We explain what we would like to see from the participants at this year’s climate-change event in Egypt.

Key Points

- COP27 is currently being hosted in Egypt with the three main goals being to agree collective plans around climate-change mitigation, adaptation and finance.

- Despite 196 governments agreeing at COP21 in Paris in 2015 to limit temperature rises to well below 2 degrees Celsius above pre-industrial levels, and preferably to limit the increase to 1.5 degrees Celsius, carbon emissions continue to rise.

- As part of the Paris Agreement at COP21 in 2015, developed countries committed to providing developing countries with US$100bn per annum to manage climate change.

- This sum has yet to be met, but it may proveinsignificant compared to what more may be required to finance the global energy transition

It has been 27 years since countries and global organisations first met at the United Nations (UN) Climate Change Conference, or COP for short, to collectively discuss how to bring about carbon-emission reductions. To many observers, this might be construed as 27 years of talking but a relative dearth of meaningful action. In this blog, we reveal our wish list of commitments and pledges we and our clients would like to see from governments and companies at COP27.

COP27 is being hosted in Egypt this year from November 6 to 18. It is significant that an African country is hosting the latest COP, given that the continent is at the sharp end in terms of its vulnerability to the consequences of climate change. In addition, Egypt is responsible for around 13% of Africa’s carbon footprint while having only 7.6% of the population, so there is pressure on the country to deliver in relation to its own goals as well as attempting to re-energize the issue globally.

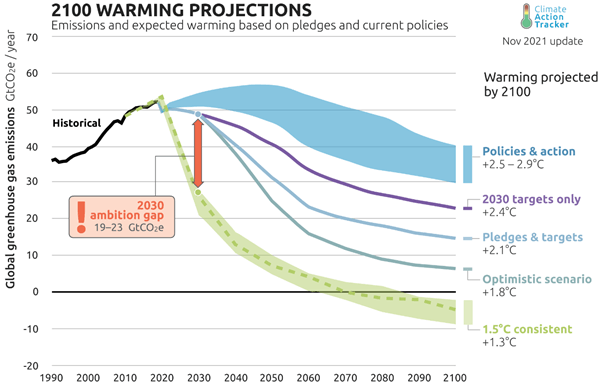

The global context for COP27 is that despite 196 governments agreeing at COP21 in Paris in 2015 to limit temperature rises to well below 2 degrees Celsius above pre-industrial levels, and preferably to limit the increase to 1.5 degrees Celsius, carbon emissions rose from 35 gigatons (Gt) in 2016 to 37 Gt prior to the Covid pandemic. They are currently projected to be around 19-23 Gt higher than required under pathways consistent with the 1.5-degree Celsius outcome even if existing 2030 targets are hit. The graphic below highlights the magnitude of the challenge.

Source: Climate Action Tracker, November 2021 Update. (One GtC02e equals one billion tonnes of carbon dioxide).

All COPs are important as they are an opportunity for countries to negotiate and work through disagreements. The three main goals for COP27 are mitigation, adaptation and finance. We look at each one below and set out our expectations.

Mitigation

Russia’s invasion of Ukraine has prompted a global energy crisis that has been in the making for at least a decade. While the current crisis is likely to be a long-term accelerant for climate action as countries seek to invest in new energy supplies which are typically cleaner, the scramble for energy security has led to a near-term resurgence in fossil-fuel power.

At the last event, COP26 in Glasgow, countries committed to resubmit enhanced emission-cutting pledges. At COP27, we hope that countries will reiterate their long-term commitments and strengthen their medium-term commitments to help reduce dependency upon an antiquated energy system that can be broadly characterized as one of monopoly, pollution and geopolitical vulnerability.

