Key points

- For retirees choosing to draw down their retirement portfolios, there is a complex set of trade-offs, which requires clarity on risk.

- A critical factor for the success of a decumulation portfolio is the sequence of returns the retiree experiences.

- However, conventional risk tools may have limited effectiveness in tackling sequencing risk and could result in under-investing a retiree’s decumulation portfolio.

- Decumulation portfolio design and management therefore demands a more comprehensive range of risk measures.

Saving for retirement in a defined-contribution (DC) pension plan is a well-studied topic that has resulted in two main types of investment solution:

- For individual plans, advisors typically suggest pooled mixed-asset portfolios that are risk-aligned to their clients’ risk appetite and capacity.

- For institutional DC pensions (master trusts and employer plans), lifestyle or target-date funds are used for default strategies. These recognise the changing balance of financial risk and human capital and aim to deliver a savings outcome that is palatable. Designed to suit the average plan member, they cater for savers who are, on the whole, disengaged and disinterested. Default-fund investing therefore dominates most pooled plans.

As individuals get closer to retirement, there is typically an increase in engagement with pensions that can be triggered by wake-up packs. These prompt near-retirees to select between pathways depending on their likely retirement choice (annuity purchase, encashment, deferral or drawdown). These pathways represent material differences that demand differently aligned investment strategies leading into retirement. For both institutional and individual DC plans, more specific and personalised choices become critical to bridge members and clients from the saving phase to the decumulation phase.

For the very wealthy, potentially with large DC savings, retirement lifestyle is unlikely to be wholly or even materially reliant upon the performance of their DC pension assets. To the extent that their investment choices are relevant, they are also more likely to seek or receive professional advice.

At the other end of the wealth spectrum, state benefits will underpin the majority of retirement income, and the minimal DC plan assets that do exist are less likely to make a material long-term contribution to retirement lifestyle. Understandably, therefore, full encashment, perhaps to repay debt, can be a sensible option, albeit taking care to avoid adverse tax and benefits impacts.

For those with aspirations for a retirement lifestyle beyond what is supported by guaranteed income sources (such as state benefits or a prior defined-benefit plan), there is increasing reliance on the quality of income that can be derived from DC investments. Those valuing predictability, stability and reliability over flexibility and inheritance appear destined for annuity purchase. However, most do not follow this path. Even with more appealing annuity rates now available, the irreversibility of this step remains unappealing to most retirees.

The majority appear to be attracted to flexibility, or perhaps just to deferring a tough decision. They continue to invest and, at some point, start to draw on their assets to maintain their lifestyle. They become heavily reliant on investment performance to deliver overall return so that they do not run out of assets, and a good sequence of returns so that their portfolio is not unexpectedly depleted.

These retirees face a complex set of trade-offs that good investment design can seek to help resolve:

- Maximising lifestyle and income reduces the potential for legacy and increases the chance of exhaustion of resources and penury in old age.

- Pensioners concerned about old-age poverty can live an unnecessarily frugal lifestyle.

- The potentially material impact of future bouts of inflation on the cost of living indicates a need for real-asset exposure. However, these assets tend to have less stable returns which could lead to sequencing risk that can deplete resources.

- The uncertainty of an individual’s lifespan can only be directly hedged by purchasing an annuity; however, this curtails flexibility and control. Those determined to remain ‘self-insured’ need, therefore, to take a precautionary approach: drawing a lower level of income so there is a higher chance of remaining financially solvent for as long as there is any material chance of remaining alive. This could mean a planning horizon of age 92+ if they seek a high (90%+) probability of remaining solvent in old age.[1]

Measurement and control of risk

Resolving the complex trade-offs faced by clients requires clarity on risk. When investment and risk are mentioned together, there is a tendency to think of evaluating risk in an established way. The first instinct is to focus on the uncertainty of annualised returns. The most common way to quantify this is volatility; however, a variety of other measures like Value at Risk (VaR), the Sharpe ratio and the Sortino ratio are closely mathematically related. This toolkit has served investors well in the context of wealth accretion and growth for decades.

For those building pension drawdown portfolios, it is understandably tempting to reach for these familiar tools in the same way as has been done during the savings phase. However, this could lead to an unappealing negative feedback loop:

- In an attempt to protect retirees from the potential ravages of sequencing risk, a diverse and low-volatility portfolio is created.

- This limits real-asset exposure and is likely to have commensurately low return potential.

- As a result, the maximum safe withdrawal rate supported by the portfolio is unappealingly low.

- In addition, the payments, such as they are, have only scant protection from bouts of inflation that may be experienced during the course of 20 to 30 years of retirement.

- Retirees’ desire to maintain a given lifestyle may mean withdrawing at a higher rate than is durable, which raises the prospect of the portfolio being exhausted long before death.

A desire for low levels of risk has created a situation in which there is a high risk of old-age penury. Low-volatility assets are not necessarily a low-risk strategy.

What is the alternative?

We think the starting point is to reconsider the risk toolkit. The accumulation challenge rightly focuses on asset uncertainty (volatility); however, creating durable retirement income is rather different. We believe risk tools aligned with real-income uncertainty are better suited to serving the drawdown client’s needs.

A critical factor for the success of a decumulation portfolio (i.e. delivering the required real income for as long as needed) is found to be the sequence of returns the retiree experiences.

What is sequencing risk and how dangerous is it?

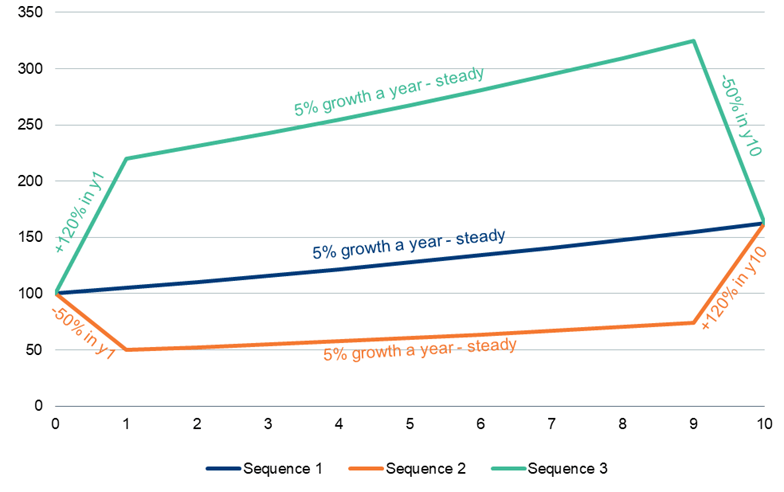

In exhibit 1 we illustrate three sequences of returns delivering the same accumulation outcome. All three deliver a 5% annualised return over a 10-year period: 100 grows to 163.

Green has a good year at the start and a bad one at the end whereas orange experiences the opposite. Irrespective of this, the outcome is the same.

Exhibit 1: Lump sum

Source: Newton, 2024.

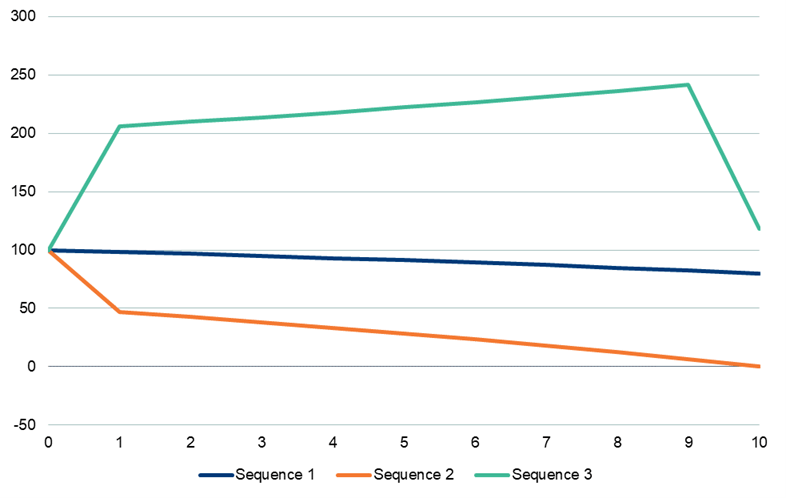

If, however, this portfolio is also supporting a drawdown of 6.3% each year, the same sequences of returns lead to starkly different outcomes, illustrated in exhibit 2. The orange portfolio is depleted entirely over the period whereas green, with the inverse sequence of returns, remains relatively healthy and outperforms blue, with steady returns.

