What legacy will the dwindling use of coal leave for the energy industry and investors in renewables?

- Global demand for coal is falling as electricity producers seek cleaner alternatives, and the cost of renewable energy tumbles.

- While Covid-19 lockdowns are expected to have a negative immediate impact on the commissioning and construction of some renewable projects, the long-term forecast for renewables appears bright.

- Renewables can also offer investors diversification benefits and the prospect of stable income payments.

In June, the UK went two months without burning coal for energy – the longest period since the industrial revolution[1] in what some hailed as a major landmark in the move away from CO2-generating fossil fuels to more sustainable energy production.

The shift was partly owing to reduced electricity demand in the nationwide lockdown forced by the Covid-19 coronavirus pandemic. Yet, while a period of unusually sustained sunny weather also played its part, such a long phase of coal-free power generation also demonstrated the benefits of the investment the UK has made in renewable energy and other power sources over the last decade.

According to International Energy Agency (IEA) estimates, the height of the Covid-19 crisis reduced electricity demand by 20% or more in countries with full lockdown measures. In May it forecast global electricity demand was set to drop by 5% in 2020, the largest decline since the Great Depression of the 1930s.[2] The IEA added that renewable energy appears to have been the power source most resilient to Covid‑19 lockdown measures.

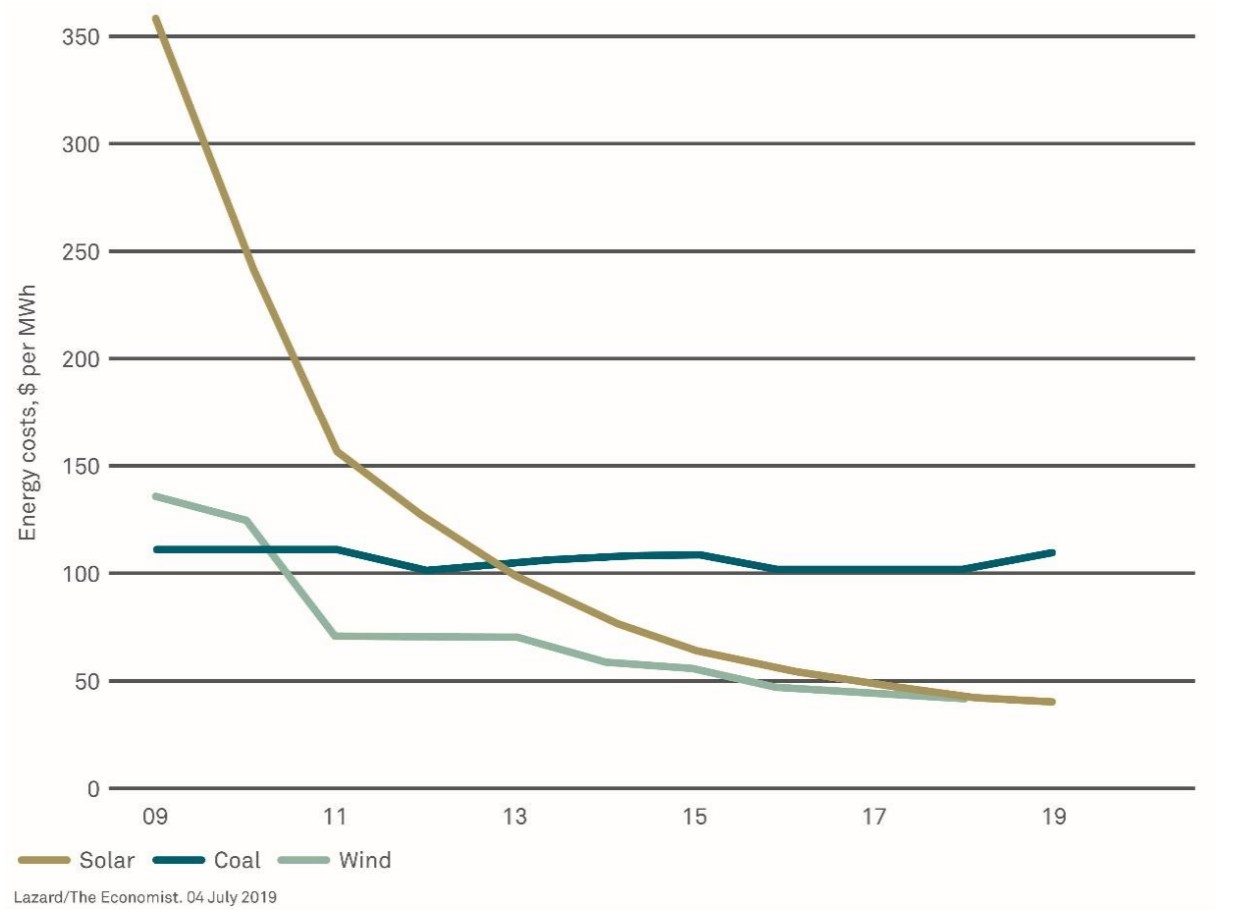

Against this backdrop, the future for coal-burning power generation in many developed markets looks increasingly bleak. In addition to the environmental costs associated with burning coal, the fossil fuel is now often more expensive than solar or wind power. Furthermore, since coal-generating power stations can be difficult to turn on and off, they can lack flexibility.

