Sustainability is a hot topic for investors, but conversations do tend to focus on exclusion. While we understand this impulse, as there are likely to be pronounced negative consequences of investing in an area that a client considers to be at odds with a sustainable focus, we strongly believe that there are many positive opportunities when it comes to sustainable investing that are currently overlooked. At Newton, we use ‘red lines’ to make clear which areas we deem unsuitable for sustainable investment, but we are also constantly discussing which industries and companies could benefit our sustainable strategies. We believe that sustainability is a valuable mindset through which to evaluate opportunities as well as to exclude them.

We are amid a societal shift away from the Friedman theory that profit maximisation should be the sole objective of company management. While it is important to appreciate that, as part of profit maximisation, companies have an implicit social licence to operate (a licence that has to be earned and maintained), we believe that the conversation is evolving. In the past, it has been possible to earn supernormal profits through the exploitation and depletion of natural and human capital, but in the future we believe businesses that rely on an under-pricing of negative external factors will see their profits come under pressure. We also think that this will make space for new companies that can innovate to provide the solutions to these factors. Challenges tend to present opportunities.

Convenience food conflicts

The prevailing consumer trend is for food on the go, with consumers choosing convenience and speed over taking the time to sit down and eat.[1] This change in eating habits has produced an increased requirement for ‘shelf-stable’ foods. However, traditional stabilisers, including salts, fats and sugars, have brought about significant detrimental effects on health, with diabetes now costing the UK’s NHS £14bn per year, which makes up 10% of the national health budget.[2] Governments are now starting to price in these negative influences with a sugar tax, among other initiatives, while many individual consumers are seeking out healthier, whole food products to improve their own health. While this is all sounds positive, research has revealed, understandably, that there remains an unwillingness to compromise on taste, which can be difficult when reducing salt, fat and sugar content considerably. At the same time, consumers and governments are placing pressure on companies to reduce food waste and plastic usage, as agriculture produces one third of global carbon emissions and research suggests that one third of food produced for human consumption is wasted each year.[3]

There are many good intentions around nutrition and waste production, but many of the demands do appear to be conflicting. Plastic is used in part to increase shelf life and reduce waste, but both plastic reduction and waste reduction are consumer and government aims. Similarly, people are looking for food which contains less sugar and fewer artificial preservatives, but which can also be picked up quickly and eaten on the go.

These conflicting aims do present challenges. However, situations like the above offer many value-creation opportunities. We have identified some food-technology companies which are able to address many of the conflicting demands outlined above, which we think are exciting additions to the consumer area. Some of these companies are working on product reformulation to reduce problematic ingredients, which can be most meaningfully achieved through improvements in the industrial processes and the use of cultures and enzymes. One such technology allows products to be shelf-stable in temperatures up to 40 degrees Celsius, which could be of great use in warmer climates.

Another trend within the food industry, which has been enabled by the rise of social-media advertising, is a significant increase in the number of small niche brands taking share from the bigger industry players. Small brands will often outsource most of the research and development (R&D) and focus on sales and marketing. Increasingly, large brands are also outsourcing R&D for new and smaller product lines, meaning that a new product can be launched in just 6 months rather than 2-3 years.

Current environmental challenges and changing consumer preferences clearly present investible opportunities that suit sustainable strategies.

Are electric vehicles the future, whether consumers like it or not?

1Source: European Environment Agency, Jato Dynamics Ltd, Shutterstock, April 2018

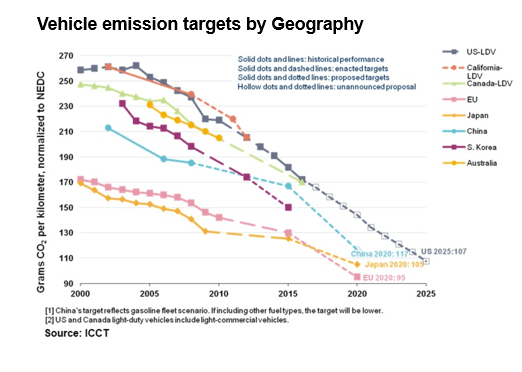

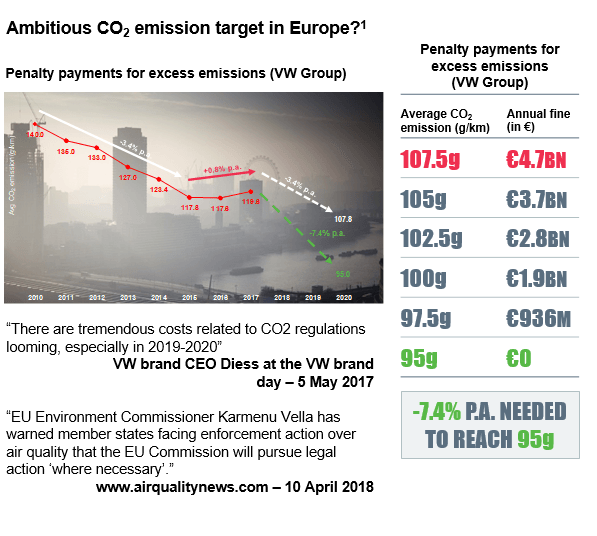

As with convenience food and plastic waste, transportation receives a considerable amount of interest as it must be a key part of efforts to reduce emissions. The first chart above shows that across all geographies tough emissions targets have been put in place, while the following charts show Volkswagen’s current fleet emissions and where they need to get to in order to meet regulations in 2020. Much of the discussion about electric vehicles seems to centre on whether consumers want them and whether the infrastructure is in place, which we believe is missing the point as electric vehicles are coming whether consumers think they want them or not. Between 2010 and 2015, Volkswagen fleet emissions were falling at 3.4% per annum, owing to the improvement in internal combustion engine efficiency, while diesel sales were relatively stable.[4] Following the diesel-gate scandal, new diesel sales have dropped significantly in favour of petrol engines, which emit 15-20% more CO2 on average at similar power. The vehicle mix has also had an impact, with sport utility vehicles continuing to grow in popularity despite emitting more CO2 compared to regular cars. Together, both fuel type and mix shift have caused fleet carbon emissions to actually start rising again, neglecting any additional internal combustion engine efficiency gains.

It is now impossible for the major auto makers to meet their fleet emissions targets in 2020 without replacing a decent proportion of sales with electric vehicles. For example, if Volkswagen replaces 10% of its sales with electric vehicles in 2020, it will save approximately €15,000 in fines for every electric vehicle it sells. The incentive to produce electric vehicles and get them into the hands of consumers is therefore very high. Understanding the regulatory dynamics here shows us that certain investments in the electric-vehicle supply chain are likely to see a significant growth in volumes in the near term. We can base our investment analysis on observable data points rather than taking a view on concerns such as consumer preference and range anxiety. Our work on sustainability and climate change indicates that regulation is likely to be unrelenting, which gives us confidence in electric vehicles as a promising area of investment.

[1] https://foodinsight.org/2018-food-and-health-survey/

[2] https://www.diabetes.co.uk/cost-of-diabetes.html

[3] http://www.fao.org/save-food/resources/keyfindings/en/

[4] https://www.acea.be/statistics/tag/category/share-of-diesel-in-new-passenger-cars

Authors

Philip Shucksmith

Portfolio manager, Real Return team

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those countries or sectors. Please note that holdings and positioning are subject to change without notice

Comments