Exhibit 2: 6.3% decumulation

Source: Newton, 2024.

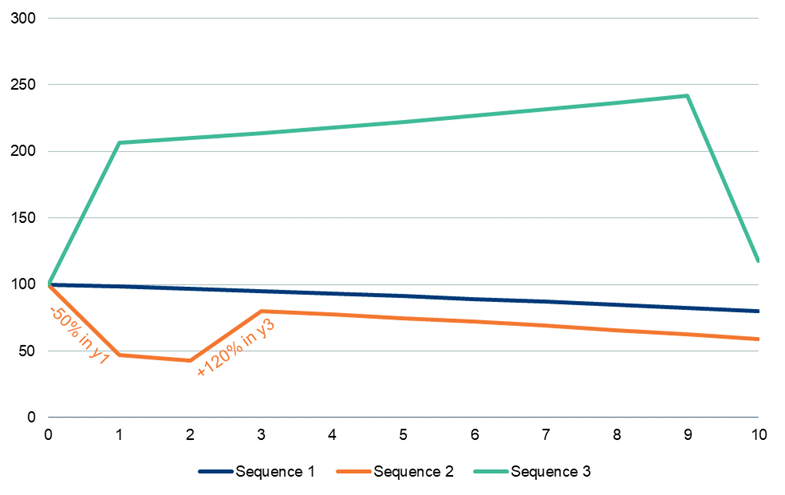

The impact of sequencing risk on decumulation portfolios depends not only on when rises and falls occur, but also on how long an adverse drawdown event lasts. Exhibit 3 shows the improved outcome for orange of an earlier recovery, in year 3 instead of year 10. The annualised return overall is unchanged but, in this situation, the orange portfolio is no longer exhausted entirely.

Exhibit 3: 6.3% decumulation with an earlier recovery

Source: Newton, 2024.

Sequencing risk is particularly dangerous because conventional tools for measuring and managing risk are prone to offering false signals.

The volatility of orange and green pathways in every case above is identical (40%). The blue paths have zero volatility. This ubiquitous measure of portfolio risk has failed to differentiate between the markedly different outcomes experienced by drawdown investors with different sequences of returns; it does not differentiate between the orange pathways in exhibits 2 and 3 that differ only in the length of delay before recovery.

Other conventional risk measures are also exposed to the same flaw. For example, maximum drawdown in the green and orange pathways is also the same at -50%.

Even worse, the conventional evaluation of risk and reward together, the Sharpe ratio, also evaluates the same outcome for green and orange pathways. This is because they both deliver a 5% return and 40% volatility. There is no recognition of the money-weighted value/cost of excess/negative returns.

The conventional approach to avoiding the asset exhaustion seen in the orange portfolio in exhibit 2 is to reduce investment risk by lowering volatility. This appears logical as the blue portfolio, with zero volatility, offers a better outcome.

Sequencing risk is particularly dangerous because conventional tools for measuring and managing risk are prone to offering false signals.

To what extent does lower volatility affect the outcome?

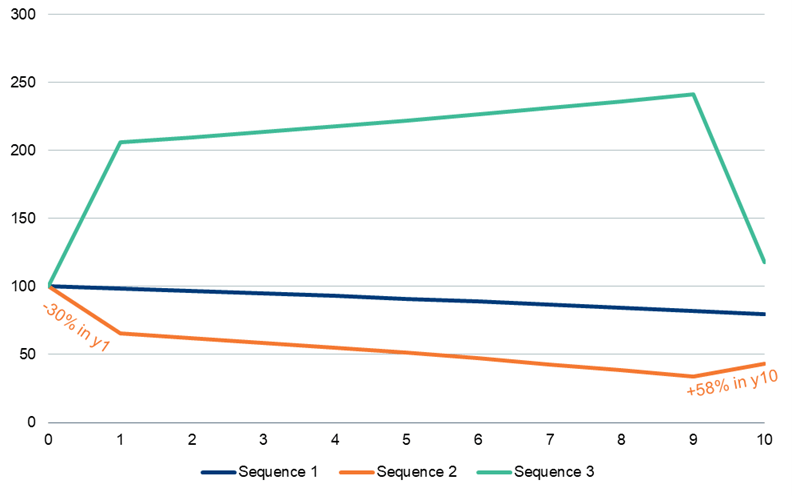

In exhibit 4, the overall annualised returns in each of the pathways remains 5%. However, in this case, the orange portfolio experiences half the previous level of volatility. The fall in year 1 is only 30% and a commensurate recovery in year 10 of 58% results in the same 5% per annum, as in previous cases. The orange sequence volatility is now 20% compared with 40% before.

Exhibit 4 illustrates that even at a much lower volatility level, with an adverse sequence of returns, we still see a worse outcome than those with higher volatility with better sequences or faster recoveries seen previously.

Exhibit 4: 6.3% decumulation with lower volatility

Source: Newton, 2024.

Halving the volatility has been less effective than improving the sequence of returns.

The implications for portfolio construction, manager selection and financial advice are material. In a decumulation setting we can no longer entirely rely on conventional risk evaluation tools:

- Volatile assets may not need to be avoided if they tend to recover quickly from drawdowns.

- Managers adept at building portfolios that recover quickly, for a given level of volatility, can potentially offer clients a better outcome.

- Investment suitability for a client’s risk appetite/capacity in decumulation needs to be evaluated in terms beyond simply a volatility target range.

Decumulation portfolios may be invested more conservatively than necessary

Exhibit 4 illustrated that halving volatility gave some improvement to the orange portfolio versus exhibit 2 (but not as much as the better sequence in exhibit 3). However, the charts assumed equivalent annualised returns in all portfolios. Lowering portfolio volatility is ordinarily linked to lower real-asset exposure, which could lead to a reduction in return potential.

If we assume the risk premium in these models was originally, say, 3%, with cash rates at 2%, the consistent outcome for the orange portfolio in exhibit 4would be 25% smaller still.

We see a vicious spiral where the desire for low sequencing risk, delivered by lowering volatility, drives down portfolio risk-taking and generates lower overall returns with less potential to keep pace with real-world inflation.

Using conventional risk tools that have limited effectiveness in tackling sequencing risk may result in under-investing a retiree’s decumulation portfolio. In other words, a risk-averse retiree who is currently advised to have a low-volatility portfolio could potentially access the higher return potential of a higher-volatility portfolio that is specifically designed to recover quickly from market stresses.

Durable decumulation

Decumulation portfolio design and management is distinct and demands a more comprehensive range of risk measures. We need ways to properly evaluate and control sequencing risk. With sequencing risk in check, we can seek to unlock additional return potential for retirees. This could result not just in higher long-term withdrawal rates, but also in the potential for retirement income to keep pace with long-term inflation, thereby creating ‘durable decumulation’.

[1] Source: Newton calculations based on data provided by the Faculty of Actuaries.

Key points

- With over half the world’s population voting this year, some results might prove consequential to investors in terms of fiscal and monetary policy, inflation, international trade and geopolitics.

- While the US remains the pre-eminent global economy and leads the world in technological development, threats to its global dominance are emerging.

- This is, in part, owing to the trifecta of political change, indebtedness and growing global competition, as identified in our big government, financialisation and great power competition investment themes.

- Higher yields currently on offer from some bonds reflect future risks but may offer opportunities for multi-asset managers to use them as a tactical risk hedge in volatile markets.

With UK politics now firmly settled upon a new course, we note that over half the entire global population will have a similar opportunity in choosing its future political leaders this year. Electorates in many countries are growing tired of established party policies, opening the door for populists to gain a share of power with promises of easy fixes for complex problems.

Just as election results may well change many lives this year, they could also prove consequential for investors in areas such as fiscal and monetary policy, inflation, international trade and broader geopolitical relations.

Interpreting the macroeconomics is key

As a mixed-assets portfolio manager, it is critical to identify and try to understand how these factors may affect different asset classes. In the short term, the impact of most elections is highly unpredictable, as manifesto promises can often evaporate after polling day. As a result, we focus on the fundamental and longer-term drivers which can often be far more significant. These drivers can clearly be shaken by political shocks, so we believe it makes sense for investors to harness the flexibility and adaptability of mixed-asset strategies that can identify opportunities in the face of such uncertainty.

