Key points

- Market shifts and geopolitical tensions have highlighted idiosyncratic and macroeconomic risks. We believe investors can benefit by adopting nimble and dynamic strategies, harnessing liquid and diversifying approaches to seek to capture varied sources of alpha and protect against market volatility.

- Examples include convex/divergent approaches like tail-risk protection, which contains components to address drawdowns, and systematic strategies that are valued for their uncorrelated returns versus traditional assets.

- Collaboration between clients, asset managers and/or advisers is essential to create a structure that meets the client’s goals.

Few would argue with the thesis that the market regime has changed markedly from the days of ultra-low interest rates, further fueled by waves of quantitative easing that lifted all boats. The Covid-19 pandemic led to an increase in volatility, less price stability and inflation moving structurally higher. Moreover, the traditional negative correlation between bonds and equities has broken down over the last few years, creating a need to update the investment toolkit, diversifying away from equity and bond beta to create a more resilient return stream.

Today’s market backdrop presents a number of risks, many of which are structural in nature as a result of the end to the ‘easy money’ era, and there will be a need to have a keen awareness of considerations such as liquidity, valuation and concentration risks.

Navigating Risks and Opportunities in a Changing Global Landscape

Recent developments in artificial intelligence, where on a number of occasions in recent months we witnessed leading stocks lose a significant portion of their value, have placed the spotlight on idiosyncratic risk. The US equity market is highly concentrated, and this can cause havoc when elevated expectations start to unravel. However, it represents fertile ground for discerning investors as risk also represents opportunity.

The macroeconomic risk inherent in the backdrop challenges those structures and businesses unaccustomed to operating in a high-interest-rate environment. There is a need to distinguish the winners from the losers: more fragile companies are likely to struggle, while nimble, creditworthy entities should thrive. This applies across the asset-class spectrum, from equities to fixed income to alternatives, and managers need to possess skill to pick the correct drivers.

Another observable shift is the formation of spheres of influence in the world, evidenced by the geopolitical tensions which have become increasingly visible with tangible consequences, notably the outbreak of war in the Middle East and the Russia/Ukraine conflict. A changing world order will have major implications for capital and how we choose to invest. Indeed, it can be viewed as the reshaping of the capital system which, while daunting when viewed through one lens, can also be viewed as an opportunity for growth and innovation.

Optimizing Portfolios with Liquid and Diversifying Approaches

These forces should represent an environment in which strategies that are both liquid and diversifying can be invaluable. Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha. Currency will also be an important factor; a weakening of the US dollar, for example, could have global repercussions and misalignment can create opportunities.

Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha.

In this context, how should investors implement such strategies and what are the barriers they face?

One important consideration is that investors have the choice to adopt either a fully outsourced solution or a more modular approach where they can select the strategies that complement their existing needs. Positioning different strategies to distinguish between their functions within a total portfolio context can be helpful, with the key metric being what these exposures bring to the table. There is often an alphabet soup of names to navigate and a complexity hurdle to overcome, so providing a clear framework is key.

The hedge fund researchers at Bfinance have structured the liquid alternatives universe into three main buckets:1

- The first of these includes convex/divergent approaches, such as tail-risk hedging strategies and diversified commodity trading advisor strategies. These have the potential to thrive in turbulent regimes and provide ‘heroic diversification.’

- The second bucket is comprised of market-independent strategies, such as equity market-neutral and relative-value systematic macro strategies. These can exhibit returns independent of the market environment, with an ability to generate uncorrelated return streams.

- Finally, the third bucket incorporates directional strategies such as equity long/short (with a long bias), dynamic beta or absolute-return strategies. These are more akin to traditional risk assets, seeking to deliver alpha through an unconstrained investment approach.

Distinct Approaches That Harness Manager Skill

Given the likelihood of persistent macroeconomic and geopolitical uncertainty leading to a greater dispersion of returns, we believe the current environment is likely to be positive for the introduction of carefully assembled strategies that are both liquid and diversifying, with each component exhibiting a distinct risk/return profile. The existence of manager skill is a prerequisite, as investors are unlikely to continue to be able to ride the wave of multi-decade, beta-driven rallies.

An example of a convex/divergent approach that should be suited to the new regime is tail-risk protection. This contains components to address both sharp and sustained drawdowns and can embed a funding element to minimize cost; indeed, the cost of such insurance is funded within the strategy itself. Investors can combine this approach with an equity allocation to help cushion the return stream in times of market turbulence.

In contrast, systematic strategies that are valued for their uncorrelated returns versus traditional assets have a different role to play. Their market-neutral design isolates alpha streams, derived from a range of sources including currency, equity, bonds and commodities, and works with the higher cash rate rather than fighting against it. It is also possible to blend systematic and discretionary approaches, each providing complementary return streams and with the potential for different time horizons.

Client-Centric Strategy Design

As with all successful strategy designs, there is no need for jargon-ridden labels: the focus should be on client needs and a structure that makes sense, given investment objectives, risk tolerance and other client-specific considerations. Education and understanding are paramount, and it is incumbent on the client, asset manager and/or adviser to work together in close partnership. Considering the utility of each component is also important and this will inform position sizing.

There is no need for jargon-ridden labels: the focus should be on client needs and a structure that makes sense, given investment objectives, risk tolerance and other client-specific considerations.

Finally, fees are another factor in the mix: many hedge-fund incumbents are currently price setters; however, new entrants are disrupting this space, and a pragmatic evaluation of net-of-fee returns and Sharpe ratios is critical in this evolving domain.

Resilient Portfolio Strategies

The ultimate aim for investors is to build a resilient portfolio, hence the need to establish clear classifications for strategies in this space in order to gain a fuller understanding of their utility from a total portfolio perspective. We encourage investors to consider this rapidly evolving domain with a fresh perspective. It is important to recognize that there is no ‘one-size-fits-all’ solution, and establishing a partnership with an asset manager that possesses the requisite expertise may be beneficial in achieving these objectives.

1 Forget Hedge Fund Strategy Labels – Here Are Three Groups that Matter, Bfinance, November 5, 2024

Key points

- The current macroeconomic and geopolitical environment favours the introduction of liquid and diversifying strategies, each with a distinct risk/return profile, to build resilient portfolios.

- Examples include convex/divergent approaches like tail-risk protection, which contains components to address drawdowns, and systematic strategies that are valued for their uncorrelated returns versus traditional assets.

- Collaboration between clients, asset managers and/or advisers is essential to create a structure that meets the client’s goals.

We have previously talked about a decade of disturbance and the scope for divergence in investment performance at a geographic, sector and asset-class level. This begs the question: is it possible to find strategies that offer not just attractive risk-adjusted returns, but also diversification within them? Furthermore, how should investors implement such strategies and what are the barriers they face?

One important consideration is that investors have the choice to adopt either a fully outsourced solution or a more modular approach where they can select the strategies that complement their existing needs. Positioning different strategies to distinguish between their functions within a total portfolio context can be helpful, with the key metric being what these exposures bring to the table. There is often an alphabet soup of names to navigate and a complexity hurdle to overcome, so providing a clear framework is key.

The hedge fund researchers at Bfinance have structured the liquid alternatives universe into three main buckets:1

- The first of these includes convex/divergent approaches, such as tail-risk hedging strategies and diversified commodity trading advisor strategies. These have the potential to thrive in turbulent regimes and provide ‘heroic diversification’.

- The second bucket is comprised of market-independent strategies, such as equity market-neutral and relative-value systematic macro strategies. These can exhibit returns independent of the market environment, with an ability to generate uncorrelated return streams.

- Finally, the third bucket incorporates directional strategies such as equity long/short (with a long bias), dynamic beta or absolute-return strategies. These are more akin to traditional risk assets, seeking to deliver alpha through an unconstrained investment approach.

Distinct approaches that harness manager skill

Given the likelihood of persistent macroeconomic and geopolitical uncertainty leading to a greater dispersion of returns, we believe the current environment is likely to be positive for the introduction of carefully assembled strategies that are both liquid and diversifying, with each component exhibiting a distinct risk/return profile. The existence of manager skill is a prerequisite, as investors are unlikely to continue to be able to ride the wave of multi-decade, beta-driven rallies.

