We assess the drivers behind unusual recent moves in global bond markets and consider what may happen next.

Key points

- The multi-decade decline in inflation since the 1970s has been a key driver of the multi-decade bull market for bonds.

- Unusually, despite recent higher inflation, bond yields have fallen over the last couple of months.

- For government bonds, we anticipate a consolidation phase for the rest of the summer, with inflation numbers trending down and central-bank demand remaining high, but potential issues late in the year.

- We believe it may be prudent for bond investors to have some protection over the next couple of months.

- The supportive backdrop for some credit markets (improving profits, lower defaults, and inexpensive finance) should continue to put downward pressure on spreads.

Inflation has always been a serious influencer upon bond-market behavior. The multi-decade decline in inflation since the 1970s explains in large part why we have enjoyed a multi-decade bull market for bonds. The reasons are simple: higher inflation erodes the fixed return you receive from a bond and prompts central banks to raise rates.

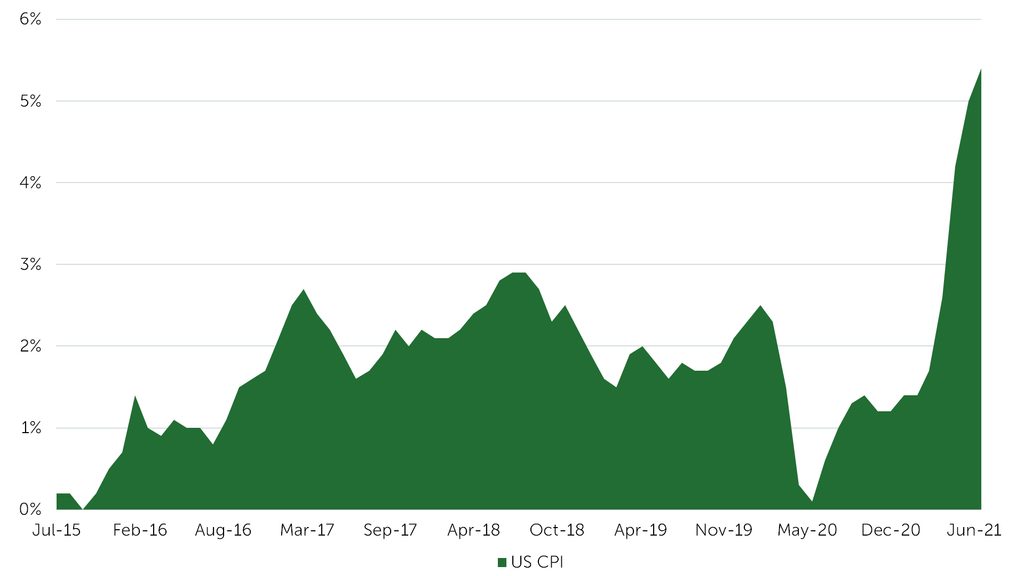

It is therefore strange that, despite recent higher inflation (see the US chart below), bond yields have fallen (returns have risen) over the last couple of months. Below, we will try to explain this phenomenon and provide our expectations for what we believe may happen next.

US Consumer Price Inflation (CPI), July 2015-July 2021 (%)

Source: Bloomberg, July 21, 2021

Government-bond markets have been the best performing bond markets recently despite these higher-than-expected inflation numbers and central banks talking about tapering quantitative easing. Yields have fallen – for example, the US 10-year yield is down from 1.74% at the end of March to around 1.30% now.

When investors are confused about markets reacting illogically to the economic data, there are the inevitable stories about the less well-known fundamentals of supply and demand imbalances and market positioning. On the demand/supply point, it is well known now that in the US the Federal Reserve has been buying up all the net supply of Treasuries, and that investors have also been buying back Treasuries ever since.

Chinese Economy Slowing?

Moreover, if you dig a little deeper into the economic and monetary data, you can see that the reflation story is not all one-way traffic. Some forward-looking economic indicators have been rolling over (from very high levels) and the ‘transitory inflation story’ is well known, so why worry about it?

Furthermore, China’s credit cycle (historically a key leading indicator for commodity prices) has been tightening sharply, causing a domestic retrenchment. The China credit impulse has been declining since its peak in September last year and you can see the effects on some of China’s leading indicators below, alongside slowing momentum in US and European purchasing managers’ index (PMI) data too.