US dominance

Around 60% of global equity markets, by value, are listed in the US. The US economy also makes up around 25% of global GDP, so it is understandable that its elections have the potential for outsized influence on investment portfolios. In many important aspects, however, such as fiscal positions or geopolitical considerations, the outcome of the US presidential election in November this year is unlikely to result in many significant changes, even though the candidates differ in their approach to areas such as immigration, Russia’s invasion of Ukraine, or energy policy. More importantly, the scale and dominance of US equity markets over recent years is the result of generous returns sustained by an era of loose monetary policy and a reassurance that authorities would be likely to intervene to smooth out the worst impact of a sharp downturn in economic activity.

US debt burden

After several years of support, the US now has an unenviable debt burden of more than 121% of GDP. Pandemic aside, this is almost double the level of the previous cyclical peak in the mid-1990s (around 65%). The outlook is also uncertain, with an ageing population likely to place a compounding burden on key welfare costs. We expect these costs to far exceed economic growth and tax revenues. One key US medical provider said recently that it expects health care to account for an additional 2% of US GDP annually by 2044.

Many might argue that this does not matter too much because the US dollar remains the dominant global currency of trade and wealth. To date, those who want to trade with the largest consumer economy globally have had little choice but to accept payment in US dollars. They would then also have little alternative but to invest their dollar profits in US assets (US government bonds and stocks).

US dollar hegemony under threat?

This is a circularity that has supported the US currency, market valuations and ever-increasing public debt for decades. However, the dollar’s hegemony appears to be under threat as other global powers take an increasingly political stance, often at odds with the US’s own foreign policy. The huge scale and increase in wealth of China and India’s middle classes suggest there are now alternative consumer markets for manufacturers to pursue. The emerging economies of two decades ago are now economic powerhouses in their own right and increasingly asserting their stature as new global trading patterns emerge.

While the US remains the pre-eminent global economy and leads the world in technological development, threats to its global dominance are emerging thanks to the trifecta of political change, indebtedness and competitionbetween global powers, as identified by our big government, financialisation and great power competition investment themes.

What does this mean for mixed-asset portfolios?

It is tempting to view higher bond yields (combined with easing inflation) as offering an attractive invitation to invest more in the asset class. However, higher yields can also reflect renewed recognition of the future risk that investors face as the scale of the debt burden comes home to roost. For us, this is a longer-term issue. In the meantime, we believe the higher yield on offer from bonds means there may be opportunities to use them as a tactical risk hedge in volatile markets.

In equities, meanwhile, the US market has become narrowly led by a handful of mega-cap stocks, with ten firms comprising 30% of the S&P 500 index. This is largely thanks to enthusiasm for artificial intelligence, which has the potential to be truly transformative both to existing processes and new innovative possibilities. However, as always, it is important to retain perspective when constructing a mixed-asset investment portfolio, and to try to maintain exposure to transformational trends. We believe this must be considered as part of a further diversification of assets and we remain cognisant that such material tailwinds can fade over time.

All this points to why we believe it makes sense for investors to consider a global mandate, which enables asset managers to pursue opportunities without being tied to asset class or index constraints. Newton’s multidimensional research team identifies and monitors the thematic drivers that shape markets and the outlook for individual firms to identify compelling opportunities, irrespective of location.

Key points

- The cost of living for pensioners has risen significantly, which necessitates a much larger pension pot to sustain a moderate living standard.

- With additional savings being unaffordable for many, a renewed focus on investment strategy can potentially help bridge the gap.

- Delivering higher returns with acceptable risk requires enhanced diversification pre-retirement and new ways to mitigate sequencing risk in the retirement phase.

- Equity income and dynamic factor strategies can work as components within DC solutions.

Higher cost of living

While headline UK consumer-price inflation is helpfully lower now than at any time since July 2021,[1] this does not mean that prices have decreased. The cost for pensioners to have a ‘moderate’ retirement living standard has risen by 34% in the last year alone, according to the Pensions and Lifetime Savings Association (PLSA). It calculates that £31,300 per year is now needed for a single retiree outside London versus £20,800 two years ago – a 50.5% uplift. Couples need 40% more than this.[2][3]

Fixing today’s moderate income level for life for a 65-year-old non-smoker would cost approximately £440k as at 16 May 2024, whereas in 2022, for the PLSA moderate income at that time, the cost was about £378k.[4] Therefore, today’s retiree needs a pension pot that is 16% larger to secure a moderate retirement living standard. Clearly, this ignores the important role that the state pension will play for most retirees. In 2022, at £9,339, it contributed almost half of the PLSA moderate income.[5] However, for the 2023-2024 tax year, at £10,600, the state pension is now only just over one third of the moderate income level. The scale of additional assets needed for a comfortable retirement has, therefore, grown much more than 16% during the period.

Consider also the plight of a retiree in 2022 who at the time could just secure a moderate lifestyle supported by a full state pension. Today, they would have a slightly higher income thanks to state pension increases. However, their income of £22,062 is now 30% behind what is needed to secure a moderate standard of living.

With great foresight, and in an attempt to tackle this inflation risk, they might have purchased an inflation-linked annuity, despite the fact that these are significantly more expensive to secure; the 2022 retiree would have needed to spend 71% more for the same starting level of income.

However, even the purchase of an inflation-linked annuity is not necessarily protective. Such products tend to be linked to official measures of price inflation which do not necessarily translate to the cost of a moderate retirement, given the differing mix of items in the spending basket. For the 2022 retiree with an inflation-linked annuity and state pension, their income today would be uplifted to only around £23,770, a 14.4% rise from the original £20,800 they had in 2022 to secure their moderate lifestyle. This still falls far short of the £31,300 they would currently need for the same standard of retirement, despite spending 71% more on their inflation-linked annuity.

It is no surprise, therefore, that annuitising remains much less popular than drawdown at retirement despite markedly improved annuity rates. According to the Financial Conduct Authority, figures for Q4 2023 show that the number of people selecting annuities is less than one third of the number choosing drawdown to access their pension pot.[6]

Those who remain invested and draw down an income from their portfolio face an array of challenges, however. In our view, to have even a moderate retirement, it is clear retirees today need:

- A more substantial asset portfolio thanks to recent inflation – they will need to accumulate significantly more while working.

- To continue to invest materially after retirement in assets that link to the real economy in order to have the potential to keep pace with future inflationary trends over a retirement span that could easily last 25 to 30 years.

- To avoid the potential ravages of sequencing risk in their retirement portfolio which can cause permanent impairment to their financial security.

The cost-of-living squeeze on workers means that making substantial additional pension savings is a luxury few can afford. The pensions and investment industry must innovate to deliver new solutions if savers and retired investors are to retain confidence in their future.

How is the pensions industry responding?

There has been a lot of interest recently in facilitating access to private equity for DC savers to unlock additional return potential. The rationale for this is that, despite the unappealing illiquidity and opacity of these assets, there could be additional long-term returns owing to higher growth seen historically in private markets; WTW reported this to be around 5% more per year than returns from listed equities.[7]

However, even assuming this remains the case in the future, a substantial allocation of, say, 10% to private equity would lift overall returns by only 0.5% per year.

Calculations by XPS indicate that those starting on their pension saving journey need to either save an extra 6% to 8% per annum of salary or generate additional investment returns of 2% to 4% per annum over their entire working lifetime in order to deliver an acceptable outcome.[8]

Given additional savings are unlikely to be forthcoming, investment returns need to do the heavy lifting. Private equity alone looks unlikely to bridge the gap in the return potential needed. How else could investment returns for DC investors be enhanced?

We think two strategies could be critical to help achieve this:

- Enhance the diversification of DC investments to support a higher allocation to real assets for longer in both accumulation and drawdown, without materially altering the risk profile

- Generate additional returns from existing allocations

How can these goals be delivered?

To enhance diversification, we think schemes could consider the role of dynamic factor strategies as a crossover asset between equities and bonds. These types of strategies can potentially target substantial absolute returns in excess of the expected return of bonds – and some managers can achieve this with little more risk and zero correlation to equities; however, a positive return is not guaranteed and capital losses may occur. Better diversification could improve returns from the lower-risk portion of the DC portfolio. They can also offer daily pricing, access and liquidity in a UCITS wrapper, which is a convenient alternative, useful while schemes wait for suitable private-market offerings to emerge.

