholders. Both domestic and international investors have closely followed market developments with the view that changes in disclosures, governance practices and corporate structures could improve the relatively lower valuations of Japanese stocks and attract investors to the region.

The updates to listing requirements announced in 2023 have again attracted attention. The Tokyo Stock Exchange (TSE) has tightened its listing criteria, encouraged companies to disclose plans to increase their capital efficiency, and announced stricter rules around diversity, disclosure and sustainability. The aim of the TSE reforms is to reverse the long-held ‘value-trap’ reputation of the Japanese market by urging listed companies “to be proactive in enhancing medium- to long-term value”1 and ultimately to attract global investors. To support this, the TSE also ruled that the companies listed in its top-tier ‘Prime’ market should make key disclosures simultaneously in English and Japanese from March 2025.

The disclosures on increasing capital efficiency are not a mandatory requirement, and there is no punishment imposed on the companies that fail to provide these details. However, the TSE is using an approach that is likely to encourage companies to make these disclosures voluntarily, such as sharing anonymous case studies online, highlighting strong disclosures, and publishing lists of disclosers. Next, it plans to broaden its scope to call out poor quality disclosures. With companies keen to be seen as setting a good example, this approach by the TSE may prove to be effective in the long run.

During a research trip to Japan, members of our responsible investment team and their Japan-based investment colleagues met the TSE, alongside other companies, to better understand the potential investment implications and opportunities associated with the change and to provide investor feedback from both Japanese and global perspectives.

Misplaced focus on PBR1

One of the most interesting takeaways of our research was that the TSE reforms have been misunderstood in some ways, both domestically and internationally. The TSE’s drive to encourage companies to prioritise their capital efficiency and to increase their book value seems to have been interpreted by parts of the market and the media as a focus on just one measure – the price-to-book ratio (PBR). Following the TSE’s announcements, ‘PBR1’, which refers to the PBR of companies for which the ratio is below 1, has become a buzzword. While the PBR has been highlighted because it is easy to understand, the TSE is not intending to mandate one measure or a specific threshold (such as a PBR of less than 1). There is a misperception that if a company’s PBR is above 1, it is not necessary to meet the request to “take action to implement management that is conscious of cost of capital and stock price”.2

This focus on the PBR appears somewhat misunderstood because the desired outcome is to drive growth and higher valuations in the Japanese market, and therefore requires the consideration of a broader range of financial measures. Companies should decide and concentrate on what is relevant to their business. For example, the TSE has highlighted the PBR, return on invested capital (ROIC), weighted average cost of capital (WACC) and return on equity (ROE) as relevant measures. At Newton, we use PBR1 not as an end goal, but as a starting point for analysis. Furthermore, our investment team compares the ROE and ROIC across companies, in addition to reviewing the action plans the companies have disclosed to improve these measures. Finally, the TSE is targeting all companies and not just those with a PBR below 1 or with lower capital efficiency. Over time, there has been an increase in companies with a PBR of greater than 1 disclosing their plans, suggesting that this misunderstanding is gradually being resolved in Japan.

How effective have the reforms been?

The changes have been somewhat effective in driving up the volume of disclosures (at around 60% for the Prime market), but the quality of disclosures generally leaves much room for improvement, in our view. It appears that many companies have rushed into disclosing their plans to improve their capital efficiency without first having taken the time to analyse their business. A company may have a low valuation for a number of reasons, and it is good business practice for the management and the board to identify the reasons for the low valuation before pushing forward a solution. There is an open question as to whether companies, in particular smaller companies, currently have the appetite or the resource to perform this analysis thoroughly.

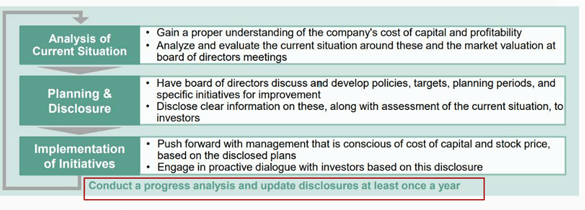

Actions required to achieve management that is conscious of cost of capital and stock price

Source: Japan Exchange Group, Inc., 2024.3

Moreover, when implementing any changes, there is a balance to be struck between applying pressure on companies and avoiding a sharp response. Effectiveness often comes down to enforcement. In this instance, investors holding companies to account will be key. We believe that the success of these reforms will, in large part, be determined by how rigorously investors, both Japanese and global, assess the disclosures that the companies make and what details the investors demand of the investee companies. For example, if investors ask questions about the robustness of companies’ plans to increase their book value, it may encourage investee companies to be thorough in their assessment of their own business.

Not just a box-ticking exercise

While the TSE and regulator are placing increasing emphasis on efforts like disclosure reforms, in our opinion it is not a simple fix to address what we perceive to be a market discount. There is a risk that these reforms end up being a box-ticking exercise instead of having the intended effects. A significant structural change in company valuations will require incremental but widespread change, and we expect this to be slow moving and to require persistent efforts over the longer term. Disclosure alone will not be sufficient to change valuations; companies will have to appropriately assess the reasons for current valuation levels. In addition, isolated regulatory disclosures will be insufficient. Management and investor relations teams must be able to consistently articulate the ways in which they are responding to such reforms during investor outreach and in written materials. The use of dividends and buy-backs may affect valuations in the short term, but long-term investors will be assessing the cost of capital, restructuring and investments to enable future growth.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Sources:

- Publication of Revised Japan’s Corporate Governance Code, Japan Exchange Group, 11 June 2021: https://www.jpx.co.jp/english/news/1020/20210611-01.html

- TSE to Publish a List of Companies That Have Disclosed Information Regarding “Action to Implement Management That Is Conscious of Cost of Capital and Stock Price”, Japan Exchange Group, 26 October 2023: https://www.jpx.co.jp/english/equities/follow-up/uorii50000004sse-att/o4sio70000000mi4.pdf

- Reminder Regarding the Criteria for Inclusion in the List of Companies That Have Disclosed Information Regarding “Action to Implement Management That Is Conscious of Cost of Capital and Stock Price”, Japan Exchange Group, 29 March 2024: https://www.jpx.co.jp/english/equities/follow-up/uorii50000004sse-att/dh3otn0000004cnc.pdf

Key Points

- The Tokyo Stock Exchange made updates to its listing requirements last year, and as a result, there has been an increased impetus for investors to hold companies to account.