An example of a convex/divergent approach that should be suited to the new regime is tail-risk protection. This contains components to address both sharp and sustained drawdowns and can embed a funding element to minimise cost; indeed, the cost of such insurance is funded within the strategy itself. Investors can combine this approach with an equity allocation to help cushion the return stream in times of market turbulence.

In contrast, systematic strategies that are valued for their uncorrelated returns versus traditional assets have a different role to play. Their market-neutral design isolates alpha streams, derived from a range of sources including currency, equity, bonds and commodities, and works with the higher cash rate rather than fighting against it. It is also possible to blend systematic and discretionary approaches, each providing complementary return streams and with the potential for different time horizons.

Client-centric strategy design

As with all successful strategy designs, there is no need for jargon-ridden labels: the focus should be on client needs and a structure that makes sense, given investment objectives, risk tolerance and other client-specific considerations. Education and understanding are paramount, and it is incumbent on the client, asset manager and/or adviser to work together in close partnership. Considering the utility of each component is also important and this will inform position sizing.

There is no need for jargon-ridden labels: the focus should be on client needs and a structure that makes sense, given investment objectives, risk tolerance and other client-specific considerations.

Finally, fees are another factor in the mix: many hedge-fund incumbents are currently price setters; however, new entrants are disrupting this space, and a pragmatic evaluation of net-of-fee returns and Sharpe ratios is critical in this evolving domain.

Resilient portfolio strategies

The ultimate aim for investors is to build a resilient portfolio, hence the need to establish clear classifications for strategies in this space in order to gain a fuller understanding of their utility from a total portfolio perspective. We encourage investors to consider this rapidly evolving domain with a fresh perspective. It is important to recognise that there is no ‘one-size-fits-all’ solution, and establishing a partnership with an asset manager that possesses the requisite expertise may be beneficial in achieving these objectives.

1 Forget Hedge Fund Strategy Labels – Here Are Three Groups that Matter, Bfinance, 5 November 2024

Key points

- Geopolitical tensions and changing market dynamics are creating opportunities and challenges for investors.

- We believe investors can benefit by adopting strategies that offer liquidity and diversification to seek to capture varied sources of return and to protect themselves against market volatility.

- Investment managers can use their experience and skill to convert risks into opportunities, using a keen awareness of secular trends to optimise future returns.

Few would argue that the market regime has changed markedly from the days of ultra-low interest rates, further fuelled by waves of quantitative easing1 that lifted all boats. The Covid-19 pandemic led to an increase in volatility, less price stability and inflation moving structurally higher. Moreover, the traditional negative correlation between bonds and equities has broken down over the last few years, creating a need to update the investment toolkit, diversifying away from traditional equity and bond exposure to create a more resilient return stream.

Today’s market backdrop presents a number of risks, many of which are structural in nature as a result of the end to the ‘easy money’ era, and there will be a need to have a keen awareness of considerations such as ready liquidity, market and individual stock valuations, and concentration risks.

Navigating risks and opportunities in a changing global landscape

Recent developments in artificial intelligence, where on a number of occasions in recent months we witnessed the posterchild Nvidia lose a significant portion of its value, sometimes in a single day,2 have placed the spotlight on idiosyncratic risk. The US equity market now represents over 65% of the world index, and the largest ten companies now account for 23% of this.3 This level of concentration could cause havoc should elevated expectations start to unravel. However, this represents fertile ground for discerning investors as the level of implied risk also represents opportunity.

The macroeconomic risk inherent in the backdrop challenges those structures and businesses unaccustomed to operating in a higher interest-rate environment. There is a need to distinguish the potential winners from the losers: more fragile companies are likely to struggle, while nimble, creditworthy entities should thrive. This applies across the asset-class spectrum, from equities to fixed income to alternatives, and managers need to possess skill to select the best outcomes.

Another observable shift is the formation of spheres of influence in the world, evidenced by the geopolitical tensions which have become increasingly visible with tangible consequences, notably the outbreak of war in the Middle East and the Russia/Ukraine conflict. The return of President Trump to the White House adds an additional source of uncertainty as world leaders wrestle for control of a broad agenda. A changing world order will have major implications for capital and how we choose to invest. Indeed, it can be viewed as the reshaping of the capital system which, while daunting when viewed through one lens, can also be viewed as an opportunity for growth and innovation.

Harnessing liquid and diversifying strategies in a volatile market

These forces should represent an environment in which strategies that are both liquid and diversifying can be invaluable. Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of return. Currency will also be an important factor; a weakening of the US dollar, for example, could have global repercussions and misalignment can create opportunities.

Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of return.

Moreover, approaches such as relative-value strategies (which seek to take advantage of price differentials between related financial instruments) can benefit from greater dispersion and market volatility and have the potential to perform well in this environment. Likewise, tail-risk hedging approaches (strategies seeking to mitigate exposure to downside risk), which acknowledge the shortcomings of traditional multi-asset diversifiers such as fixed income, may provide a more reliable form of protection in the context of a more skittish, volatile backdrop.

Collaboration for success

In summary, the opportunity set is rich. We think that both we and our clients need to adapt to the new normal and adopt strategies that are liquid and diversifying, and which can navigate less predictable market scenarios. This may require some investors to increase their appetite for complexity, sharpen their research (these are skill-based investments) and overcome biases from the previous decade. We anticipate that better performance from liquid alternative diversifiers over the last few years may help investors make the leap.

Investors do not need to do it all on their own. If asset owners and asset managers like ourselves partner together, we believe there is a greater likelihood that market risks can be converted into opportunities for optimising future returns.

1 Quantitative easing is a monetary policy whereby central banks buy predetermined amounts of government bonds or other financial assets in order to stimulate the economy and increase liquidity.

2 Source: DeepSeek sparks AI stock selloff; Nvidia posts record market-cap loss, Reuters, 28 January 2025

3 Source: MSCI ACWI Index – Factsheet, 31 January 2025

Glossary

Visit our knowledge centre for a glossary of common investment terms and to learn more about key investment concepts.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Key points

- Market shifts and geopolitical tensions have highlighted idiosyncratic and macroeconomic risks, creating both challenges and opportunities for investors.

- We believe investors can benefit by adopting nimble and dynamic strategies, harnessing liquid and diversifying approaches to seek to capture varied sources of alpha and protect against market volatility.

- Asset owners and managers can partner to convert risks into opportunities, using skill-based investments and a keen awareness of secular trends to optimise future returns.

Few would argue with the thesis that the market regime has changed markedly from the days of ultra-low interest rates, further fuelled by waves of quantitative easing that lifted all boats. The Covid-19 pandemic led to an increase in volatility, less price stability and inflation moving structurally higher. Moreover, the traditional negative correlation between bonds and equities has broken down over the last few years, creating a need to update the investment toolkit, diversifying away from equity and bond beta to create a more resilient return stream.

Today’s market backdrop presents a number of risks, many of which are structural in nature as a result of the end to the ‘easy money’ era, and there will be a need to have a keen awareness of considerations such as liquidity, valuation and concentration risks.

Navigating risks and opportunities in a changing global landscape

Recent developments in artificial intelligence, where we witnessed the posterchild Nvidia lose a significant portion of its value in a single day in a five-sigma event,1 have placed the spotlight on idiosyncratic risk. The US equity market is highly concentrated, and this can cause havoc when elevated expectations start to unravel. However, it represents fertile ground for discerning investors as risk also represents opportunity.

The macroeconomic risk inherent in the backdrop challenges those structures and businesses unaccustomed to operating in a high-interest-rate environment. There is a need to distinguish the winners from the losers: more fragile companies are likely to struggle, while nimble, creditworthy entities should thrive. This applies across the asset-class spectrum, from equities to fixed income to alternatives, and managers need to possess skill to pick the correct drivers.