With greater diversification, the portfolio allocation to equity assets can be both increased and re-activated.

Currently, most DC default investment strategies are run to a minimum-cost model. Plan sponsors have been driven to compete on lowering costs to members as these are easy to compare. The result is that most equity assets are held passively in index allocations. This has arguably served DC savers well over the period following the global financial crisis as quantitative easing flooded markets with cheap money, lifting all asset prices and therefore indexes with them.

Why is a different approach needed?

Since the pandemic, inflation has accelerated and so too have interest rates. The era of cheap money has now ended, removing a key tailwind for indices. Equity-index performance has recently been driven by a narrow group of global leaders that now dominate the technology sector, thanks largely to optimism around artificial intelligence. While this may have somewhat further to run, such narrow market leadership could be risky for index investors like DC default strategies. Without the tailwind of cheap money, index performance is expected to be much more uncertain in years to come. A new strategy is therefore needed for DC default investment in equities.

We believe that active management is critical to deal with narrow market leadership, the end of free money and a range of other factors that make the outlook for indices in the coming decade look unappealing. We think that thematically underpinned fundamental research will be key to selecting future winners that will benefit from potential tailwinds, such as reshoring and the energy transition.

What difference might this make?

The value added by active management is never certain so care and due diligence will be needed in selection and oversight. To the extent that a selected manager’s targets are delivered in practice could, however, make a material difference to long-term returns. In addition, with dynamic factor strategies offering the potential for a more diverse portfolio, it may be possible to increase the allocation to real assets such as equities. This could deliver an additional boost to both long-term returns and mitigation of future inflation risks. However, a positive return is never guaranteed and capital losses may occur.

These steps could potentially go a long way to bridging the gap between affordable savings and comfortable retirement, and ought to be an appealing competitive advantage for plan sponsors tired of the race to the bottom on fees.

What about after retirement?

The other factor that can make a big difference to the affordability of a comfortable retirement will be improving the investment strategy following retirement. The current consensus is focused on low-volatility investments in an attempt to avoid sequencing risk. The result is post-retirement portfolios dominated by fixed-income securities. These not only have little prospect of keeping pace with future inflation shocks over a 20 to 30-year retirement span, but also support only low long-term withdrawal rates, potentially leaving retirees short of PLSA target income levels.

Our decumulation research shows that there are ways to tackle sequencing risk directly through asset choices that react well in left-tail events.

Lowering portfolio volatility is an indirect and rather inefficient way to mitigate sequencing risk because it generally comes at a significant expense to return potential. Good overall returns are the primary determinant of a durable decumulation portfolio. Therefore, sequencing-risk mitigation actions that also impair returns can be self-defeating. Instead, our decumulation research shows that there are ways to tackle sequencing risk directly through asset choices that react well in left-tail events.

We find that some assets become sought after as periods of market stress unfold. They therefore recover more quickly than others. This kind of behaviour is particularly helpful to exploit when creating portfolios to support durable decumulation in retirement.

For example, value and quality-biased equity income strategies tend to hold stocks that see an earlier recovery in bids during times of market stress. As a result, they tend to suffer less and recover faster during market crashes, leading to lower sequencing-risk exposure if held in a retirement income portfolio. Tail-risk-protection strategies can also be tuned to help portfolios bounce back quickly, and the high-quality diversification and return potential of dynamic factor strategies have an important role to play too.

These strategies can help build decumulation portfolios that could support durable drawdown and, because they can potentially sustain a materially higher allocation to real assets than is commonplace today, are potentially more likely to keep pace with future inflation over the possible 20 to 30-year retirement span.

At Newton, we run equity income and dynamic factor strategies which can work as components within DC solutions. We also offer bespoke investment solutions which encompass flexible asset allocation, sophisticated risk management and a multidimensional research approach. If you are considering the design of a post-retirement default strategy for your plan, talk to our solutions team.

[1] As at 31 April 2024. Source: Consumer price inflation, UK: April 2024, Office for National Statistics, accessed 5 June 2024: https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/april2024

[2] https://www.plsa.co.uk/Press-Centre/Press-Releases/Article/Latest-Retirement-Living-Standards-show-change-of-UK-public-expectations

[3] https://www.plsa.co.uk/Press-Centre/News/Article/articleid/1297

[4] Source: Newton and Sharing Pensions: https://www.sharingpensions.co.uk/annuity-rates-chart-latest.htm

[5] Benefit and pension rates 2022 to 2023, GOV.UK: https://www.gov.uk/government/publications/benefit-and-pension-rates-2022-to-2023/proposed-benefit-and-pension-rates-2022-to-2023

[6] Retirement income market data 2022/23, Financial Conduct Authority, 16 April 2024: https://www.fca.org.uk/data/retirement-income-market-data-2022-23

[7] Why defined contribution pensions should choose private equity as the first step into illiquids, WTW, 12 April 2024: https://www.wtwco.com/en-gb/insights/2024/04/why-defined-contribution-pensions-should-choose-private-equity-as-the-first-step-into-illiquids

[8] CPI falls to 2.3% but has it fallen far enough for DC savers to catch up?, XPS Pensions Group, 22 May 2024: https://www.xpsgroup.com/news-views/insights-briefings/cpi-falls-23-has-it-fallen-far-enough-dc-savers-catch

Key points

- One of the common approaches to settling upon an appropriate retirement investment portfolio is the use of a multi-pot model – separating pots of assets according to different underlying purposes.

- However, the demonstrable weakness of many multi-pot drawdown portfolios is that they are automatically rebalanced across the pots, meaning there is no discretion applied to the timing of sales of higher-risk assets to refill the short-term pot.

- Nevertheless, there are options, such as the use of income-focused equity and multi-asset portfolios in the mid and long-term pots, and directing those dividends straight into the short-term pot.

Since the introduction of the pensions freedoms legislation in 2015 which allowed savers more flexibility in how they access their defined contribution pension scheme, retirees have embraced the opportunity to do something other than lock into annuities at retirement. The majority now exercise this freedom, with most of those who have larger DC pots continuing to invest while drawing down to meet the balance of their income requirements in retirement. With this option comes a plethora of decisions to be made and potential risks. However, few are well equipped for the task and only a small proportion take qualified professional advice; fortunately guidance is increasingly available.

Whether guided or advised, one of the common approaches to settling upon an appropriate retirement investment portfolio is the use of a multi-pot model. By separating pots of assets according to different underlying purposes – for example a ‘wallet’ for day-to-day spending, a ‘rainy-day fund’ for unexpected expenses, and a long-term pot to generate returns – retirees implicitly commit to using those assets for a particular purpose. However, does the multi-pot model for retirement investment decision making result in the best use of assets or is it simply a cognitive tool to assist asset allocation?

The implicit commitment of assets to pots can mean that the ‘leave well alone’ assets for later life offer less temptation to overspend today and the ‘wallet’ pot offers some degree of confidence that parsimony is unnecessary – avoiding the risk of underspending. There is a clear mental accounting that matches the pots to purpose, providing discipline.

Evaluating the multi-pot retirement investment strategy

Nevertheless, how optimal is the investment strategy that is implied by this pot-type model and how does it navigate market uncertainty? Critically, does it reduce sequencing risk, and can other investments offer a superior outcome?

Evaluation of the multi-pot model is a task that several researchers (e.g. Huxley, Burns and Pfau) have undertaken already.1,2 The value it creates has been demonstrated to be connected to the mechanism used for rebalancing across the pots as markets move and income is drawn. Clearly, the parameters used for comparing results, as well as the nature of the market model used, are also important. While different examinations have revealed different winners, there is one unifying strand in the research, which relates to the weakness of market-agnostic time-based rebalancing to a static target asset allocation. The fact that this is a common approach used in many cases suggests clients could potentially be better served.

The demonstrable weakness of many multi-pot drawdown portfolios is the fact they are automatically rebalanced across the pots. This means that spending from the ‘wallet’ is effectively just spending across all the pots. There is no discretion applied to the timing of sales of higher-risk assets to refill the spending bucket, nor is there ongoing re-evaluation of the mix between growth and later-life (perhaps annuity purchase) pots. There are notable exceptions, such as what Nest is doing in its retirement default portfolio, where trustees decide how much to pass over to the ‘wallet’ each year and consider the overall appropriate asset mix. The challenge is doing this in a personalised manner rather than through a one-size-fits-all default structure.