World Economic Indicators over the Last Five Months

Source: Newton, Bloomberg July 2021

More Importantly, What Next?

For government bonds, we anticipate a consolidation phase for the rest of the summer, with inflation numbers trending down and central-bank demand remaining high. We also see fiscal support for the economy receding, with the removal of some of the emergency support packages. This support (through credit and income payments) has been significant, and not all of it will be replaced as economies open; for markets, it may offer more of a short-term catalyst for greater volatility.

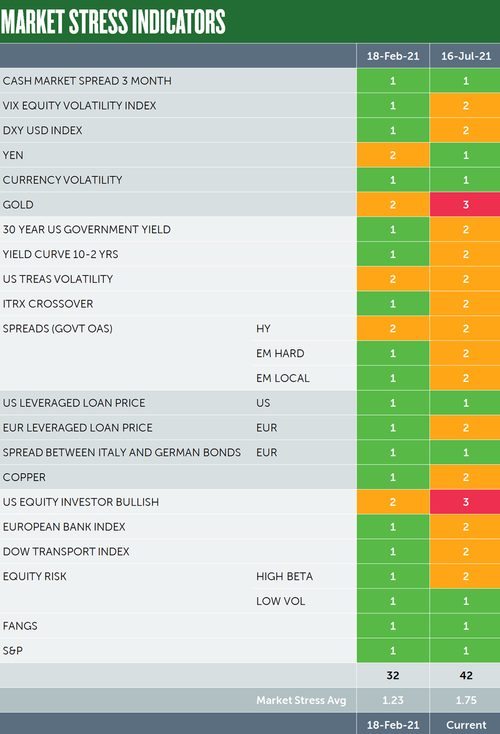

We have dusted off our market-stress table once again (see below). This set of indicators has been in ‘goldilocks’ territory since the middle of last year, but some indicators are flashing red, causing us some concerns right now.

Therefore, we believe it may be prudent for investors to have some protection over the next couple of months. There is also the continued spread of Covid-19 variants to worry about, and, increasingly, markets will be focusing on the ‘haves’ and the ‘have nots’, in terms of who has and has not been vaccinated.

Market Stress Indicators – February 18 and July 16, 2021

Source: Newton, Bloomberg July 2021

We believe it is prudent for bond investors to tactically reduce any shorts on the US dollar, and to consider reducing emerging-market currency exposure. In our view, it may also be worth considering adding to any call options on the US Treasury market.

The fourth quarter is where we see more significant problems developing for government–bond markets as central banks will need to step up the rhetoric about removing the various financial support ‘punchbowls’, and renewed fiscal support will weigh on bond supply. Furthermore, China is now loosening monetary policy which may support global growth later in the year. We expect government-bond market yields to rise as a result.

Credit Markets to Improve?

The supportive background for some credit markets (improving profits, low defaults, and cheap finance) will continue to put downward pressure on spreads. It is not a one-way story however, and we favor BBB to B-rated credit. High-quality credit is more influenced by government-bond yields and offers limited spread compression, while we believe CCC-rated bonds are very rich and do not reflect the uncertain economic recovery.

Emerging-market bonds are a mixed bag. Hard-currency emerging-market bonds have proven themselves to be a higher-beta US duration risk, and spreads are relatively tight. This suggests vulnerability if US yields rise once more. Local-currency markets are different, as divergent vaccination and monetary policy is likely to raise political volatility, and, as a result, currency risks.

Authors

Paul Brain

Deputy chief investment officer of Multi-Asset

Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice.

Important information

This is a financial promotion. Issued by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Newton Investment Management Limited is authorized and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. 'Newton' and/or 'Newton Investment Management' brand refers to Newton Investment Management Limited. Newton is registered in England No. 01371973. VAT registration number GB: 577 7181 95. Newton is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Newton's investment business is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only.

Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms, including Newton and (iv) representatives of Newton Americas, a Division of BNY Mellon Securities Corporation, U.S. Distributor of Newton Investment Management Limited.

Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York or any of its affiliates. The Bank of New York assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith. © 2020 The Bank of New York Company, Inc. All rights reserved.

Comments