Another observable shift is the formation of spheres of influence in the world, evidenced by the geopolitical tensions which have become increasingly visible with tangible consequences, notably the outbreak of war in the Middle East and the Russia/Ukraine conflict. A changing world order will have major implications for capital and how we choose to invest. Indeed, it can be viewed as the reshaping of the capital system which, while daunting when viewed through one lens, can also be viewed as an opportunity for growth and innovation.

Harnessing liquid and diversifying strategies in a volatile market

These forces should represent an environment in which strategies that are both liquid and diversifying can be invaluable. Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha. Currency will also be an important factor; a weakening of the US dollar, for example, could have global repercussions and misalignment can create opportunities.

Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha.

Moreover, approaches such as relative-value strategies, which benefit from greater dispersion and market volatility, have the potential to perform well in this environment. Likewise, tail-risk hedging approaches, which acknowledge the shortcomings of traditional multi-asset diversifiers such as fixed-income market beta, may provide a more reliable form of protection in the context of a more skittish, volatile backdrop.

Collaboration for success

In summary, the opportunity set is rich. We think that both clients and asset managers need to adapt to the new normal and harness strategies that are liquid and diversifying, and which can pull their weight in less predictable market scenarios. This may require some investors to increase their appetite for complexity, sharpen their research (these are skill-based investments) and overcome biases from the previous decade. We anticipate that better performance from liquid alternative diversifiers over the last few years may help investors make the leap.

Investors do not need to do it all on their own. If asset owners and asset managers partner together, we believe there is a greater likelihood that risks can be converted into opportunities, and establishing perspective on secular trends and themes can provide a roadmap for optimising future returns.

1 DeepSeek sparks AI stock selloff; Nvidia posts record market-cap loss, Reuters, 28 January 2025

Key points

- Market shifts and geopolitical tensions have highlighted idiosyncratic and macroeconomic risks, creating both challenges and opportunities for investors.

- We believe investors can benefit by adopting nimble and dynamic strategies, harnessing liquid and diversifying approaches to seek to capture varied sources of alpha and protect against market volatility.

- Asset owners and managers can partner to convert risks into opportunities, using skill-based investments and a keen awareness of secular trends to optimise future returns.

Few would argue with the thesis that the market regime has changed markedly from the days of ultra-low interest rates, further fuelled by waves of quantitative easing that lifted all boats. The Covid-19 pandemic led to an increase in volatility, less price stability and inflation moving structurally higher. Moreover, the traditional negative correlation between bonds and equities has broken down over the last few years, creating a need to update the investment toolkit, diversifying away from equity and bond beta to create a more resilient return stream.

Today’s market backdrop presents a number of risks, many of which are structural in nature as a result of the end to the ‘easy money’ era, and there will be a need to have a keen awareness of considerations such as liquidity, valuation and concentration risks.

Navigating risks and opportunities in a changing global landscape

Recent developments in artificial intelligence, where we witnessed the posterchild Nvidia lose a significant portion of its value in a single day in a five-sigma event,1 have placed the spotlight on idiosyncratic risk. The US equity market is highly concentrated, and this can cause havoc when elevated expectations start to unravel. However, it represents fertile ground for discerning investors as risk also represents opportunity.

The macroeconomic risk inherent in the backdrop challenges those structures and businesses unaccustomed to operating in a high-interest-rate environment. There is a need to distinguish the winners from the losers: more fragile companies are likely to struggle, while nimble, creditworthy entities should thrive. This applies across the asset-class spectrum, from equities to fixed income to alternatives, and managers need to possess skill to pick the correct drivers.

Another observable shift is the formation of spheres of influence in the world, evidenced by the geopolitical tensions which have become increasingly visible with tangible consequences, notably the outbreak of war in the Middle East and the Russia/Ukraine conflict. A changing world order will have major implications for capital and how we choose to invest. Indeed, it can be viewed as the reshaping of the capital system which, while daunting when viewed through one lens, can also be viewed as an opportunity for growth and innovation.

Harnessing liquid and diversifying strategies in a volatile market

These forces should represent an environment in which strategies that are both liquid and diversifying can be invaluable. Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha. Currency will also be an important factor; a weakening of the US dollar, for example, could have global repercussions and misalignment can create opportunities.

Rather than adopting a ‘buy and hold’ approach, we think there will be a need to be nimble and dynamic, using as wide a toolkit as possible to seek to capture diversified sources of alpha.

Moreover, approaches such as relative-value strategies, which benefit from greater dispersion and market volatility, have the potential to perform well in this environment. Likewise, tail-risk hedging approaches, which acknowledge the shortcomings of traditional multi-asset diversifiers such as fixed-income market beta, may provide a more reliable form of protection in the context of a more skittish, volatile backdrop.

Collaboration for success

In summary, the opportunity set is rich. We think that both clients and asset managers need to adapt to the new normal and harness strategies that are liquid and diversifying, and which can pull their weight in less predictable market scenarios. This may require some investors to increase their appetite for complexity, sharpen their research (these are skill-based investments) and overcome biases from the previous decade. We anticipate that better performance from liquid alternative diversifiers over the last few years may help investors make the leap.

Investors do not need to do it all on their own. If asset owners and asset managers partner together, we believe there is a greater likelihood that risks can be converted into opportunities, and establishing perspective on secular trends and themes can provide a roadmap for optimising future returns.

1 DeepSeek sparks AI stock selloff; Nvidia posts record market-cap loss, Reuters, 28 January 2025

Key points

- We believe relative-value strategies are well placed to exploit the current conditions of greater dispersion and heightened volatility.

- US earnings continue to grow but the gap between valuation and earnings has increased.

- There is still room for the US economy to expand, if the new Trump administration can quickly implement its growth initiatives, or contract if it enacts policies that impede growth.

Relative value versus directional alpha

The discount rate is one of the most important metrics in the evaluation of financial assets. Current short-term interest rates are a proxy for the discount rate that is used to determine the net present value of all the future cash flows associated with a financial asset.

The change in cash rates and the discount rate, which began in the aftermath of the Covid pandemic when policy rates began to move higher, signalled the transition from a directional market regime to a relative-value market regime. In our view, this has significant consequences for investors. For example, in a directional regime when the market is in an upward or downward trend, buy and hold equity strategies have typically thrived. On the other hand, a relative-value environment may require a more tactical view across an investment universe that also includes a fair amount of dispersion.

We expect 2025 to continue to favour relative-value alpha strategies that seek to generate a return that is uncorrelated with the broader market, while buy-and-hold directional strategies are likely to face challenges and relatively low premiums. Strategies that utilise relative value have shown increased effectiveness due to dispersion across monetary and policy rates, fiscal tightening, growth rates, inflation rates and returns—not only in equities and bonds but also across currencies and commodities.

Key takeaway: Embrace the macro dislocations and uncertainty as opportunities to generate alpha.

US inflation

Due to the large Covid-era stimulus, the US experienced unprecedented inflation, which peaked at 9%. Conveniently, the Federal Open Market Committee (FOMC) redefined its inflation target as Flexible Average Inflation Targeting (FAIT), where an average of 2% could be commensurate with a current level of 2.5% (core personal consumption expenditures inflation). Unfortunately for the FOMC and the new US administration, historically it has been the rule, rather than the exception, that inflation jumps or reaccelerates before it settles at levels closer to 2.5%.