Even those pensioners benefitting from personalised advice from an independent financial adviser may find that discretionary rebalancing is not a service that is offered. Advisers are typically specialists in personal finance and tax planning rather than investment markets. Making discretionary portfolio changes puts the adviser at risk of being criticised for mistiming the asset switches. In many cases, they may be uncomfortable making market timing calls, and historical practice may have been to rely on ‘pound cost averaging’. While this has been adequate in regular savings accumulation, it is demonstrably not the case for decumulation investors, as it results in ‘pound cost ravaging’, where programmed withdrawals from portfolios result in pensioners experiencing higher wealth uncertainty than the volatility of underlying assets.

Even when a discretionary portfolio management service is employed, the push for efficiency means that standardised model portfolios are often used and, as a result, the asset allocation is not client-specific so cannot take account of any particular level of income being drawn down.

What can be done?

Clearly there are some discretionary advisers who, for a suitable fee, will use their own research to make the timing call for their clients. For those that do not want to pay such fees, and for institutional DC plans offering decumulation in-plan using robo advice to guide members, other options are available.

If the multi-pot model is deemed unnecessary, a risk-appropriate multi-asset investment could be used given that, within the portfolio, the asset manager may make asset-allocation calls as part of the overall active investment process. While this may lack calibration to individual drawdown levels, both risk capacity and market path dependency can be actively and expertly managed.

The potential benefits of an income focus

For those that want to retain the personalisation, cognitive comfort and ease of understanding that the multi-pot model offers, there may be another option – the use of income-focused equity and multi-asset portfolios in the mid and long-term pots. By using their income share classes, the dividends can be directed straight into the ‘wallet’. This effectively devolves the timing of moving assets to the individuals closest to the economic activity that actually underpins the returns as a whole – the organisations that are using pensioners’ capital. They are arguably in the best position to determine when they can pay sustainable dividends – they pay dividends when they feel this is the smartest way they can add value for their shareholders, as opposed to retaining earnings to finance growth or buying back shares. The fact that the pensioners’ portfolios contain a diverse array of dividend-paying securities means the timing of ‘rebalancing’ is smoothed by the separate decisions of the firms, each one making the optimal timing choice for its business.

The aim of income strategies such as our Global Equity Income and Multi-Asset Income strategies is, of course, to generate attractive returns through holding companies accountable for their decisions through stewardship, while carefully selecting those with the best prospects for sustaining and growing the income and overall return.

Naturally, one may ask, in this arrangement, what if the income flowing into the short-term/cash pot is not enough (or is too much) compared to the pensioners’ actual spending needs?

In such a case, a pensioner’s additional demand could serve as a first indicator (to them) that their spending may be too high to be sustainable over the long term without capital erosion. Alternatively, if the short-term/cash pot is growing steadily, it could indicate that their investments are doing well enough to support additional spending. In either case, this would lead to a need to engage with the drawdown platform, along with its built-in guidance tools. In the process, the pensioner should actively reconsider their situation, rebalancing their pots if necessary, and become cognisant that they shoulder responsibility for any decision to decumulate faster (or slower) than is naturally supportable. In doing so, they can be guided as to the risks they are exposing themselves to.

The pensions freedoms come tied up with a complex set of personal responsibilities, and for those who find the burden is too great and are not prepared to seek expert advice, the annuity option is always available.

Sources:

- Stephen J. Huxley and J Brent Burns, ASSET DEDICATION: How to Grow Wealthy with the Next Generation of Asset Allocation, 22 October 2004.

- Wade D. Pfau, Time Segmentation as the Compromise Solution for Retirement Income, 27 March 2017.

Key points

- Our themes highlight to us areas of potential opportunity, and they also reveal companies, sectors and asset classes that face significant headwinds, and which we should therefore avoid.

- Our China influence and great power competition macro themes have indicated that as Western economies seek to reduce their reliance on China, we are likely to see the deflationary effect of globalisation diminish.

- However, trends identified by our smart everything group of micro themes could create some significant productivity gains and lead to a more deflationary force.

Thematic research is one of the many research capabilities our investment teams have at their disposal via our multidimensional research platform. Themes are instrumental in helping us understand the investment backdrop, providing us with a long-range lens through which to view the structural changes that are taking place across the globe. Our themes highlight to us areas of potential opportunity, and they also reveal companies, sectors and asset classes that face significant headwinds, and which we should therefore avoid.

Our themes encompass macro themes, which encapsulate geopolitical and economic shifts, and micro themes, which capture key technological, social and environmental trends.

Importantly, for our mixed-asset portfolios, we tend not to focus on a single theme; we consider the spectrum of themes to ensure that we are aware of the broad backdrop that is driving change across global economies.

Themes and asset allocation

Our China influence macro theme recognises that China is a much bigger part of the global economy now than it was 20 years ago, and what happens to China has significant implications for the rest of the world. It also links to our great power competition theme – the West continues to be much more aware of the security concerns related to its reliance on China, leading to trade and tech wars. As Western economies seek to reduce their reliance on China, we are likely to see the deflationary effect of globalisation diminish, as those economies move away from offshoring manufacturing to low-cost locations, bringing it back to developed markets. We therefore expect to see slightly higher levels of inflation and interest rates in the future.

We have had very little exposure to bonds in our mixed-asset portfolios for quite a long time. However, more recently, as central banks have raised interest rates and moved away from quantitative easing (QE), and governments have been more focused on providing support to the real economy rather than financial markets – often referred to as ‘people’s QE’, we have had the opportunity to increase exposure to fixed income.

In contrast, trends identified by our smart everything group of micro themes, covering areas including big data and artificial intelligence, could create some significant productivity gains and lead to a more deflationary force. This could not only create investment opportunities, but also cause considerable disruption to many industries. Therefore, at times, there may be competing forces driving our themes, and we are continuously assessing which overriding trends will play out over the longer term.

Bringing micro and macro themes together

We also see a number of interesting opportunities stemming from our big government macro theme, a key element of which is environmental policy, which is likely to drive substantial capital into areas focused on decarbonising our economies. The difficulty with this is that all countries are trying to decarbonise at the same time, so the costs are rising. Our Earth matters micro theme, which was created nearly two decades ago, has evolved into natural capital, to reflect that with the growing understanding of the importance of environmental issues, we are likely to see investment accelerate. We therefore need to find the companies that can benefit from this spending on natural capital.

We think that it will not only be clean energy such as solar and wind power that will benefit, but also other forms of decarbonisation. Take HVAC (heating, ventilation and air conditioning) equipment, for instance. 40% of global carbon emissions come from heating,1 and so upgrading this equipment is one of the easiest ways for a company to reduce emissions, given that new systems are considerably more efficient than legacy ones. Investors are frequently asking investee management teams about their lifetime carbon emissions, and so an efficient way to show progress on this matter is for companies to upgrade their HVAC systems, as the payback time of the investment during a period of high power prices is relatively short. This is why clean energy has evolved into a new decarbonisation theme, to highlight that it is not just about the buildout of renewables; there are many other solutions that can play a role in decarbonising our economy.

Source:

1https://www.iea.org/reports/renewables-2019/heat

Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic research structure the security has been assigned to.

Amid price instability, heightened geopolitical risks and volatility, investment opportunities remain.

Last year was a transition year – and a painful one at that. The end of the Cold War, the break-up of Russia, and the advancement of China had driven inflation and interest rates lower for decades, creating a benign environment for risk assets. However, the 2020 Covid-19 pandemic led to unprecedented spending and assistance – with global central banks spending the equivalent of nearly US$800m every hour for 18 months. This was bound to have an inflationary impact, with the subsequent environment seeing the fastest, most aggressive interest rate-hiking cycle in decades.