The UK is not alone in seeking to end coal-fired power generation. Other European countries are also seeking to do this, with Germany, whose grid is more reliant on coal than many other European countries, intending to phase out coal use. It seeks to end coal-fired generation by 2038 at the latest and has already agreed on a shutdown schedule for individual lignite power stations while providing compensation payments for operators.[3]

Elsewhere, continuing reform of the European Union Emissions Trading System, in moves designed to cut greenhouse-gas emissions by at least 40% by 2030, also poses a potential threat to carbon-intensive coal generation in Europe.[4]

A Brighter Future?

From a renewables standpoint, the recent pandemic, coupled with the slow death of coal, could deliver an unexpected bounty for more sustainable energy producers and their investors.

While Covid-19 lockdowns are expected to have a negative immediate impact on the commissioning and construction of some renewable projects – amid broader economic inertia – investors actually gave the green light to US$35bn worth of offshore wind projects worldwide in the first half of 2020, more than quadrupling the figure from the previous year in this area, and the long-term forecast for other renewables appears bright.[5]

About five million jobs are already associated with the solar and wind industries and the falling cost of new wind and solar projects over the last decade has also made capital investment far more productive – all of which is further bad news for coal and other fossil-fuel producers.

Energy costs, $ per MWh

At a wider economic level, many major markets face potentially dire economic consequences from the coronavirus pandemic and are now looking to marshal recovery. In many countries, this looks set to be primed by government spending, some of which could be earmarked for renewable-energy projects. In June, the UK government sketched out plans for what it calls a £5bn (US$6.5bn) ‘new deal’[6] aimed at building houses and renewing infrastructure which will include £3bn (US$3.9bn) of energy-efficiency measures.[7]

While renewable energy remains a variable power source, dependent largely on the weather, we believe that continuing national energy-efficiency drives, the use of ‘smart’ technologies in metering and other areas of the grid all bode well for renewable-energy operators and investors in the sector. Over the last 15-20 years we have continually driven greater energy efficiency in our homes through means such as better insulation, LED lighting, smart meters and improvements to the wider grid system. As the use of renewables increases we also expect to see the development of more sophisticated battery technologies. This should provide more flexible power storage that could allow electricity to be stored and brought back to the market as it is required.

We believe that renewables, many of which benefit from steady government subsidies that can help to underpin the value of investments in the sector, can offer investors important diversification benefits. Furthermore, while the coronavirus crisis has resulted in many dividend cuts in wider equity markets, renewables have continued to pay stable dividends throughout this turbulent period. We think that this can help to compound returns over the longer term, and is also particularly relevant in the context of the growing number of retirees who require a regular income from their investments.

[1] The Independent. Britain goes coal-free for two months – longest period since industrial revolution. June 9, 2020.

[2] IEA. Global energy demand to plunge this year as a result of the biggest shock since the Second World War. April 30, 2020.

[3] Clean energy wire. Spelling out the coal exit – Germany’s phase-out plan. June 30, 2020.

[4] European Council, Council of the European Union. EU Emissions Trading System reform: Council approves new rules for the period 2021 to 2030. February 27, 2018.

[5] Guardian. Offshore wind energy investment quadruples despite Covid-19 slump. July 13, 2020.

[6] BBC. Coronavirus: Johnson sets out ‘ambitious’ economic recovery plan. 30 June 2020.

[7] FT. UK government’s £3bn energy efficiency plan ‘not yet a green recovery’, 8 July, 2020.

Authors

Paul Flood

Head of Mixed Assets Investment

Newton manages a variety of investment strategies. Whether and how ESG considerations are assessed or integrated into Newton’s strategies depends on the asset classes and/or the particular strategy involved, as well as the research and investment approach of each Newton firm. ESG may not be considered for each individual investment and, where ESG is considered, other attributes of an investment may outweigh ESG considerations when making investment decisions.

Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice.

Important information

This is a financial promotion. Issued by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Newton Investment Management Limited is authorized and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. 'Newton' and/or 'Newton Investment Management' brand refers to Newton Investment Management Limited. Newton is registered in England No. 01371973. VAT registration number GB: 577 7181 95. Newton is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Newton's investment business is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only.

Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms, including Newton and (iv) representatives of Newton Americas, a Division of BNY Mellon Securities Corporation, U.S. Distributor of Newton Investment Management Limited.

Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York or any of its affiliates. The Bank of New York assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith. © 2020 The Bank of New York Company, Inc. All rights reserved.

In Canada, Newton Investment Management Limited is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Ontario and Quebec and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.