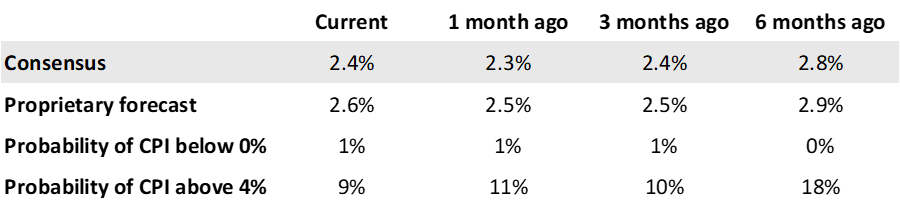

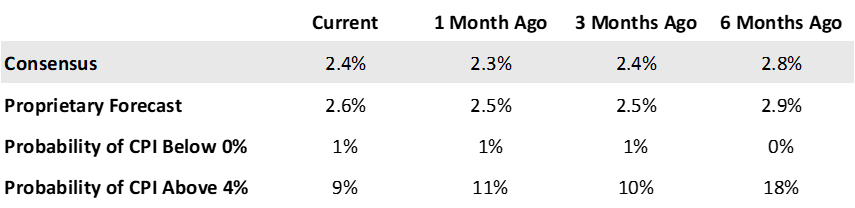

We believe there could be a slight increase in the US consumer price index (CPI) to 2.6% relative to the consensus forecast of 2.4% over the next 12 months. More worryingly, the Cleveland Federal Reserve’s nowcasting model forecasts the December 2024 CPI to be 0.38%, equivalent to 4.5% on an annualised basis.1 Its year-over-year inflation forecasts are all around 3%.

Forecasted 12-month change in US headline CPI

Key takeaway: Do not ignore risk of inflation running hot before it settles at 2%.

Currencies: US dollar and Japanese yen

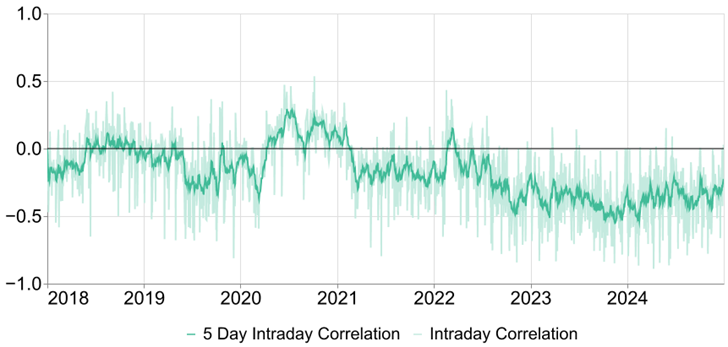

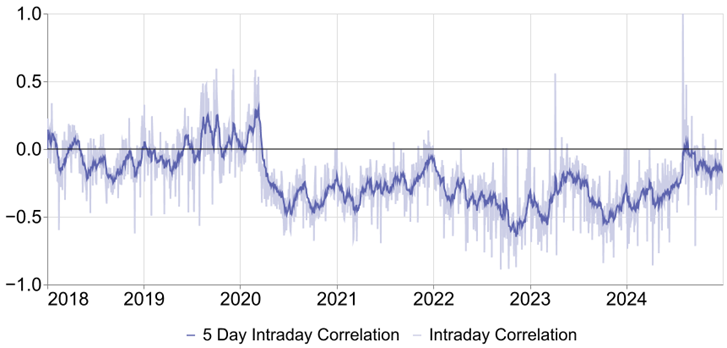

The value of the US dollar as represented by the US Dollar Index has rallied 9.5% since October 2024. This has quickly become one of the more crowded trades as both systematic and discretionary strategies latch onto this clear trend. However, a strong, or in this case over-valued, US dollar relative to the Japanese yen and Chinese renminbi does not suit the long-term policy goals of the new US Trump administration. To facilitate ‘friend shoring’ and improved competitiveness for US manufacturers, the dollar needs to move in the other direction.

In the meantime, the US dollar provides a useful and rare negative correlation to bonds and equities. We believe other currencies such as the yen could balance this trend, perhaps making it the anti-fragile currency for 2025

US 10-year Treasury note vs. US Dollar Index

S&P 500 vs. US Dollar Index

Key takeaway: Enjoy the US dollar ride while it lasts; look for other currencies such as the Japanese yen to balance exposure.

US equity earnings

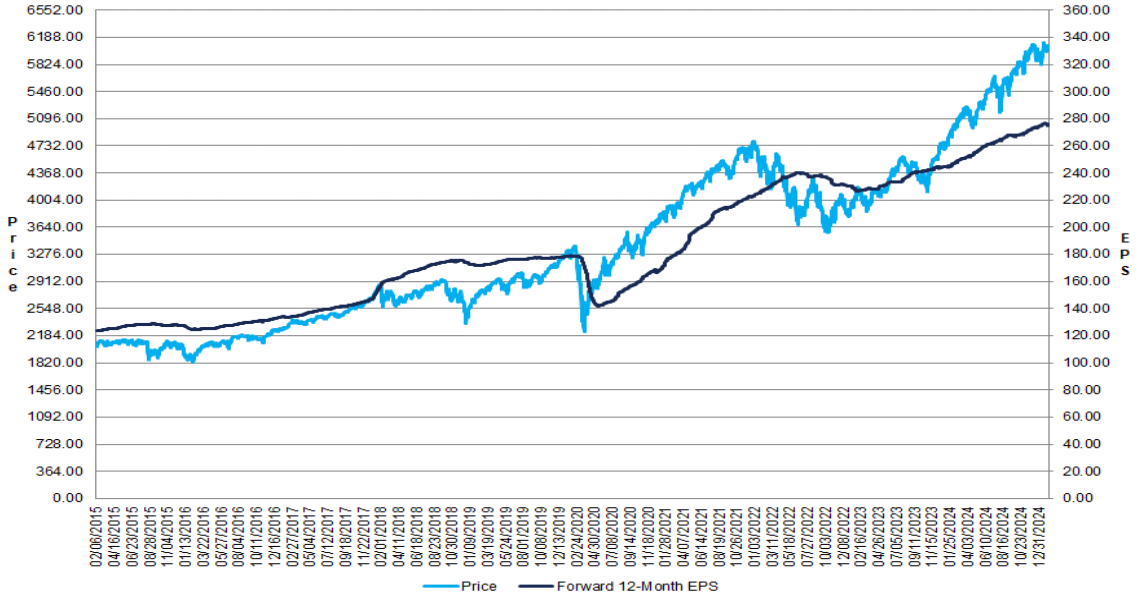

Thus far, US equity earnings in 2024 have not disappointed, with full-year earnings-per-share (EPS) growth expected to be 11.7%, the highest since the post-Covid recovery in 2021. We expect S&P 500® EPS to fall short of expectations yet still provide healthy growth with little chance of a contraction. Over the next 12 months, the S&P 500 EPS consensus forecast is 12.1%, while our proprietary forecast is 6.6%, or approximately one half that of the consensus. Fundamental analysts tend to be an optimistic bunch who start the calendar year with high expectations but then walk back their outlook as each quarter’s earnings become clearer.

Despite positive EPS growth, the value of the S&P 500 has run ahead of the bottom-up earnings since 2023.2 This is the same period when EPS grew a meagre 2% in nominal terms against the total return of 26.3% and inflation of 6.5%. In fact, the gap between valuation and earnings has increased due to the boost related to artificial intelligence (AI), a productivity tool which is as yet difficult to quantify.

S&P 500: Change in forward 12-Month EPS vs. change in price

Key takeaway: US earnings continue to grow but the gap between valuation and earnings has increased.