This will, we hope, arrive in the shape of some updated nationally determined contributions to global emission reductions and increased commitments to renewable energy as part of the energy mix. The countries likely to update their plans include Chile, Egypt, Indonesia, Mexico, Turkey, United Arab Emirates and Vietnam, which collectively represent around 4% of global emissions.[1]

Adaptation

The role of adaptation has gained prominence in the face of the increasing frequency of natural catastrophes that are being linked to climate change. Examples such as the recent floods in Pakistan, hurricanes in the US, and wildfires in Australia, the US and Europe, have focused the mind that building resiliency into our global systems is becoming a prerequisite, particularly in the face of increasing global emissions. The UN estimates that typically only around 20% of climate change-related finance goes towards adaptation as it is more difficult to generate a return from such activity than from mitigation projects like renewable energy.[2] It is not anticipated that there will be any concrete outcomes on adaptation but, instead, that countries will continue to enhance their understanding of climate adaptation and flesh out principles and targets on how it can be achieved. This foundation building is important to enable meaningful progress in 2023.

Finance

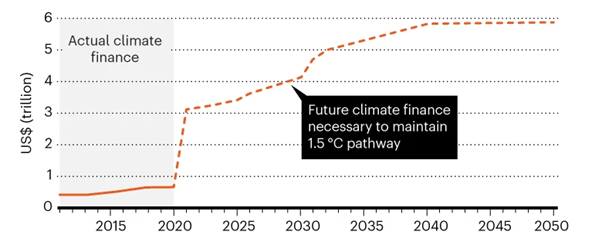

There are two components within financing: first, climate finance, and second, loss and damage. As part of the Paris Agreement in 2015, developed countries committed to providing developing countries with US$100bn per annum to manage climate change. This transfer was agreed owing to the reality that the bulk of the cumulative cause of climate change rested with developed nations. Since the Paris Agreement, this target has not been met. In 2021, it was closest to being achieved when US$83bn was raised through public and private sources. The bigger picture here is that the US$100bn is insignificant compared to what may be required to finance the global energy transition as estimated in the chart below.[3]

Climate Finance (Actual and Forecast Requirements)

Source: Climate Policy Initiative, 2020

At COP27, developing countries will be seeking to reapply the pressure on developed countries to deliver, and we would like to see the beginnings of an agreement between developed countries as to who will provide what, to whom, and when. These nascent plans could then be finalized at COP28 in 2023.

This clarity will help developing countries to plan capital expenditure for either mitigation or adaptation initiatives which are so desperately needed if the Paris Agreement’s goal to limit temperature rises to 1.5 degrees Celsius is to be realized. Given the near-term geopolitical and inflationary headwinds facing much of the developed world, we fear that enthusiasm for this process is likely to be somewhat muted at COP27.

The issue of loss and damage has become a contentious issue in the last few years with no consensus or enforceable plan. Loss and damage differ from mitigation and adaptation, in that they seek to provide help to people after they have suffered climate-related events, while mitigation works on preventing it and adaptation on minimizing it.

Despite developed nations having caused the issue of climate change, national-level political cycles and self-interests have served to deter developed world governments from being interested in transferring sufficient wealth or paying compensation. Given the increasingly deglobalized world and political challenges at a national level in developed markets, we fear there is a high probability that insufficient progress will be made in this area at COP27, as developed countries seek to protect themselves from extra liabilities against a government budget-constrained backdrop. At best, we hope that some meaningful pledges will be made that can serve to help in the fight against the biggest existential threat we face.

[1] https://www.whitehouse.gov/briefing-room/statements-releases/2022/06/18/chairs-summary-of-the-major-economies-forum-on-energy-and-climate-held-by-president-joe-biden/

[2] https://www.un.org/en/climatechange/raising-ambition/climate-finance

[3] https://www.nature.com/articles/d41586-021-02846-3

Authors

Newton responsible investment team

Responsible investment team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. Newton manages a variety of investment strategies. How ESG considerations are assessed or integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved. ESG may not be considered for each individual investment and, where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions. ESG considerations do not form part of the research process for Newton's small cap and multi-asset solutions strategies. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY Mellon"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.