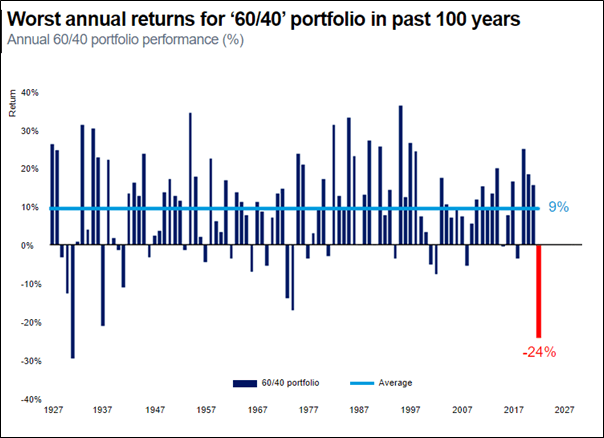

In the context of this transition, 2022 was a difficult year across all asset classes, disrupting the negative correlations that have supported the traditional 60/40 equity/bond asset-allocation model in recent years. Against this backdrop, we believe bonds may no longer be the best way to stabilise portfolios. While it appears unlikely that we will return to the c.15% interest-rate levels experienced by past generations, a return to zero interest rates also looks improbable any time soon. This is why we believe it is important to start considering a broader set of alternative investments.

Source: BofA Global Investment Strategy, GFD Finaeon. 2022 estimate is annualised as of December. Reprinted by permission. Copyright © 2023 Bank of America Corporation (“BAC”).

I would highlight the attractiveness of a few such alternatives, such as carbon. In 2005, carbon emissions trading schemes were initiated, allowing companies to sell on unused credits which bigger polluters can buy. Europe has become the largest carbon trading market in the world. Today, with the increased global focus on emissions and lowering targets, each year the supply of unused credits is becoming constricted.

Another area of alternatives relates to continuing electrification, which is driving greater demand for commodities. Such is the growing demand for commodities that we may eventually see governments start to hoard supply in anticipation of future shortages – such as in copper. Other aspects of the energy transition, like wind farms and solar panels, have other attractive qualities, such as somewhat predictable cash flows thanks to implicit and explicit government support.

Another potential area where alternatives can offer diversifying effects is volatility itself. Volatility can be seen as an asset class, and some of the instruments in this area can offer the prospect of equity-like returns with roughly half the volatility.

Reflecting this view, allocations within our Real Return strategy have increasingly favoured alternatives in recent years. As of the end of April 2023, just under 20% of the strategy was invested in alternatives such as infrastructure, music royalties, energy storage, commodities and risk premia.

We also favour consumer companies with pricing power as well as domestic producers (companies that do not have to worry about foreign-exchange issues), commodities and health care. The latter has been an unloved area thanks to worries over patent expiries. However, post Covid, the health-care industry is trying to catch up on procedures that were delayed, while innovation in drugs has become an exciting area that could save governments billions in health-care provision, particularly in areas like Alzheimer’s and obesity.

Elsewhere, we see opportunities in China’s reopening, and while we find select individual Chinese/Hong Kong securities attractive, we believe index futures can be a liquid and efficient way for a diversified, multi-asset strategy to gain exposure to the reopening story. Liquidity is key for us in this market as we want to be able to exit quickly should it be necessary.

While we value alternatives’ attractive diversification and return potential, we believe there is still a place for risk assets. Although we are cautious, we view the use of alternatives as providing an opportunity to be more dynamic. If we are to learn from times such as the high-inflation, rising-rate environment of the 1970s, we must remember that such periods also saw aggressive equity rallies, in spite of the challenging economic backdrop. It is therefore important to be adaptable.

We do expect volatility to rise, and we believe that the way in which an investment strategy manages that eventuality is likely to become increasingly important. Volatility does create opportunities and dispersion of performance between different securities, sectors and asset classes, which we believe favours active stock selection.

Key points

- Given the intangible and complex nature of the topic, applying a biodiversity lens to investment decisions is not straightforward.

- We believe that any biodiversity investment framework needs to be designed to evolve as our scientific understanding, regulation and industry-leading practices develop.

- There are numerous ways in which biodiversity can have an impact on a business and investments, and these financially material risks can be physical, transitional or systemic in nature.

- We expect such risks to emerge more frequently in the future, as we have seen with climate change.

Application to investments

Taking a topic as intangible and complex as biodiversity and applying it to investment decisions is not easy. There are lessons that can be learnt from how the investment industry has approached climate change, but biodiversity has its own additional challenges. A tonne of carbon emitted anywhere on the planet has very similar real-world outcomes, whereas one particular tree lost or planted in a region does not have the same impact as the same tree in another location, or indeed a different species in the same location. The role of location-based data and the need for granularity is especially important in relation to biodiversity, even relative to other environmental issues.

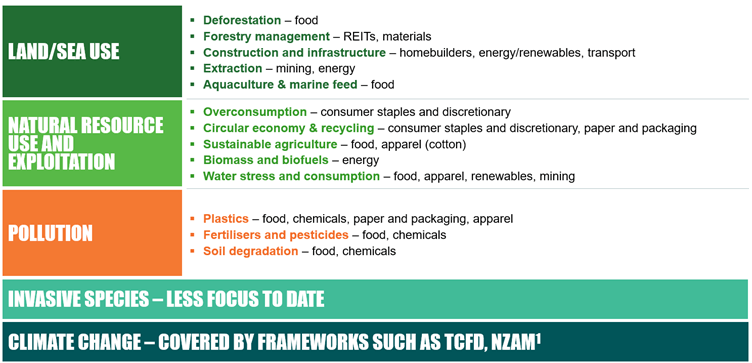

The Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) is a leading authority on the science of biodiversity and public policy responses. It cites five direct drivers of biodiversity loss: (1) land and sea use and change, (2) natural resource use and exploitation, (3) pollution, (4) invasive species, and (5) climate change. These can be viewed as a channel through which humans have an impact on nature, and as we begin to build out our own framework, we are looking at using these to connect biodiversity to investments.

The five drivers can first be connected to corporate activities, and subsequently industries that we may invest in. This is essentially a materiality mapping exercise – one in which we can take tangible components of one issue and consider how different industries may affect it. Below is an indicative example of how each driver links to specific issues and industries (it is not exhaustive). We find that the connection of our scientific understanding of what is driving biodiversity loss to the products and services that companies offer, and the way in which they produce or conduct these, is one of the key areas for investors to bridge.

Financials play an overarching role

Note: 1 TCFD = Task Force on Climate-Related Financial Disclosures; NZAM = Net Zero Asset Managers initiative.

The issues highlighted above are not new environmental challenges – deforestation, plastic pollution and water stress are all well understood by investors and companies. In some ways, biodiversity is now used as a new lens through which to view these issues, and we are even seeing some use the term to refer to any environmental issue that is not explicitly climate change, which highlights the breadth of this topic. This means that many of the biodiversity targets and engagements we now see discussed are not necessarily new but are the relabelling of existing initiatives. As investors, we need to be aware of this, but equally, the nature of the subject means that it requires breaking down into actionable issues. Work has already been done on some of these, but the focus on biodiversity enables us to concentrate more on the real-world impacts of these, and at a systems level, rather than in isolation.

At present, this still has its limitations. We believe that any biodiversity investment framework needs to be designed to evolve as our scientific understanding, regulation and industry-leading practices develop. For example, there is currently very little research on invasive species and the way in which corporate activities may affect them. The problem regarding the grey and red squirrels is well known – the introduction of the American grey squirrel has led to the endangerment of the European and Asian red, as the greys carry a specific virus that can kill the red squirrels, and they also eat the red’s primary food source before they are able to consume it. However, it is not easy to identify and analyse the way in which corporate activities influence such practices.

Financial materiality

There are numerous ways in which biodiversity can have a financial impact on a business and investments. We have seen limited examples to date but expect such risks to emerge more frequently in the future, as we have seen with climate change. Often, the ESG (environmental, social and governance) case studies that we see demonstrating financial materiality are those where a risk materialises from a significant catalyst – a strike resulting in cancelled flights, labour issues in a supply chain being investigated by governments or NGOs (non-governmental organisations), or physical risks destroying land or property. We have not yet seen this type of acute risk within biodiversity – it may indeed be more chronic in nature. Moreover, given that this is such an intangible topic, and one often used as an umbrella term for a range of specific concerns, such as deforestation, we may not see events labelled as biodiversity issues, where in fact they are. Water stress affecting operations and supply chains is a good example of this.