US bond rollercoaster

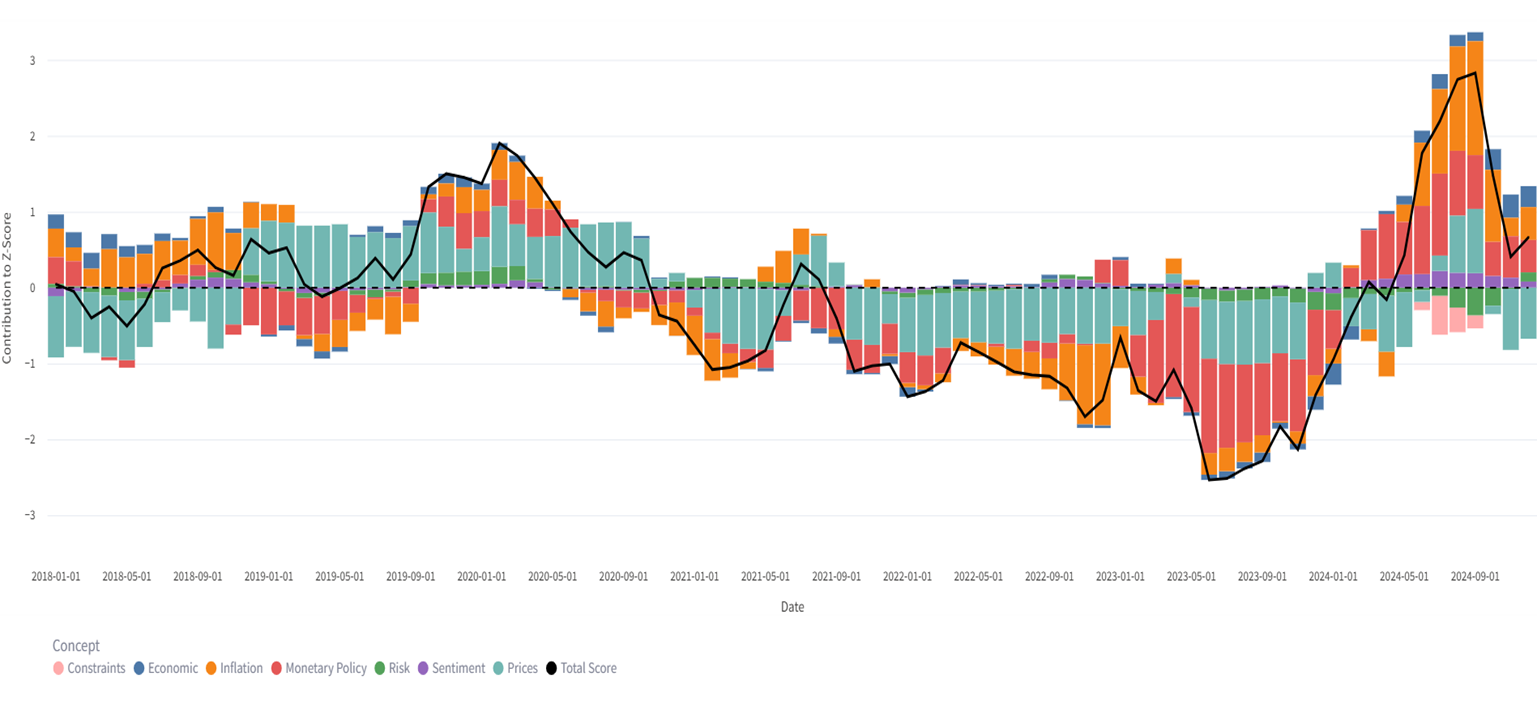

One of the most difficult directional views since the pandemic has been US bonds as well as sovereign bonds in general. During the past four calendar years (2021-2024), US Treasuries have delivered very little return (cumulative return of -10%3), and very little diversification, with correlations to equities shifting positive. In 2024, US 10-year Treasury yields ranged from 3.6% to 4.7%, with at least two V-shaped cycles over the year.

The below chart illustrates our tactical bond signal which is meant to complement the longer-term carry and term premium. It has reflected the bond rollercoaster and importantly its various turning points.

Monthly bond macro signal attribution by concept: January 2018 – December 2024

Key takeaway: Net long or short bond positions require relative nimbleness in mind as well as exposure.

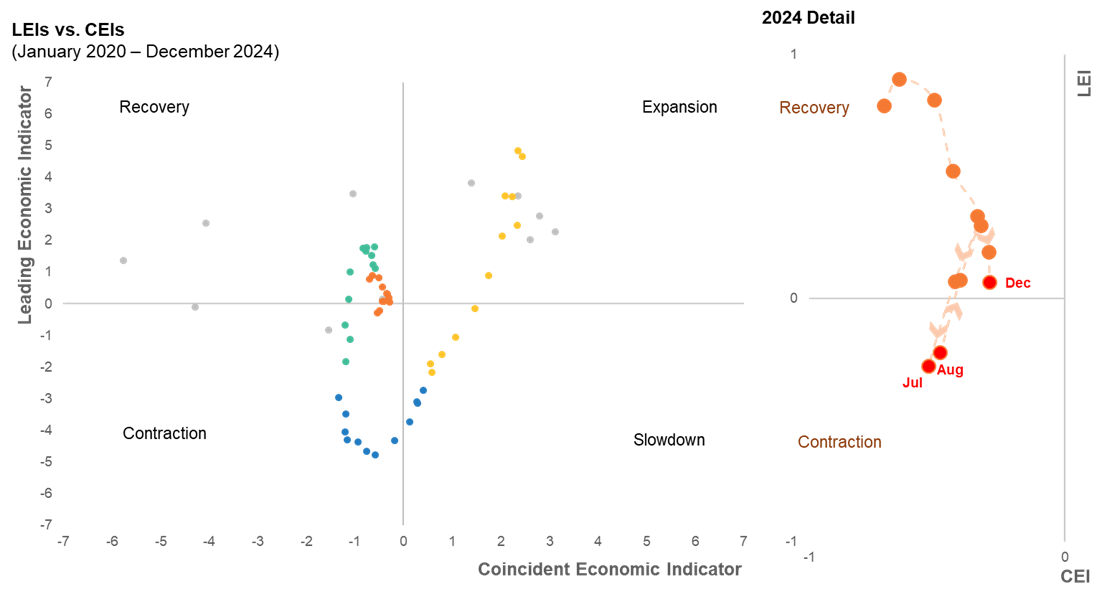

US economic cycle

Prior to the active stimulus to combat the effects of the Covid lockdowns and large-scale unemployment, the US economic cycle was relatively well behaved for ten years. Given the aggressive policy intervention and very high fiscal stimulus deployed, the US has experienced four phases of the economic cycle in a very short four years.

The below illustrates this journey based on our proprietary leading economic indicators (LEIs) and coincident economic indicators (CEIs). Currently, the US economy is in neither contraction nor recovery, in other words the ‘no landing’ scenario. There is still room for the US economy to expand if the new Trump administration can quickly implement its growth initiatives, such as deregulation and budget cuts. Alternatively, the economy could contract if policies that impede growth, such as tariffs and unfunded tax cuts, prevail.

US flexcasting indicators

Key takeaway: As of yet, the “no landing” scenario for the US economy is most likely; consequently, it could expand into a recovery or descend into a contraction. No bets are off.

1 Source: Federal Reserve Bank of Cleveland https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting, accessed on 14 Jan 2025.

2 Source: Factset https://www.factset.com/earningsinsight, as of January 10, 2025.

3 Source: JPMorgan US Treasury Index.

Key points

- As well as being an area of concern for charities, inflation forecasting is key to enable them to project grant giving, withdrawal rates and spending needs.

- While some structural trends remain disinflationary, particularly technological disruption and the integration of artificial intelligence, other trends such as deglobalisation have reversed.

- Provided that the Bank of England sticks to its inflation-targeting regime, it is likely to hold rates higher for longer to bring inflation down and combat the forces of ‘sticky’ inflation.

The 2024 Newton Charity Investment Survey revealed that, despite concern about inflation having declined, inflation remains a unifying issue across the sector. Its implications are significant for charities, as it affects their level of uncertainty about the future, and their ability to maximise the benefit of grants. While some of the concern is related to short-term spikes and the astronomic figures seen in 2022, our discussions with clients have highlighted that charities recognise the potential for inflation to reach a higher average level than it has in the past.

As well as being an area of concern for charities, inflation forecasting is key to enable them to project grant giving, withdrawal rates and spending needs. In response, we outline our views for the inflation and interest-rate outlook over the next five years to 2030. This long-term perspective is important – we are deliberately not forecasting short-term inflation in the current year which will be driven by short-term growth and monetary pressures. Our focus is to collate market forecasts and our view of the structural forces that will affect broad inflationary pressures and the interest-rate-setting policy response in order to assess where inflation in the UK may settle on average.