- Improved disclosure by companies can be useful for investors to identify opportunities, and combining this with focused dialogue can help in understanding the full picture of an investment opportunity.

- We believe that for the reforms to achieve the desired aims, a cultural change across corporate Japan is needed, which will be slow and require persistent efforts over the longer term.

Holding Companies to Account

In 2023, The Tokyo Stock Exchange (TSE) made updates to its listing requirements, tightening its listing criteria, encouraging companies to disclose plans to increase their capital efficiency, and announcing stricter rules around diversity, disclosure and sustainability. We discussed what these updates mean for investors in our blog Japan: Investment Implications of Corporate Governance Reforms.

A key implication of the reform is the additional impetus for investors to hold companies to account, both for their disclosures and the quality of their plans. We expect that for the initiatives to be most effective, investors will have to act as enforcers by providing additional incentive to meet the spirit of the requirements. Without such incentives, there is the possibility that companies respond with low-quality disclosures which are merely ‘box-ticking’ in nature, or with a plan lacking in credibility, with no repercussions.

Understanding the Full Picture

Improved access to information about a company’s capital management is helpful for active investors when analyzing opportunities. An ambitious plan with poor credibility, for which there is little faith that the management will be able to execute, could present an opportunity if investors were instead to believe in it. Dialogue with management can add valuable qualitative data points concerning the management’s actual priorities, thereby adding to investors’ confidence in the plan or otherwise. Ultimately, we see great value in combining disclosures with direct interaction with companies to understand the full picture.

Engagement Opportunities

Insights gained from company dialogue may also present opportunities to invest in companies in which investor confidence does not yet fully exist, or where its potential is not priced in by the market but we believe there to be a reasonable prospect of increasing conviction. A number of elements could improve investors’ confidence in a company: proposed changes to the company’s plan, enhancing its credibility; successful execution of the plan; or even improved transparency of the plan to the market, enabling the plan and potential investment implications to be fully recognized.

In cases where investors believe changes need to go further, they may turn to engagement. Engagement at Newton centers on the purposeful dialogue that we can have with issuers to reduce risk and potentially add value to an investment. We set clear outcome-focused objectives for each engagement, tailored to the specific action the issuer can take to address the matter of concern, which can be evaluated over a suitable time horizon and can be linked back to a relevant investment thesis.[1] For this reason, capital allocation, as part of corporate governance and business strategy, is a topic that we tend to focus on when engaging with companies in Japan.

Engagement in Action

We engaged with a small-cap Japanese company which provides labor dispatching services such as outsourcing of permanent employees in manufacturing, design and development, construction, and other sectors across Japan. After analyzing its reporting, we considered disclosures to be insufficient, and consequently, there was an opportunity for the company to improve them and receive market recognition. This is frequently the case for smaller companies, which often have fewer resources to dedicate to reporting and market transparency, whether that be in relation to financial measures and/or sustainability. Specifically, we considered the following areas to be light on information: its required investments to achieve the mid-term plan, its expected cash flows, its target balance sheet, and its capital distribution plan. Having met the company, including external directors, we shared our view that improving these disclosures on the financial/capital allocation plan is important.

Positively, in the updated mid-term plan, the company had enhanced the disclosure of its financial and capital allocation plan. In addition, it amended the policy for the payout to shareholders, increasing the payout ratio. The market value of this company rose by more than 30%, which we consider to be in part owing to the increase in payout to shareholders. We expect to continue this dialogue with the company, and will monitor it to ensure that the capital allocation plan is both communicated and carried out successfully.

Meaningful Dialogue

This is another interesting period for the Japanese market, and many stakeholders appear to be keeping a keen eye on the impacts of the TSE’s latest initiatives and company responses. Even though there is considerable support and strong drivers behind the reforms, there is a risk that this does not move past a box-ticking exercise and does not deliver the intended effects. We believe that to achieve the desired aims, a cultural change across corporate Japan is needed, which will be slow and require persistent efforts over the longer term. However, the achievement of this could present mutual benefits for numerous stakeholders, including investors, their clients, companies and management. Meaningful dialogue between investors and investee companies, focused on financially material enhancements, within the context of the business model and culture, could begin to unlock such benefits.

However, even assuming a rising tide, we do not believe that the reforms will lift all boats. We believe that investors that can conduct meaningful analysis and dialogue with companies will be better able to identify investment opportunities. It will be imperative to understand businesses, the credibility and relevance of the capital allocation and financial plan, management’s ability to execute its plans, and their capacity to communicate effectively with the market. Investors can combine this understanding with targeted engagement to encourage improvements, where such improvements are likely to unlock value for all stakeholders. A local-market understanding of culture, language and context may support investors in doing so most effectively.

[1] View Our Approach to Engagement to learn more: https://newtonim.com/responsibleinvestment