In terms of how biodiversity issues can have a financially material impact on a company, first there are physical risks. For instance, biodiversity loss is linked to deforestation, which exacerbates climate change by reducing the planet’s carbon sequestration abilities, as well as its ability to provide humans with protection against extreme weather events. Biodiversity is also interconnected with soil degradation, which negatively affects agricultural yields and therefore our ability to produce foods efficiently. Furthermore, the Food and Agriculture Organization of the United Nations notes that pollinators affect 35% of global land use for agriculture, which covers the production of 87 of the leading global food crops.1

In May 2020, the European Union adopted a Biodiversity Strategy for 2030, which aims to protect nature and restore ecosystems. This will seek to increase the number of protected sites and will include binding nature restoration targets. It will also create funding to improve understanding of biodiversity, monitor impacts, and ensure these are integrated into business and investment decision making.2 Consequently, there are clearly transition risks as regulation and international coordinated efforts to promote biodiversity increase.

Finally, there are systemic risks as a result of human reliance on biodiversity. For example, approximately 60,000 plant species are harvested for traditional or modern medicine, comprising key raw materials in professional medicines and consumer products.3 It is likely that the medicinal benefits of many natural resources have yet to be discovered, as plants are often crucial to our understanding of medicines and biology, from peppermint as a natural antispasmodic to ginger as a treatment for nausea. Many ecosystems have been underexplored (e.g. the ocean) and new species of plants and animals are regularly being identified – suggesting that there are many species and therefore benefits yet to be discovered. Furthermore, research suggests that infectious diseases can thrive where biodiversity has been depleted. As the Dasgupta Review: The Economics of Biodiversity highlights, if nature is undisturbed, it will generate life, and continue to provide services that we do not pay for, but are of great benefit to humankind.

Sources:

- Why bees matter: The importance of bees and other pollinators for food and agriculture, Food and Agriculture Organization of the United Nations, 20 May 2018

- Biodiversity strategy for 2030, European Commission

- CITES and Medicinal Plants, CITES

We assess the UK’s current monetary and fiscal predicament and the prospects for the gilt market.

Key Points

- Radical UK government policies which aimed to slash taxes to aid growth have been replaced by a renewed focus on fiscal discipline.

- Panic has subsided in the gilt (UK government bond) market, but the perceived hit to credibility and confidence are longer lasting.

- Mortgage rates have yet to fall materially, remaining at almost double the rates they were at six months ago.

- The decision not to extend generalized energy price caps beyond the spring reduces the potential hole in the public finances, but higher implied future borrowing costs, on top of the hefty additional interest bill on index-linked gilts already incurred, still leaves a sizeable gap to fill.

- Should the Bank of England’s Monetary Policy Committee press ahead with quantitative tightening (QT), and the chancellor plug the budget gap with fiscal restraint, it may mean fewer interest-rate rises.

- In our view, having reversed most of the sell-off since late September, gilt yields are not high enough to represent compelling value versus better-rated New Zealand, Australia and, to a lesser extent, US government bonds.

It has been a tumultuous few weeks for the United Kingdom, not least for the gilt (UK government bond) market. As I wrote recently in a blog entitled The closest thing to crazy? in the aftermath of the not-so-mini budget in late September, that ill-fated fiscal statement contained what we believed to be many of the wrong policies and the wrong priorities at the wrong time.

The statement elicited a damning verdict from the financial markets, as well as in opinion polls, and it caused havoc for UK defined benefit pension schemes, necessitating emergency intervention from the Bank of England. As predicted in the blog, the authors of those seemingly ill-judged policies (Prime Minister Liz Truss and Chancellor Kwasi Kwarteng) were both forced to resign.

New Leadership

The UK now has a new prime minister and a new chancellor in Rishi Sunak and Jeremy Hunt respectively. Radical policies which aimed to slash taxes to aid growth have been replaced by a renewed focus on fiscal discipline. Panic has subsided in the gilt market, but the perceived hit to credibility and confidence are longer lasting. Not least, mortgage rates have yet to fall materially, remaining at almost double the rates they were at six months ago. Recent data also suggests an understandable reluctance by consumers to buy big-ticket items.

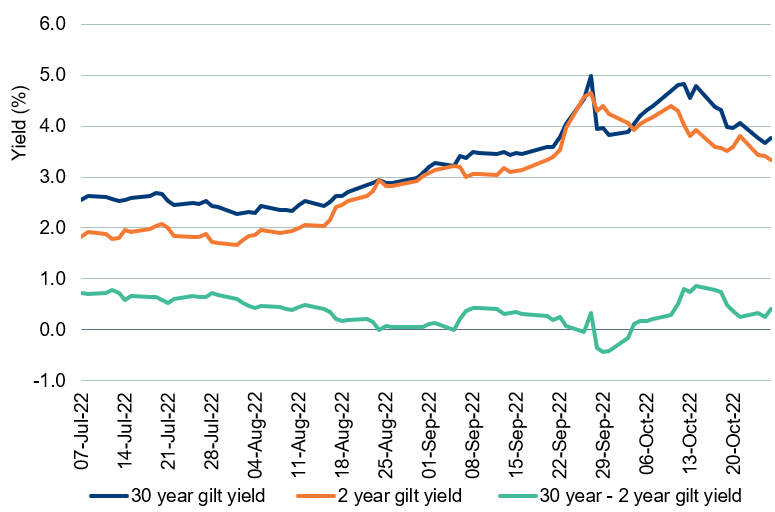

Gilt yields have retraced somewhat from the 5% peak seen in late September, but they remain materially higher than over the summer. Not only has the level of gilt yields remained volatile, but the curve shape has been very erratic, as the Bank of England plays ‘whack-a-mole’. The chart below shows the 2-year and 30-year gilt yield history since former Prime Minister Boris Johnson was forced to resign in early July.

UK Gilt Yields July 7 – October 26, 2022 (%)

Source: Bloomberg, October 26, 2022

Emergency intervention on financial-stability grounds in late September arrested the spike in long-term gilt yields which had been brought about by forced selling from the liability-driven investing (LDI) community and caused the curve to invert briefly. However, in the first half of October the curve re-steepened, before the budget measures were progressively reversed and the curve flattened again. The Bank of England’s decision to exclude any gilts dated 20 years or more from its plan to sell gilts for the remainder of 2022 also supported this flattening.

Rating Downgrades

The decision not to extend generalized energy price caps beyond the spring reduces the potential hole in the public finances, but higher implied future borrowing costs, on top of the hefty additional interest bill on index-linked gilts already incurred, still leaves a sizeable gap to fill. Credit rating agency decisions to revise the outlook on the UK’s rating to negative over recent days reflect this.

See-sawing energy pricing policy also has implications for inflation; former Chancellor Sunak’s policy of allowing the market to set utility prices but paying rebates meant that headline inflation rose, at significant cost to the Exchequer in the form of higher interest and principal payments on index-linked gilts. Former Prime Minister Truss’ price capping pushed down headline inflation, but other policies threatened to push up core inflation. Assuming only targeted or partial help with energy bills beyond the spring, combined with tighter fiscal policy, we could expect higher headline inflation in the middle of next year, but lower underlying inflationary pressures, which could be a good environment for index-linked gilts, offering good carry from still-elevated retail price inflation, while real yields may drop as the economy sags.

It was noteworthy that under Truss and Kwarteng’s plan to borrow over £70bn extra this year, virtually nothing was allocated to additional index-linked gilt issuance, such is the sensitivity of these bonds to higher inflation. Even as financing needs abate, we would expect index-linked gilt supply to remain relatively low as a proportion of the total debt issuance, which may also offer technical support to that market, offset by uncertainty around future LDI-driven demand.

Plate Spinning at the Bank of England

Meanwhile the Bank of England continues its plate spinning: raising interest rates to tackle inflation, selling corporate bonds and gilts (after false starts) as part of its quantitative tightening (QT), while standing ready to take additional measures if financial stability is threatened. Confirmation that the full fiscal statement and Office for Budget Responsibility (OBR) forecasts will be delayed until November 17, to allow time for the new prime minister and cabinet to fine-tune fiscal policy, only adds to the Bank’s headache, as the next interest-rate policy meeting is on November 3.

We now know that the Bank of England had not been briefed about the disastrous ‘mini budget’ when it made its last rate decision the day before that event. We hope and expect that Bank officials will at least have been briefed on the outlines of fiscal plans before they make their next decision.

The delay to the fiscal update from October 31 to November 17 is perhaps understandable, but it has created a little more market volatility, albeit not on the scale of late September/early October, because the renewed commitment to fiscal responsibility seems non-negotiable for now.

Fewer UK Rate Rises Ahead?