The policy-setting environment

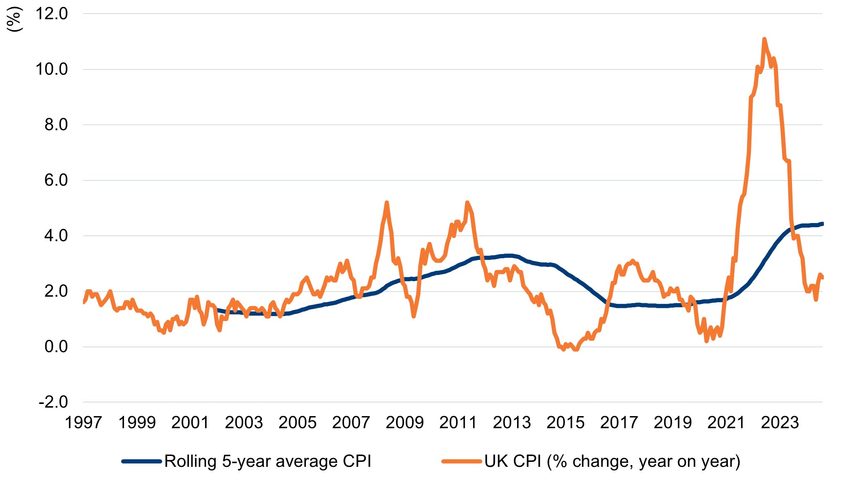

Interest rates and inflation are inherently linked, particularly in the UK where, unlike the US, the mandate of the central bank, the Bank of England (BoE), is focused solely on the delivery of an inflation target. In the UK, this is set by the government at 2% as measured by consumer price inflation (CPI), and any outcome that is 1% above or below this amount must be explained to the chancellor of the exchequer. In order to deliver the objective, the BoE relies on setting interest rates, albeit in recent years it has taken direct action in the gilt and corporate bond markets through quantitative easing (buying predetermined amounts of bonds in order to stimulate the economy and increase liquidity) and tightening (shrinking its balance sheet). The chart below shows annual UK CPI back to 1997, when the BoE was given independence from the government. This highlights the volatility in year-on-year changes in UK inflation as measured by CPI, as well as the considerable length of time when inflation either overshot or undershot this target. We have overlaid a five-year moving average rate.

UK consumer price inflation (% change, year on year)

Bank of England inflation forecasts

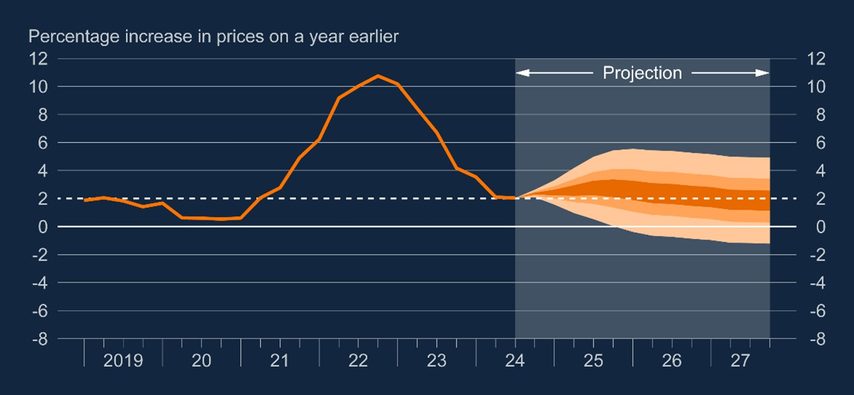

At its monetary-policy setting meetings, the BoE releases its forecasts for a range of economic variables, including inflation, for the next three years based on its interest-rate setting. The primary output for our purposes is the forecast inflation rate and the fan chart below, which conveys the uncertainty around the future path of inflation.

Bank of England CPI inflation projection

Given that the BoE sets interest rates according to a model which predicts what will happen to inflation under interest-rate scenarios, it is, in effect, marking its own homework, and inflation typically comes back to its target over the forecast horizon. The fan chart was subject to criticism from Ben Bernanke, a renowned economist, in his review of the BoE’s forecasting and communication.1

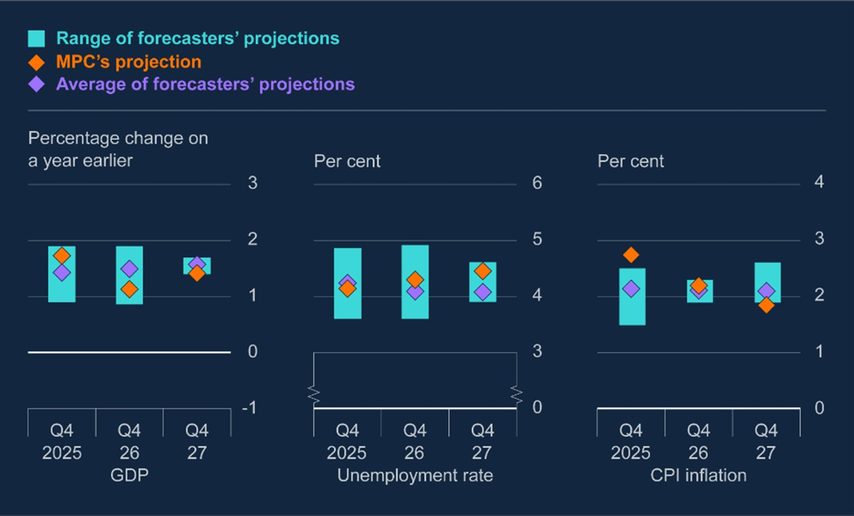

In its report, the Monetary Policy Committee (MPC) also includes the average of market forecasters’ predictions, provided by external researcher Consensus Economics. These are shown for the next three years in the chart below (the latest report is November 2024).

Bank of England summary of external forecasters

The table below shows the actual inflation data that the markers represent:

| Market forecasters | MPC’s projection | |

| 2025 | 2.1% | 2.7% |

| 2026 | 2.1% | 2.2% |

| 2027 | 2.1% | 1.8% |

For long-run inflation assumptions, most forecasters tend towards the BoE’s target, and setting a five-year average number different to that must be based on a view that inflation will consistently overshoot or undershoot the target. As at 28 January 2025, the Bloomberg consensus for CPI is 2.5% for 2025 and 2.2% for 2026.

Bond market expectations

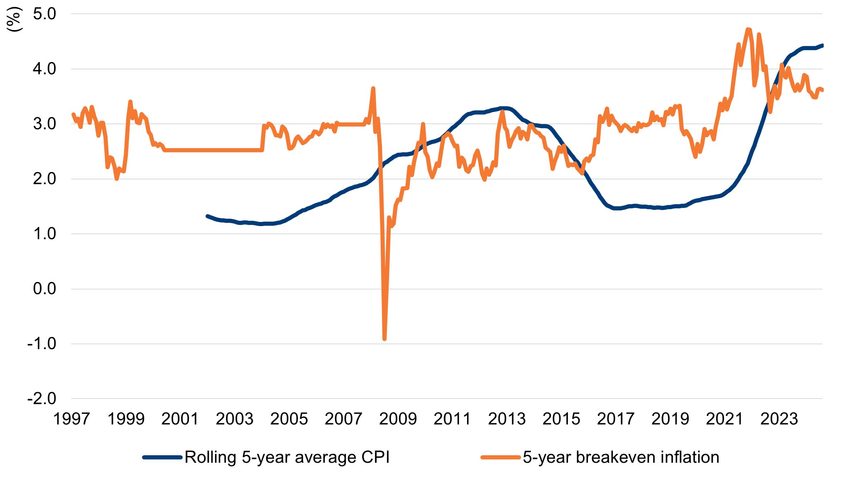

The bond market can be a useful source of forward inflation expectations, by considering what is priced into nominal gilt yields relative to inflation-linked gilts, as shown in the chart below and represented by the grey line, with data going back to 2000. This is calculated as the difference between the real yield (the yield accounting for inflation) received from buying an index-linked gilt, and the nominal yield (the yield before accounting for inflation) from buying a five-year conventional gilt.