Should the Monetary Policy Committee press ahead with QT, and the chancellor plug the budget gap with fiscal restraint, it may mean fewer rate rises. This might help short-dated gilts but is unlikely to be supportive for sterling, already dogged by twin deficits and high inflation; however, it is already beaten up. Gilts may capture a bid on weakening economic growth, and long gilts are currently excluded from QT, providing some respite, but we would not base a long-term investment case on this temporary reprieve, especially when faced with uncertain demand from overseas investors and pension funds.

As gilt supply is still likely to outstrip demand, even as spending plans are reined in, and with political and social discord high, twin deficits, and the UK’s relations with the European Union still fraught, we expect volatility in sterling assets to remain high. In our opinion, having reversed most of the sell-off since late September, gilt yields are not high enough to represent compelling value versus better-rated New Zealand, Australia and, to a lesser extent, US government bonds.

We assess the UK’s current monetary and fiscal predicament and the prospects for the gilt market.

Key points

- Radical UK government policies which aimed to slash taxes to aid growth have been replaced by a renewed focus on fiscal discipline.

- Panic has subsided in the gilt market, but the perceived hit to credibility and confidence are longer lasting.

- Mortgage rates have yet to fall materially, remaining at almost double the rates they were at six months ago.

- The decision not to extend generalised energy price caps beyond the spring reduces the potential hole in the public finances, but higher implied future borrowing costs, on top of the hefty additional interest bill on index-linked gilts already incurred, still leaves a sizeable gap to fill.

- Should the Bank of England’s Monetary Policy Committee press ahead with quantitative tightening (QT), and the chancellor plug the budget gap with fiscal restraint, it may mean fewer interest-rate rises.

- In our view, having reversed most of the sell-off since late September, gilt yields are not high enough to represent compelling value versus better-rated New Zealand, Australia and, to a lesser extent, US government bonds.

It has been a tumultuous few weeks for the United Kingdom, not least for the gilt market. As I wrote recently in a blog entitled The closest thing to crazy? in the aftermath of the not-so-mini budget in late September, that ill-fated fiscal statement contained what we believed to be many of the wrong policies and the wrong priorities at the wrong time.

The statement elicited a damning verdict from the financial markets, as well as in opinion polls, and it caused havoc for UK defined benefit pension schemes, necessitating emergency intervention from the Bank of England. As predicted in the blog, the authors of those seemingly ill-judged policies (Prime Minister Liz Truss and Chancellor Kwasi Kwarteng) were both forced to resign.

New leadership

The UK now has a new prime minister and a new chancellor in Rishi Sunak and Jeremy Hunt respectively. Radical policies which aimed to slash taxes to aid growth have been replaced by a renewed focus on fiscal discipline. Panic has subsided in the gilt market, but the perceived hit to credibility and confidence are longer lasting. Not least, mortgage rates have yet to fall materially, remaining at almost double the rates they were at six months ago. Recent data also suggests an understandable reluctance by consumers to buy big-ticket items.

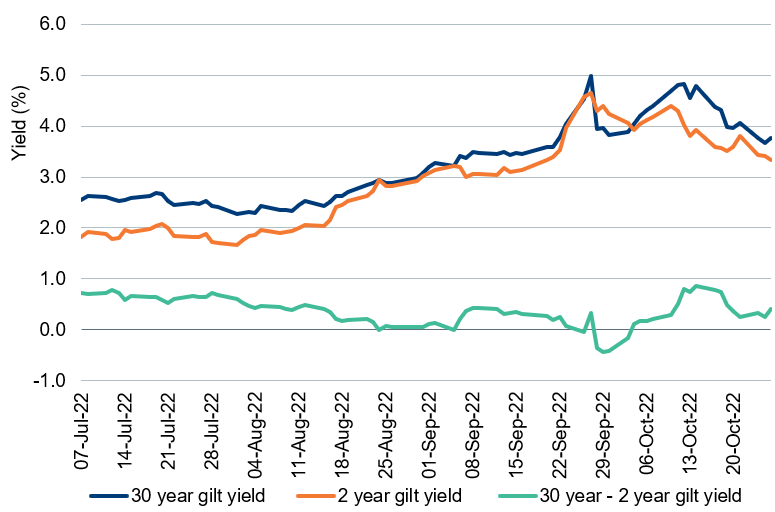

Gilt yields have retraced somewhat from the 5% peak seen in late September, but they remain materially higher than over the summer. Not only has the level of gilt yields remained volatile, but the curve shape has been very erratic, as the Bank of England plays ‘whack-a-mole’. The chart below shows the 2-year and 30-year gilt yield history since former Prime Minister Boris Johnson was forced to resign in early July.

UK gilt yields 7 July – 26 October 2022 (%)

Source: Bloomberg, 26 October 2022

Emergency intervention on financial-stability grounds in late September arrested the spike in long-term gilt yields which had been brought about by forced selling from the liability-driven investing (LDI) community and caused the curve to invert briefly. However, in the first half of October the curve re-steepened, before the budget measures were progressively reversed and the curve flattened again. The Bank of England’s decision to exclude any gilts dated 20 years or more from its plan to sell gilts for the remainder of 2022 also supported this flattening.

Rating downgrades

The decision not to extend generalised energy price caps beyond the spring reduces the potential hole in the public finances, but higher implied future borrowing costs, on top of the hefty additional interest bill on index-linked gilts already incurred, still leaves a sizeable gap to fill. Credit rating agency decisions to revise the outlook on the UK’s rating to negative over recent days reflect this.

See-sawing energy pricing policy also has implications for inflation; former Chancellor Sunak’s policy of allowing the market to set utility prices but paying rebates meant that headline inflation rose, at significant cost to the Exchequer in the form of higher interest and principal payments on index-linked gilts. Former Prime Minister Truss’ price capping pushed down headline inflation, but other policies threatened to push up core inflation. Assuming only targeted or partial help with energy bills beyond the spring, combined with tighter fiscal policy, we could expect higher headline inflation in the middle of next year, but lower underlying inflationary pressures, which could be a good environment for index-linked gilts, offering good carry from still-elevated retail price inflation, while real yields may drop as the economy sags.

It was noteworthy that under Truss and Kwarteng’s plan to borrow over £70bn extra this year, virtually nothing was allocated to additional index-linked gilt issuance, such is the sensitivity of these bonds to higher inflation. Even as financing needs abate, we would expect index-linked gilt supply to remain relatively low as a proportion of the total debt issuance, which may also offer technical support to that market, offset by uncertainty around future LDI-driven demand.

Plate spinning at the Bank of England

Meanwhile the Bank of England continues its plate spinning: raising interest rates to tackle inflation, selling corporate bonds and gilts (after false starts) as part of its quantitative tightening (QT), while standing ready to take additional measures if financial stability is threatened. Confirmation that the full fiscal statement and Office for Budget Responsibility (OBR) forecasts will be delayed until 17 November, to allow time for the new prime minister and cabinet to fine-tune fiscal policy, only adds to the Bank’s headache, as the next interest-rate policy meeting is on 3 November.

We now know that the Bank of England had not been briefed about the disastrous ‘mini budget’ when it made its last rate decision the day before that event. We hope and expect that Bank officials will at least have been briefed on the outlines of fiscal plans before they make their next decision.

The delay to the fiscal update from 31 October to 17 November is perhaps understandable, but it has created a little more market volatility, albeit not on the scale of late September/early October, because the renewed commitment to fiscal responsibility seems non-negotiable for now.

Fewer rate rises ahead?

Should the Monetary Policy Committee press ahead with QT, and the chancellor plug the budget gap with fiscal restraint, it may mean fewer rate rises. This might help short-dated gilts but is unlikely to be supportive for sterling, already dogged by twin deficits and high inflation; however, it is already beaten up. Gilts may capture a bid on weakening economic growth, and long gilts are currently excluded from QT, providing some respite, but we would not base a long-term investment case on this temporary reprieve, especially when faced with uncertain demand from overseas investors and pension funds.

As gilt supply is still likely to outstrip demand, even as spending plans are reined in, and with political and social discord high, twin deficits, and the UK’s relations with the European Union still fraught, we expect volatility in sterling assets to remain high. In our opinion, having reversed most of the sell-off since late September, gilt yields are not high enough to represent compelling value versus better-rated New Zealand, Australia and, to a lesser extent, US government bonds.