Five-year inflation expectations derived from the gilt market2

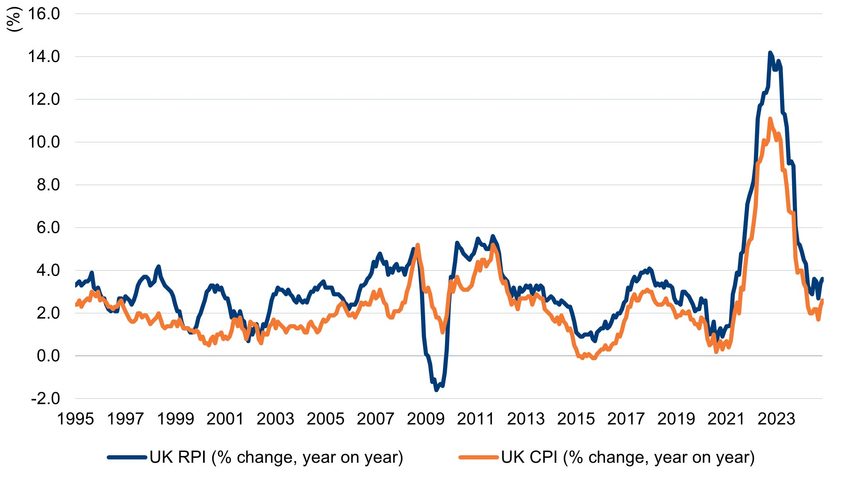

The ‘breakeven’ inflation rate is a measure of the fixed rate that market participants are willing to pay today in order to receive the actual inflation outcome over the subsequent five years. At the end of 2024 this was 3.6%, but while pricing in an active market is a useful starting point, there are reasons to treat this number with caution, as the breakeven level is typically higher than the outturn of inflation. First, buyers are willing to pay a premium for the certainty of receiving actual realised inflation and hedging their risk. This is particularly the case in the UK, where pension funds and insurers are dominant buyers of these assets to protect against liabilities. Secondly, index-linked gilt coupons and principal are currently linked to retail price inflation (RPI) rather than CPI, and for reasons related to different calculation methods and composition of the inflation baskets for the two indices, RPI tends to be higher than CPI. The situation is further complicated by the fact that RPI will be reformulated in 2030 (just beyond this five-year horizon) to be closer to CPI. At the end of 2024, RPI was exactly 1% higher than CPI, while the long-run average was 0.85% higher, as shown in the chart below.

Comparison of UK CPI and RPI

While the five-year RPI breakeven rate at the end of 2024 was 3.6%, that would indicate breakeven market expectations for CPI at around 2.8%. Adjusting for market structure considerations would reduce that expectation further.

Structural considerations

The quantitative easing years which followed the global financial crisis led to rapid asset-price inflation, but not goods-price inflation, which consistently undershot its target. In the early 2000s, the emergence of China as a manufacturing and export centre kept inflationary pressures at bay, boosting corporate profit margins and consumers’ real incomes. Since the Covid-19 pandemic, there has been a regime shift and there are reasons to believe that inflation will now be structurally higher than during the prior two decades.

Some trends remain disinflationary, particularly technological disruption and the integration of artificial intelligence. The adoption rate of this technology in areas previously reserved for humans could have a dramatic impact on labour supply and wage inflation.3 However, other long-term trends have reversed.

Deglobalisation has been replaced with protectionism and reshoring, going against the traditional mantra of comparative advantage in favour of domestic employment. Asia’s role as the global manufacturing centre is changing, and while it remains dominant, local growth and inflation has reduced the cost advantage enjoyed by Western companies. In recent years, there has been a growing focus on investment in decarbonisation initiatives, electrification and reindustrialisation. In the long term, as costs of energy production from renewable sources fall, there is potential for technological disruption. In the short term, however, the impact could be inflationary, with lower investment in fossil fuels while the world remains reliant on them, and a shortage of key minerals such as copper for electrification.4 The peace dividend and low levels of geopolitical risk enjoyed for a long time has changed dramatically in the last few years, and with defence spending on the up and commodity prices more volatile, the inflationary aspects of geopolitical uncertainty are likely to be seen in the data.

We expect inflation data to be more volatile and to settle at a rate above the Bank of England’s target over the five-year forecast period

As a result, we expect inflation data to be more volatile and to settle at a rate above the BoE’s target over the five-year forecast period. Where the average rate settles will depend partly on the reaction function of central banks and their willingness to sacrifice short-term employment and growth for lower levels of inflation. The BoE’s credibility and belief in the mantra of inflation targeting will be on the line.

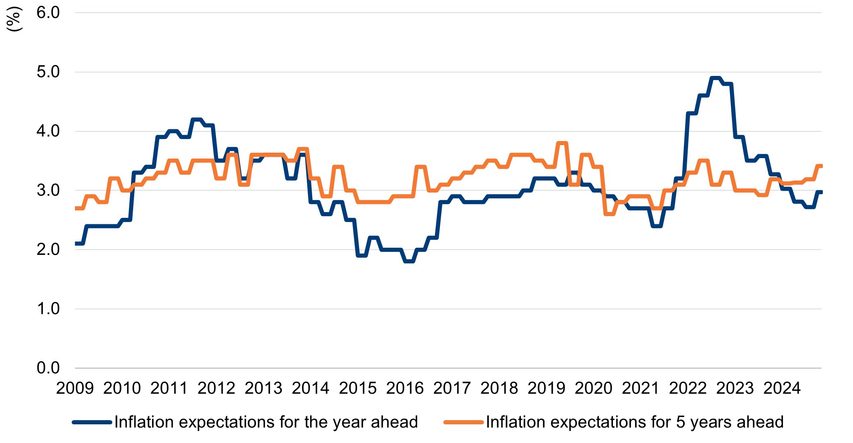

In the short term, measures announced in October’s Budget are likely to push up inflation. According to the British Retail Consortium, 67% of leading retailers stated that they would raise prices as a result of the increase in employer National Insurance contributions and other costs.5 Household inflation expectations have also nudged up, which may feed through to higher wage demands.

Bank of England short and long-term inflation expectations

Interest-rate implications

Interest rates are the BoE’s primary tool to control the price of money and, so the theory goes, the level of inflation through economic activity. We expect policy setting to face very different challenges over the next few years compared to the last 20 years, with the government debt-to-GDP ratio at 100%, stubborn twin deficits (fiscal and trade), a structurally slower economy relative to history, and substantial expected gilt supply. The net result is that investors are demanding higher yields on UK bonds and cash than might otherwise be the case, such that forward interest-rate expectations are currently elevated.

To assess where interest rates are likely to settle is to consider the neutral interest rate – the level at which monetary policy is neither stimulating nor restricting economic growth. This is a hotly debated topic, but we would estimate that the neutral rate in the UK is approximately 3% on a nominal basis. The evolution of demographic trends, productivity growth and the savings and investment balance has brought the neutral interest-rate level down over time, in a similar manner to the reduction in the structural growth rate of the economy.

Current interest rates and gilt yields are therefore in restrictive territory and would be expected to slow activity, particularly in the context of a highly indebted economy such as the UK. Reducing nominal and real interest rates back towards neutral will require a restoration of fiscal credibility, and presents the BoE with the challenge of keeping interest rates high for long enough to calm inflation, but not so long as to drive the economy from low growth to negative growth.

Our estimate

The average levels of inflation and interest rates over the next five years are closely linked subjects. It is likely that cash rates will remain above inflation, creating a positive real return in line with the pre-global-financial-crisis years and without the financial repression of the 2008-2023 period. Provided that the BoE sticks to its inflation-targeting regime, it is likely to hold rates higher for longer to bring inflation down and combat the forces of ‘sticky’ inflation. The path to lower inflation, and whether a recession can be avoided, will rely on the BoE’s policymaking skills. Given the global and local structural factors noted above, we would place a higher probability of inflation reaching an above-target average level than an at-target or below-target level, particularly in the shorter term.

In terms of our forecast point estimate, we believe a 2.5% inflation rate to be reasonable within a 2-3% range for the five-year average. There is a high probability of inflation printing outside of this range within any 12-month period. We would expect the accompanying average BoE base rate to be between 3.5% and 4%, implying real yields of 1-1.5%. Clearly, a recession would change these forecasts, as would a sustained risk premium in the bond market. Forward market pricing of short-term rates is currently in the low to mid-4% range, but this reflects current angst around fiscal policy and could easily drop with a credible fiscal plan or an economic slowdown.

Glossary

Visit our knowledge centre for a glossary of common investment terms and to learn more about key investment concepts.

1. Forecasting for monetary policy making and communication at the Bank of England: a review, Bank of England, 12 April 2024 (https://www.bankofengland.co.uk/independent-evaluation-office/forecasting-for-monetary-policy-making-and-communication-at-the-bank-of-england-a-review/forecasting-for-monetary-policy-making-and-communication-at-the-bank-of-england-a-review)

2. Note that the severe negative rate relates to the global financial crisis of 2008 when market pricing ceased to work effectively.

3. See, for example, Klarna’s announcement that it cut its spending on external marketing suppliers by 25%; even creative industries may see the impacts of generative artificial intelligence: Klarna touts ‘brutally efficient’ AI-enhanced marketing, WARC, 20 May 2024 (https://www.warc.com/content/feed/klarna-touts-brutally-efficient-ai-enhanced-marketing/en-GB/9541)

4. For more on this subject we recommend a very readable speech by the European Central Bank: A new age of energy inflation: climateflation, fossilflation and greenflation, 17 March 2022 (https://www.ecb.europa.eu/press/key/date/2022/html/ecb.sp220317_2~dbb3582f0a.en.html)

5. National Insurance increase will force retailers to raise prices, British Retail Consortium, 15 January 2025 (https://brc.org.uk/news-and-events/news/corporate-affairs/2025/ungated/national-insurance-increase-will-force-retailers-to-raise-prices/)

Key Points

- We believe relative-value strategies are well placed to exploit the current conditions of greater dispersion and heightened volatility.

- US earnings continue to grow but the gap between valuation and earnings has increased.

- There is still room for the US economy to expand, if the new Trump administration can quickly implement its growth initiatives, or contract if it enacts policies that impede growth.

Relative Value versus Directional Alpha

The discount rate is one of the most important metrics in the evaluation of financial assets. Current short-term interest rates are a proxy for the discount rate that is used to determine the net present value of all the future cash flows associated with a financial asset.

The change in cash rates and the discount rate, which began in the aftermath of the Covid pandemic when policy rates began to move higher, signaled the transition from a directional market regime to a relative-value market regime. In our view, this has significant consequences for investors. For example, in a directional regime when the market is in an upward or downward trend, buy and hold equity strategies have typically thrived. On the other hand, a relative-value environment may require a more tactical view across an investment universe that also includes a fair amount of dispersion.

We expect 2025 to continue to favor relative-value alpha strategies that seek to generate a return that is uncorrelated with the broader market, while buy-and-hold directional strategies are likely to face challenges and relatively low premiums. Strategies that utilize relative value have shown increased effectiveness due to dispersion across monetary and policy rates, fiscal tightening, growth rates, inflation rates and returns—not only in equities and bonds but also across currencies and commodities.

Key takeaway: Embrace the macro dislocations and uncertainty as opportunities to generate alpha.

US Inflation

Due to the large Covid-era stimulus, the US experienced unprecedented inflation, which peaked at 9%. Conveniently, the Federal Open Market Committee (FOMC) redefined its inflation target as Flexible Average Inflation Targeting (FAIT), where an average of 2% could be commensurate with a current level of 2.5% (core personal consumption expenditures inflation). Unfortunately for the FOMC and the new US administration, historically it has been the rule, rather than the exception, that inflation jumps or reaccelerates before it settles at levels closer to 2.5%.

We believe there could be a slight increase in the US consumer price index (CPI) to 2.6% relative to the consensus forecast of 2.4% over the next 12 months. More worryingly, the Cleveland Federal Reserve’s nowcasting model forecasts the December 2024 CPI to be 0.38%, equivalent to 4.5% on an annualized basis.1 Its year-over-year inflation forecasts are all around 3%.

Forecasted 12-month Change in US Headline CPI

Key takeaway: Do not ignore risk of inflation running hot before it settles at 2%.

Currencies: US Dollar and Japanese Yen

The value of the US dollar as represented by the US Dollar Index has rallied 9.5% since October 2024. This has quickly become one of the more crowded trades as both systematic and discretionary strategies latch onto this clear trend. However, a strong, or in this case over-valued, US dollar relative to the Japanese yen and Chinese renminbi does not suit the long-term policy goals of the new US Trump administration. To facilitate ‘friend shoring’ and improved competitiveness for US manufacturers, the dollar needs to move in the other direction.

In the meantime, the dollar provides a useful and rare negative correlation to bonds and equities. We believe other currencies such as the yen could balance this trend, perhaps making it the anti-fragile currency for 2025.

US 10-year Treasury note vs. US Dollar Index

S&P 500 vs. US Dollar Index

Key takeaway: Enjoy the US dollar ride while it lasts; look for other currencies such as the Japanese yen to balance exposure.

US Equity Earnings

Thus far, US equity earnings in 2024 have not disappointed, with full-year earnings-per-share (EPS) growth expected to be 11.7%, the highest since the post-Covid recovery in 2021. We expect S&P 500® EPS to fall short of expectations yet still provide healthy growth with little chance of a contraction. Over the next 12 months, the S&P 500 EPS consensus forecast is 12.1%, while our proprietary forecast is 6.6%, or approximately one half that of the consensus. Fundamental analysts tend to be an optimistic bunch who start the calendar year with high expectations but then walk back their outlook as each quarter’s earnings become clearer.

Despite positive EPS growth, the value of the S&P 500 has run ahead of the bottom-up earnings since 2023.2 This is the same period when EPS grew a meager 2% in nominal terms against the total return of 26.3% and inflation of 6.5%. In fact, the gap between valuation and earnings has increased due to the boost related to artificial intelligence (AI), a productivity tool which is as yet difficult to quantify.

S&P 500: Change in Forward 12-Month EPS vs. Change in Price

Key takeaway: US earnings continue to grow but the gap between valuation and earnings has increased.

US Bond Rollercoaster

One of the most difficult directional views since the pandemic has been US bonds as well as sovereign bonds in general. During the past four calendar years (2021-2024), US Treasuries have delivered very little return (cumulative return of -10%3), and very little diversification, with correlations to equities shifting positive. In 2024, US 10-year Treasury yields ranged from 3.6% to 4.7%, with at least two V-shaped cycles over the year.

The below chart illustrates our tactical bond signal which is meant to complement the longer-term carry and term premium. It has reflected the bond rollercoaster and importantly its various turning points.

Monthly Bond Macro Signal Attribution by Concept January 2018 – December 2024

Key takeaway: Net long or short bond positions require relative nimbleness in mind as well as exposure.

US Economic Cycle

Prior to the active stimulus to combat the effects of the Covid lockdowns and large-scale unemployment, the US economic cycle was relatively well behaved for ten years. Given the aggressive policy intervention and very high fiscal stimulus deployed, the US has experienced four phases of the economic cycle in a very short four years.

The below illustrates this journey based on our proprietary leading economic indicators (LEIs) and coincident economic indicators (CEIs). Currently, the US economy is in neither contraction nor recovery, in other words the “no landing” scenario. There is still room for the US economy to expand if the new Trump administration can quickly implement its growth initiatives, such as deregulation and budget cuts. Alternatively, the economy could contract if policies that impede growth, such as tariffs and unfunded tax cuts, prevail.

US Flexcasting Indicators

Key takeaway: As of yet, the “no landing” scenario for the US economy is most likely; consequently, it could expand into a recovery or descend into a contraction. No bets are off.

1 Source: Federal Reserve Bank of Cleveland https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting, accessed on 14 Jan 2025.

2 Source: Factset https://www.factset.com/earningsinsight, as of January 10, 2025.

3 Source: JPMorgan US Treasury Index.